![]()

Hydrofarm Holdings Group Announces Fourth Quarter and Full Year 2021 Results

Company Provides Full Year 2022 Outlook

SHOEMAKERSVILLE, Pa., March 01, 2022 (GLOBE NEWSWIRE) — Hydrofarm Holdings Group, Inc. (“Hydrofarm” or the “Company”) (Nasdaq: HYFM), a leading independent manufacturer and distributor of branded hydroponics equipment and supplies for controlled environment agriculture (“CEA”), today announced financial results for its fourth quarter and full fiscal year ended December 31, 2021.

Fourth Quarter 2021 Highlights vs. Prior Year Period:

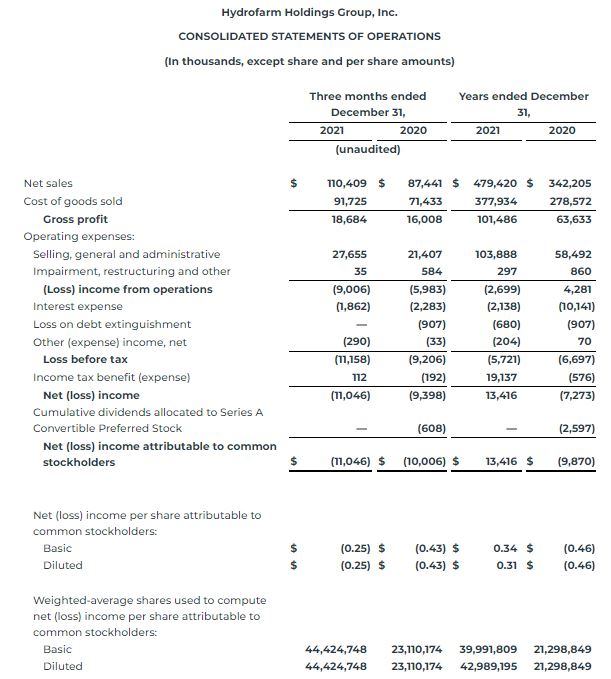

- Net sales increased 26.3% to $110.4 million compared to $87.4 million.

- Gross profit increased 16.7% to $18.7 million compared to $16.0 million.

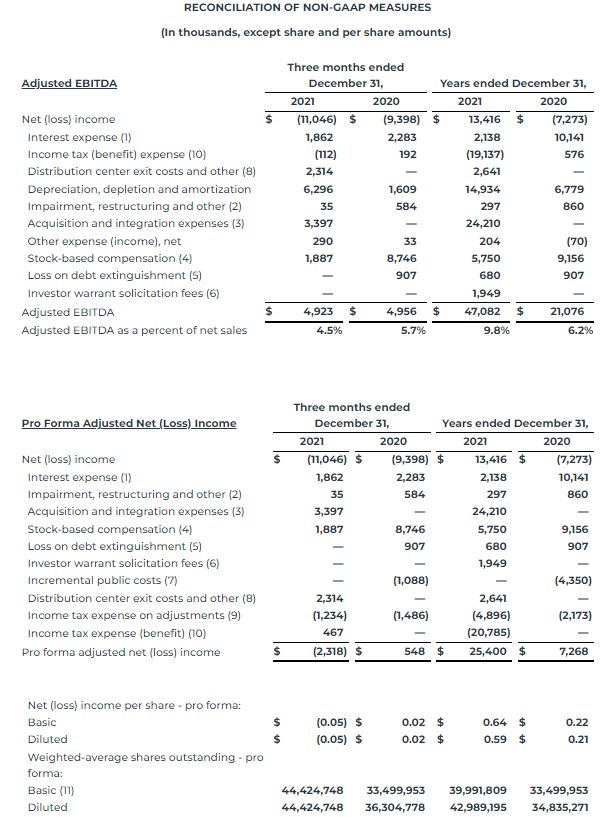

- Net loss attributable to common stockholders was ($11.0) million, or ($0.25) per diluted share, compared to a net loss of ($10.0) million, or ($0.43) per diluted share. Pro forma adjusted net loss(1) was ($2.3) million, or ($0.05) per pro forma diluted share, compared to a pro forma adjusted net income of $0.5 million, or $0.02 per pro forma diluted share.

- Adjusted EBITDA(1) decreased 0.7% to $4.9 million compared to $5.0 million.

- Closed on new $125.0 million Senior Secured Term Loan Facility.

- Completed acquisition of Innovative Growers Equipment and related entities (“IGE”).

