Summary

- Sunset Island Group (OTC: SIGO) is a recent reverse-merger that purports to be a startup cannabis producer in California

- Over 99% of the float was sold at $0.00275 per share to a single entity ten months ago, though the stock now trades 596X higher, at $1.64

- Management has ties to another failed cannabis penny stock, 1PM Industries (OTC: OPMZ)

- The company, with minimal sales and cash of just $2876 with lots of debt, has raised $11,000 equity capital to date but has an effective registration statement to sell 20mm shares at $0.10, a 94% discount to the current price

- The current market cap of $82mm is unrealistic

Sunset Island Group (OTC: SIGO), relatively new as a cannabis stock, was one of the most actively-traded stocks in the sector last week following press release issued on August 15th and 17th as well as an 8-K filing on August 16th, all discussed below. The stock more than doubled during the week, ending at $1.64, with a market cap of $82mm (based on 50.037,710 fully-diluted shares), has increased by 681% so far in August and 1267% since June 30th.

A review of the history of the company, the people involved and its financials suggests that the stock is likely wildly overvalued. The mechanism for the stock’s potential decline ahead is clearly in place, and investors should approach SIGO with caution.

The First Dumping of Shares

SIGO is a penny stock with a long trading history that caught my attention in late 2016 when it filed an S-1 registration statement with the SEC. Until then, the company had never filed with the SEC, but it had previously filed with OTC Markets, with the last report having been in early 2011. For several years, it had traded with a “stop’ sign at OTC Markets after failing to provide financial information. The November filing, which followed a 1:10,000 reverse split in October, was amended in December and then amended again on January 5th. This S-1 went effective with the SEC on January 20th.

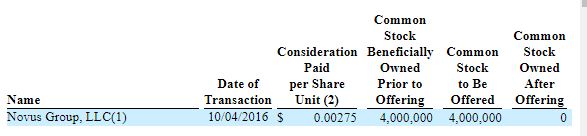

This first S-1 permitted the sale of 4mm shares of SIGO. The shares were held by Brian Weigel of Novus:

According to the footnotes:

- Mr. Brian Weigel, an US resident and citizen exercises the sole voting and dispositive powers with respect to the shares of the Registrant’s common stock owned of record and beneficially by Novus Group.

- The above-referenced shares were obtained as part of the reverse merger between the Company and Battle Mountain Genetics. The Novus Group invested $11,000 into Battle Mountain Genetics for 4,000 shares which were exchanged for 4,000,000 shares of the Company as part of the reverse merger.

With the registration statement going effective, Weigel was free to sell shares that he had acquired for just $0.00275 per share. At that time and to this day, there were 50.31771mm shares outstanding. The 46mm shares, held by insiders T.J. Magallanes, CEO, and Valerie Baugher, CFO, were not permitted to be sold yet. This left Weigel with 99.99% of the float in his ownership.

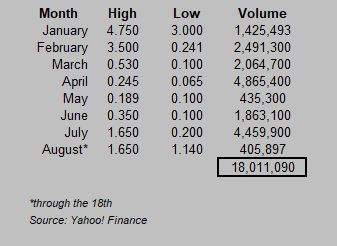

Since the effective date, the stock has had the following monthly trading range and volume:

So far in 2017, over 18mm shares have traded, with the very lowest price at $0.065. In its first few weeks of trading, over 1.4mm shares trades at a minimum of $3.00. The ability of Weigel of Novus Group, LLC to easily sell its shares of a company with limited operating experience and weak financials, as demonstrated below, is a red flag, compounded by the lack of information about the individual, who isn’t mentioned in any SEC filing over the past decade. His company, though, was acquired by publicly-traded 1PM Industries (OTC: OPMZ) in February, which I discuss further below.

There is no proof that Weigel has sold the shares (or at what price), though clearly he has done so based on the volume of trading. Sadly, the company received almost nothing for these shares ($11,000).

