Riposte Capital Calls on Leading Cannabis Licensed Producer, HEXO Corp., to Initiate a Review of Strategic Alternatives

- Despite Enviable Assets, Contracts and Strong Balance Sheet, HEXO Trades at Deep Discount

- Riposte Looks Forward to a Dialogue Leading to Constructive Action

NEW YORK, Sept. 6, 2018 /PRNewswire/ — Riposte Capital, LLC, the second largest public shareholder of HEXO Corp. (“HEXO”), a leading Canadian cannabis Licensed Producer (formerly called Hydropothecary Corp.), has sent the following letter from Khaled Beydoun, Riposte Capital’s Managing Partner and Portfolio Manager, and Ryan Price, a Partner and the firm’s Director of Research, to HEXO’s Chief Executive Officer and Board of Directors:

VIA ELECTRONIC AND OVERNIGHT MAIL

September 5, 2018

Dear Sebastien and Members of the HEXO Corp. Board of Directors,

As the second largest shareholder in HEXO Corp., we are writing to reiterate to you the concern we have expressed previously about the severely depressed valuation of HEXO in spite of significant positive milestones and developments that management and the Board have accomplished this year. Though we have appreciated and look forward to continuing our dialogue, its pace of late has lagged the rapidly changing industry dynamics, and a catalyst has become necessary.

We – and, we are confident, other like-minded shareholders – believe your success in establishing enviable assets and contracts for HEXO has not translated to success in earning an appropriate equity price and multiple from the investment community for the company’s considerable existing and potential value. Moreover, the stock suffers from poor research coverage and investor awareness, a late listing to the TSX, no US listing, and an investor relations effort that needs significant improvement.

At a time of rapid development in the industry, with participants racing for scale, capital is a strategic asset. In our view, promptly addressing and remedying the company’s severe and unwarranted equity discount is essential to its competitive position. Taking decisive action to dramatically lower the company’s cost of capital, and thereby unleash its growth potential, should be the Board and management’s highest priority, and should be addressed at the next scheduled Board meeting.

We believe HEXO has the highest revenue visibility in the sector, due to your SAQ contract – the industry’s largest and longest government contract, worth more than $1bn in sales over 5 years and potentially $100mm of annual EBITDA contribution by year 3. Furthermore, you are one of two companies in the sector to have a formal agreement with a large alcohol company, in the form of your recently announced joint venture with Molson Coors Brewing Company. The other company with an alcohol partnership is Canopy Growth Corporation, which now has a market capitalization of over $23bn. This compares to HEXO’s market capitalization of just $1bn. We believe HEXO’s Molson Coors JV alone could be worth multiples of the current market capitalization of HEXO today.

We believe a conservatively calculated current intrinsic value for HEXO is $18 per share, based on a sector average multiple of 30x 2020 EV/EBITDA (current average trading multiple of the top 10 Canadian Licensed Producers by market capitalization) and the Molson Coors JV, to which we ascribe a modest $500mm vs. the implied $12bn in market capitalization being ascribed to Canopy from the Constellation deal (under the same methodology).

Yet HEXO trades at an EV/EBITDA multiple of just 8.1x 2020 consensus EBITDA – a mere fraction when compared to Tilray at 93.8x, Canopy 89.2x, Aurora at 27.2x, Cronos at 23.7x and Aphria at 19.5x.

Meanwhile HEXO has:

- The largest government guaranteed contract (in size) with the longest duration (5 years) in the sector;

- One of the strongest balance sheets (22.4% of market cap in cash); and

- The industry’s lowest cost production thanks to energy prices in Quebec (about 1/4th the cost compared to the rest of country), and labor expense (a minimum wage that is 33% below the Canadian national average).

Without a doubt, HEXO has the potential to be one of the market leaders in the cannabis sector based on its:

- Strength of management;

- Product suite;

- Research & Development and Innovation Pipeline;

- One of a kind partnership with Molson Coors; and

- Its leading position in Quebec.

We see it as a testament to your team’s operational acumen, as a producer, that Molson Coors indicated that they had conducted thorough due diligence on the sector, met with other much larger competitors, and ultimately selected HEXO based on shared culture and corporate values, a science-based approach with continuity of supplies, innovation pipeline, and track record. That all being said, HEXO still suffers from a low multiple and share price, which is critically important, as it significantly hampers the company in the race for global growth and expansion.

As significant shareholders we encourage management and the Board to act decisively at the next scheduled Board meeting to initiate a review of strategic alternatives to maximize shareholder value, which include (but are not limited to):

1) Engaging with any interested buyers of the company at a significant premium to the current share price. In light of the extreme valuation differentials that are now evident between HEXO and peers, HEXO would still be accretive on 2020 EBITDA if multiples of the current share price were offered.

2) Taking the company private, now that the financing markets are open to the sector and banks are providing leverage, and doing so in a manner that would permit us to maintain our existing ownership percentage in the company.

3) A meaningful direct investment from Molson Coors to fund growth and further strengthen the company’s relationship with a major alcohol player. In lieu of your pending proposal to issue warrants with a $6 strike, consider a direct placement for up to 20% of the equity at current levels in order to underpin the balance sheet and solidify distribution partnership.

4) A no-premium, accretive merger with a comparably-sized LP that can add further geographic diversification, scale, international opportunities, and medical expertise.

Given the company’s depressed valuation, the competitive implications that flow directly from remedying your undervalued share price and inflated cost of capital, and the ongoing commitment from the Board and management to maximize shareholder value, the company’s prior public position of completely taking a potential sale off the table should be reconsidered.

We look forward to your response and prompt action.

Sincerely,

/s/ Khaled and Ryan

Riposte Capital

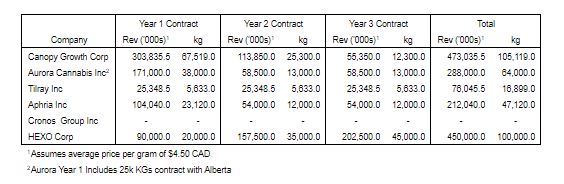

APPENDIX:

Announced Contract Wins by Canadian LPs

All figures in Canadian dollars, except as otherwise noted

Canadian LP Valuation Comps