Fiscal Year 2021 Highlights vs. Prior Year:

- Net sales increased 40.1% to $479.4 million compared to $342.2 million.

- Gross profit increased 59.5% to $101.5 million compared to $63.6 million.

- Net income attributable to common stockholders was $13.4 million, or $0.31 per diluted share, compared to a net loss of ($9.9) million, or ($0.46) per diluted share. Pro forma adjusted net income(1) was $25.4 million, or $0.59 per pro forma diluted share, compared to $7.3 million, or $0.21 per pro forma diluted share.

- Adjusted EBITDA(1) increased 123.4% to $47.1 million compared to $21.1 million.

- Completed five acquisitions during the year.

Full Year 2022 Outlook:

- Net sales growth of 20.0% to 28.0%, or approximately $575.0 million to $615.0 million.

- Adjusted EBITDA(1) of $63.0 million to $74.0 million, or approximately 11.0% to 12.0% of net sales.

(1) Adjusted EBITDA and Pro Forma Adjusted Net (Loss) Income are non-GAAP measures. For reconciliations of GAAP to non-GAAP measures see the “Reconciliation of Non-GAAP Measures” accompanying the release. Note that Pro Forma Adjusted Net (Loss) Income is pro forma as if our Initial Public Offering (IPO) had occurred at the beginning of each period presented. Please see the “Non-GAAP Financial Measures” for definitions used herein.

Bill Toler, Chairman and Chief Executive Officer of Hydrofarm, said, “While we posted solid top line growth during the fourth quarter, our overall results were impacted by industry agricultural oversupply, which we discussed on our last earnings call, as well as higher freight and labor costs.”

For the full year 2021, we’re pleased to report successful results as we grew our top line by 40%, including organic net sales growth of over 18%. We also completed five acquisitions that further strengthened our branded product portfolio and manufacturing capabilities.

Bill Toler, Chairman and Chief Executive Officer of Hydrofarm

Bill Toler, Chairman and Chief Executive Officer of Hydrofarm

To further support our manufacturing, we expanded our distribution centers and production space by nearly 70%. And importantly, we more than doubled our adjusted EBITDA to $47 million for the year, which is within our previously provided guidance range.

Mr. Toler added, “As we look ahead, we believe we have several momentum builders in the new year, including growth expected both in the commercial channel and in our proprietary brand portfolio. Additionally, in late 2021 and early 2022 we acted on several margin enhancing initiatives to reduce costs and mitigate inflationary pressures, including increasing prices where appropriate, as well as right-sizing our headcount as we have begun realizing synergies from our 2021 acquisitions. Together with our unique position as a leading ‘picks and shovels’ supplier to the CEA industry and a strong balance sheet that can support future growth, we remain excited about our prospects in 2022 and beyond.”

Fourth Quarter 2021 Financial Results

Net sales in the fourth quarter of 2021 increased $23.0 million, or 26.3%, to $110.4 million compared to the fourth quarter of 2020, driven by an approximate 22.8% increase in volume of products sold, including sales from acquisitions closed within the quarter and preferred brands added in the year-to-date period, an approximate 2.8% increase in price/mix of products sold, and an approximate 0.7% growth from favorable foreign exchange rates. The growth in volume of products sold was related entirely to recently acquired brands, which offset a decline in organic sales.

Gross profit increased $2.7 million, or 16.7%, to $18.7 million compared to the fourth quarter of 2020, driven by the increase in net sales, tempered by an approximate 140 basis point decline in gross margin to 16.9% compared to 18.3% in the fourth quarter of 2020. The year-over-year decline in gross profit margin resulted primarily from $3.2 million in distribution center exit costs and acquisition related-costs. Gross profit margin, excluding the distribution center exit costs and acquisition-related cost was 19.8%, an approximate 150 basis point increase from the prior year period. This increase in gross profit margin was driven by a more favorable sales mix of the Company’s proprietary and preferred brand products, partially offset by higher freight and labor costs.

Selling, general and administrative (“SG&A”) expense was $27.7 million in the fourth quarter of 2021 compared to $21.4 million in the fourth quarter of 2020. The increase in SG&A expense was primarily related to 2021 distribution center exit costs and acquisition and integration-related costs, as well as increases in salaries and benefits, insurance costs and added facility costs as a result of the Company’s growth. SG&A expense, excluding acquisition and integration-related costs, stock-based compensation, depreciation & amortization, and distribution center exit costs (“Adjusted SG&A expenses”), was $18.5 million, or 16.7% of net sales, compared to $11.2 million, or 12.8% of net sales in 2020. The year-over-year increase in Adjusted SG&A expenses was largely driven by increases in added facility costs, marketing expenses, and salary and benefits.