Background on the Company

The S-1 provided some initial information on the company, including biographies of its management team, a review of its financial condition and its plan of business. It also included this description of the company:

On October 17, 2016, the Company entered into an Agreement whereby the Company acquired 100% of Battle Mountain Genetics, Inc., which was incorporated in the State of California on September 29, 2016. Battle Mountain Genetics was the surviving Company and became a wholly owned subsidiary of Sunset Island Group. At the time of the merger, Sunset Island had no operations, assets or liabilities. On October 20, 2016, the acquisition closed and under the terms of the Agreement Battle Mountain Genetics was the surviving entity. The Company selected October 31 as its fiscal year end. The Company’s executive 4325 Glencoe Ave Ste C9-9903, Marina Del Rey, CA 90292.

The address provided is a U.S. Postal Service facility, which is not usually a good sign! No address was provided, though the filing also suggested that the company is headquartered in Oakland. SIGO now claims to be headquartered in San Clemente (most recent S-1). Subsequently, the executive address changed to 555 N. El Camino Real #A418, San Clemente, CA 92672, which is a UPS storefront.

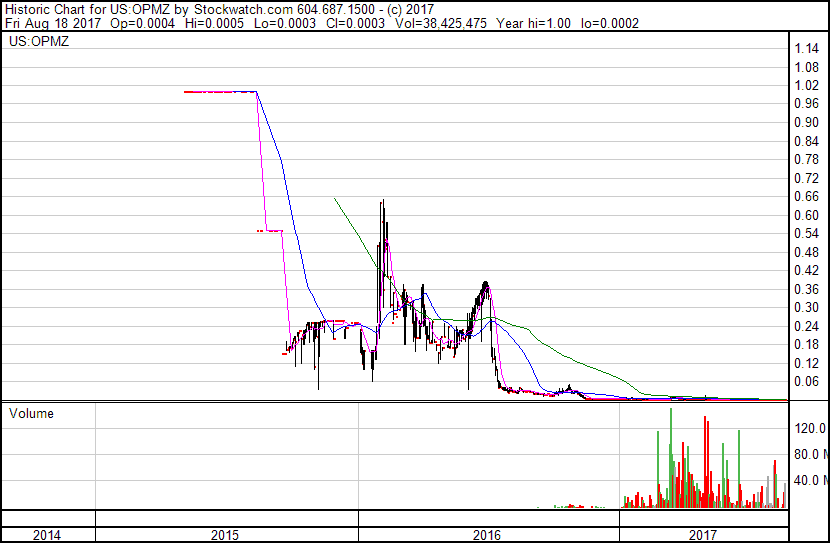

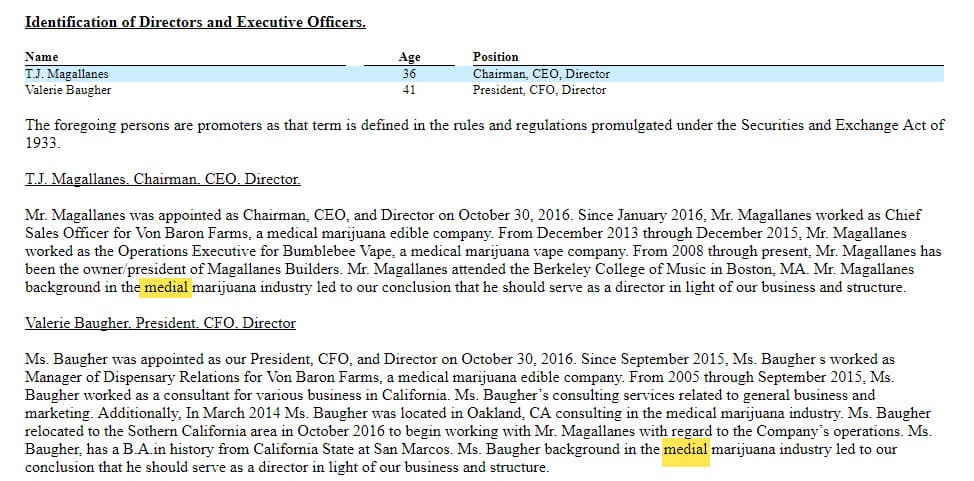

The two officers, CEO T.J. Magallanes and CFO Valerie Baugher, were the other two shareholders listed in the S-1, at 36.8mm and 9.2mm shares, respectively. The combined 46mm shares represent 92% of the shares of SIGO, with Weigel’s 4mm shares representing almost the entire balance. Both execs worked formerly at Von Baron Farms, though it isn’t mentioned in the SEC filing that Von Baron Farms was part of publicly-traded 1PM Industries (OTC: OPMZ). It’s no wonder, as OPMZ was one of the worst penny stock disasters the cannabis industry has seen, with the stock trading from over $0.60 per share in early 2016 to $0.0045 by the end of the year, a loss of more than 99%.

Magallanes served as the Chief Sales Officer from January 2016. Baugher served as Manager of Dispensary Relations from September 2015. The bio also fails to mention her involvement with several other penny stocks, all connected to the person who controls OPMZ, Joseph Wade. OPMZ was highly promotional but never reported material sales despite all the hype. In the case of both executives, the company made a funny error in how it described their “medial marijuana” experience:

There has been a big shift in the SIGO business as it was originally represented. The SIGO S-1 described the business initially:

The Company’s principal line of business is consulting and advising clients that operate in the medical marijuana business by providing clients a licensed manufacturing facility to produce products such as oils and edibles. The Company is currently looking for a facility in the Oakland, California that would satisfy the Company’s needs. Currently, the Company is using space from its CEO in Oakland, CA at no charge. The Company currently has the ability to distribute products in 50 dispensaries throughout the state of California. The Company’s officers have sold products to the dispensaries over the past 5 