Fighting the Feds, Round Two: Harborside vs. the IRS Industry threatened as nation’s model dispensary attacked over obscure tax code, 280E OAKLAND, Calif., Jun 04, 2016 (GLOBE NEWSWIRE via...

This article marks the end of this series’ emphasis on income tax. After introducing section 280E’s confiscatory effect, identifying the need for cannabis enterprise to maximize cost of goods...

I finished Part 2 of this series emphasizing section 280E’s principle force. Section 280E does not universally bar illegal commercial enterprises from deducting necessary and ordinary business expenses. Rather,...

Last week I introduced the conflict between federal income tax law and state-sanctioned cannabis enterprises here and here. In brief, the Internal Revenue Code (“Code”) section 280E proscribes state-sanctioned...

Mike Parnes, Attorney at Barth Daly LLP With the recent legalization of recreational cannabis sales in Alaska, Colorado, Oregon, and Washington, the writing is on the wall for the...

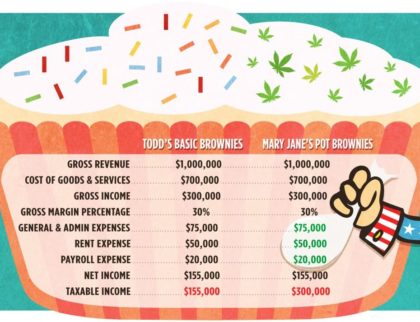

This comparison shows how a marijuana bakery can’t claim federal deductions a typical bakery can claim. Items in green cannot be deducted. (Image courtesy of wweek.com) The long lines and eager...