Net loss attributable to common stockholders was ($11.0) million, or ($0.25) per diluted share, in the fourth quarter of 2021, compared to a net loss of ($10.0) million, or ($0.43) per diluted share in the fourth quarter of 2020. Pro Forma Adjusted Net Loss(1) was ($2.3 million), or ($0.05) per pro forma diluted share, in the fourth quarter of 2021, compared to Pro Forma Adjusted Net Income of $0.5 million, or $0.02 per pro forma diluted share, in the fourth quarter of 2020.

Adjusted EBITDA(1) was $4.9 million, or 4.5% of net sales, for the fourth quarter of 2021, compared to $5.0 million, or 5.7% of net sales, in the fourth quarter of 2020. The slight decrease in Adjusted EBITDA as a percentage of net sales was primarily related to higher SG&A expenses relative to net sales.

Key Fourth Quarter 2021 Events

Senior Secured Term Loan

On October 25, 2021, the Company entered into a new $125.0 million senior secured term loan facility (the “Term Loan”). The Term Loan bears interest at a rate of either LIBOR (with a 1.00% floor) plus 5.50%, or an alternate base rate (with a 2.00% floor) plus 4.50%, and matures on October 25, 2028. The Company used a portion of the net proceeds from the Term Loan to fund the cash portion of the IGE purchase price and to repay the outstanding balance under the Company’s existing revolving credit facility.

Acquisition of Innovative Growers Equipment

On November 1, 2021, the Company completed the acquisition of Innovative Growers Equipment, Inc. and related entities (“IGE”), an Illinois-based custom manufacturer of horticulture benches, racking and LED lighting systems. IGE also has a commercial equipment product range that complements Hydrofarm’s existing lineup of high performance, proprietary branded products.

Balance Sheet and Liquidity

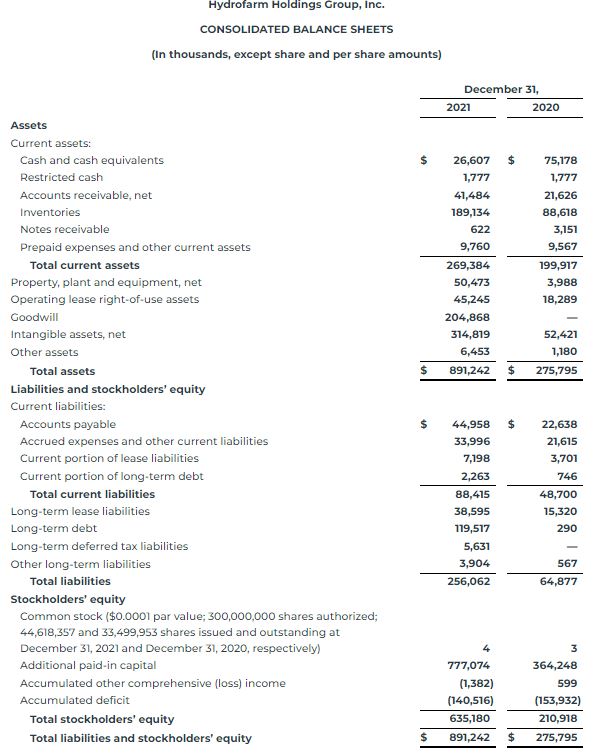

As of December 31, 2021, the Company had unrestricted cash and cash equivalents of approximately $26.6 million and an aggregate principal amount of debt outstanding of $125.4 million, as well as approximately $83.6 million of additional available borrowing capacity under its revolving credit facility.

Full Year 2022 Outlook

The Company is providing the following outlook for the full fiscal year 2022:

- Net sales growth between 20% and 28%, or approximately $575.0 million to $615.0 million.

- Adjusted EBITDA(2) of $63.0 million to $74.0 million, representing approximately 11.0% to 12.0% of net sales for the full fiscal year.

(2) Adjusted EBITDA is a non-GAAP measure. See the ”Reconciliation of Non-GAAP Measures” accompanying this release.

The Company’s 2022 outlook includes the following assumptions:

- Modest full-year organic growth and strong full-year M&A growth; organic growth is heavily weighted toward the back-half of the year with sequential improvement from negative organic growth in 1Q to positive organic growth in 3Q. This assumes industry recovery throughout 2022, as well as expected growth both in the Company’s commercial channel and in its proprietary brand portfolio.