years and are able to leverage this pre-existing relationship with the dispensaries to introduce client’s products to these dispensaries. Once a product is introduced to a dispensary they place an order. No other agreements would exist between the Company and the dispensary. The Company charges clients a fee to produce its products and will receive a commission on products sold through its network. In November 2016, the company planned on acquiring a C02 extraction machine to begin producing oils for the `Company’s clients. However, the Company expects the acquisition of the CO2 extraction machine to be completed in January 2017.

The way the company described itself, it was operating as a service provider. It also described itself this way in a press release issued on February 3rd, saying “The Company’s vision is to establish a fully integrated company that provides turnkey solutions to the medical cannabis industry. The Company’s main focus is on providing a licensed facility that companies can manufacture and produce their products.”

The Story Changes

SIGO had absolutely no material assets at 10/31/16, with cash of just $970 and no liabilities, and it had not yet generated revenue. Through the first half of the fiscal year ending 10/31/17, the company has still generated no revenue, but SIGO has seen a deterioration in the balance sheet, as seen in the 10-Q for the quarter ending 4/30/17:

- Assets of $16,876, including cash of $2,876 and a security deposit of $14,000, but liabilities of $130,308, including notes payable to a third party not related to the company by 12/31/18 fo $123,200 (and an additional $34,000 was borrowed after the quarter ended)

- Operating expenses and operating loss of $114,402, and $121,294 used to fund operations

- The purported acquisition of a CO2 extraction machine, expected to be completed by January, did not happen and wasn’t discussed in the filing

This doesn’t look like the balance sheet of a company worth $82mm:

The company also changed its prior business model, updating it to indicate that it is now a cultivator of cannabis:

Sunset Island Group, Inc. is a Colorado corporation. The Company’s principal line of business is the cultivation of medical cannabis. The Company has leased green house space in Northern California that has been approved for cannabis cultivation. The greenhouse is 12,000 square feet; however, the Company has filed permits to expand to 22,000 square feet. Additionally, the Company will be consulting and advising clients that operate in the medical marijuana business by providing clients a licensed manufacturing facility to produce products such as oils and edibles. However, the company is waiting for the State of California to finalize the licensing process and requirements for licensed manufacturing facilities.

The business model shift had been previously described in an 8-K filing from March 21st:

(1) The Company is filing permits in Northern California for up to 22,000 square feet of greenhouse space to begin its growing operations. The 22,000 square feet is expected to be able to generate up to 4,000 pounds of medical cannabis per year. The price per pound is currently $1,000 to $1,750. The Company expects the first harvest to occur in July/August 2017.