- Pricing and cost saving initiatives that will help to mitigate the impact of rising input, freight and labor costs.

- Capital expenditures of approximately $8.0 million to $12.0 million; and

- An effective tax rate of 11% to 15% of pre-tax book income.

With respect to projected fiscal year 2022 Adjusted EBITDA, a quantitative reconciliation is not available without unreasonable effort due to the variability, complexity and low visibility with respect to certain items, including, but not limited to, stock-based compensation and employer payroll taxes, uncertainties caused by the global COVID-19 pandemic, changes to the regulatory landscape, and certain potential future transaction expenses, which are excluded from Adjusted EBITDA. The Company expects the variability of these items to have a potentially unpredictable, and potentially significant, impact on its future GAAP financial results.

Conference Call

The Company will host a conference call to discuss financial results for the fourth quarter and full year 2021 today at 4:30 p.m. Eastern Standard Time. Bill Toler, Chairman and Chief Executive Officer, and John Lindeman, Chief Financial Officer, will host the call.

The conference call can be accessed live over the phone by dialing 201-389-0879. A replay will be available after the call until Tuesday, March 8, 2022 and can be accessed by dialing 412-317-6671. The passcode is 13726991. The conference call will also be webcast live and archived on the corporate website at www.hydrofarm.com, under the “Investors” section.

About Hydrofarm

Hydrofarm is a leading independent manufacturer and distributor of branded hydroponics equipment and supplies for controlled environment agriculture, including grow lights, climate control solutions, growing media and nutrients, as well as a broad portfolio of innovative and proprietary branded products. For over 40 years, Hydrofarm has helped growers make growing easier and more productive. The Company’s mission is to empower growers, farmers and cultivators with products that enable greater quality, efficiency, consistency and speed in their grow projects.

Non-GAAP Financial Measures

Non-GAAP Financial Measures

We report our financial results in accordance with generally accepted accounting principles in the U.S. (“GAAP”). However, management believes that certain non-GAAP financial measures provide investors with additional useful information in evaluating our performance and that excluding certain items that may vary substantially in frequency and magnitude period-to-period from net income (loss) provides useful supplemental measures that assist in evaluating our ability to generate earnings and to more readily compare these metrics between past and future periods. These non-GAAP financial measures may be different than similarly titled measures used by other companies.

To supplement our audited consolidated financial statements which are prepared in accordance with GAAP, we use “Adjusted EBITDA”, “Adjusted EBITDA as a percent of net sales”, “Pro Forma Adjusted Net (Loss) Income” and “Pro Forma Adjusted Net (Loss) Income per Diluted Share” which are non-GAAP financial measures. Our non-GAAP financial measures should not be considered in isolation from, or as substitutes for, financial information prepared in accordance with GAAP. There are several limitations related to the use of our non-GAAP financial measures as compared to the closest comparable GAAP measures. Some of these limitations include:

We define Adjusted EBITDA as net (loss) income excluding interest expense, income taxes, depreciation and amortization, share-based compensation, employer payroll taxes on share-based compensation and other unusual and/or infrequent costs (i.e., impairment, restructuring and other expenses, acquisition-related expenses, loss on debt extinguishment and other income, net), which we do not consider in our evaluation of ongoing operating performance.

We define Adjusted EBITDA as a percent of net sales as adjusted EBITDA as defined above divided by net sales realized in the respective period.

We define Pro Forma Adjusted Net (Loss) Income as net (loss) income excluding (i) pro forma adjustments to interest expense for all periods presented as if our IPO and the resulting paydown of all outstanding debt had occurred at the beginning of each period presented, (ii) share-based compensation and employer payroll taxes on share-based compensation which have disproportionately impacted select periods presented as certain awards had catch-up vesting conditions triggered by the IPO, (iii) certain other unusual and/or infrequent costs (i.e., impairment, restructuring and other expenses, acquisition-related expenses, loss on debt extinguishment), which we do not consider in our evaluation of ongoing operating performance but including (iv) incremental costs of being a public company estimated for the periods presented during which the Company was not yet public and (v) the pro forma income tax expense resulting from the above adjustments to net income.

We define Pro Forma Adjusted Net (Loss) Income per Diluted Share as pro forma adjusted net income as defined above divided by the weighted average shares that would have been outstanding if our IPO had occurred at the beginning of each period presented.

We define Pro Forma Net Sales and Pro Forma Adjusted EBITDA as Net Sales and Adjusted EBITDA as if all five acquisitions had occurred at the beginning of the period presented.