(2) The Company has completed the design of the label for its CBD/Hemp Dietary supplement and is expecting the website to be completed within the next 60 days.

(3) The Company has completed a private label deal with its supplier that includes products such as CBD/Hemp Energy Shot and CBD/Hemp Pain Reliving Cream. Pursuant to the deal, the supplier will produce, label, box the products and ship finished products to the Company. This alleviates the need for the Company to acquire equipment to manufacture the product and allows the Company to produce products in any necessary quantity that is required.

The company has never followed up on the supplement, nor has there been any announcement of a related website, though five months have now passed.

Management had also issued a press release on February 17th that mentioned the development of a CBD dietary supplement product by a “trained French Chef and with over 20 years’ experience in Product Development and Food Production and who also has developed products from their concept stage to national distribution that have generated over $100 million in sales.” It had previously disclosed this information in an SEC filing on February 13th and then also filed the press release as an 8-K filing four days later. To date, there has been no mention of progress with this endeavor.

Another odd announcement from the company with no subsequent follow up occurred on February 27th, when it issued an 8-K about a breakfast product:

On February 25, 2017, the Company began discussions to exclusively license and private label a breakfast product that has previously generated $20 million in sales. The product has been sold in over 3,000 stores including CostCo, WalMart, and Target. The Company is expecting to complete the license agreement within the next two weeks. Once the agreement is in place and a new label has been approved, the Company can begin selling the product into grocery stores and box stores throughout the United States.

Back to the business of cannabis, the company reported on April 4th that its operations could produce revenue of $4-7mm per year and that it would see its first harvest by July or August. SIGO then went pretty quiet for three months, providing no press releases or operational updates until right before it filed its 10-Q for the quarter ending 4/30 on June 16th. In an 8-K issued on June 9th, it announced that it was cancelling a 40:1 stock split because the transfer agent cost was too high. It also provided its first update in over two months:

On June 8, 2017, the Company uploaded photos of its greenhouse and grow operations onto its website. The photos can be found: https://www.sunsetislandgroup.com/pictures.

The Company expects to begin harvesting the first crop at the end of July 2017. The yield is expected to be between 100-200 pounds for the initial harvest and the company expects to harvest between 1,000 to 1,500 pounds over the next 12 months.

SIGO management started discussing operations again publicly at a much quicker pace on July 20th, the timing of which is quite interesting, as I explain below:

- 7/20: Press release about its first harvest and its expansion plans

- 8/01: Press release about being “in the process of securing multiple cultivation agreements in order to facilitate expansion plans” and that it would be “sharing more about this incredible opportunity with investors on or before August 15th.”

- 8/07: Press release about a monthly dividend it decided to implement (with what?) and its expectation that the harvest would yield $158K in sales from 8/1-8/14

- 8/10: 8-K saying “From August 1, 2017 through August 7, 2017, the Company generated approximately $140,400 from 117 pounds harvested.”

- 8/15: Press release indicating that the Magallanes and Baugher would be locking up their shares for three years

- 8/16: 8-K about continuing discussions with the landlord about the leasing of additional space and an invitation to the public to tour its facilities on October 18th

- 8/17: Press release about certification from Envirocann

- 8/18: 8-K indicating the two officers would now convert their common shares to preferred shares

- 8/18: Additional 8-K suggesting that the dividend rate will be shared by 8/23 and that there is still no final agreement with its landlord to expand

Selling Shares at $0.10 (The Stock is at $1.64)

The company is throwing a lot of info at potential investors on topics like dividends it can’t likely pay and big expansion plans. Why? This is the most interesting part of the SIGO story: The company is trying to sell shares at $0.10.

The effort began on June 26th, when it filed the second S-1, just ahead of all of the increased public communication. It filed an amended S-1 on July 17th and a the final amended S-1 on July 28th, which went effective on 8/7, the day the company started talking about the potential dividend.

The S-1 permits the company to sell 20mm shares:

We are offering for sale a maximum of 20,000,000 shares of our Common Stock in a self-underwritten offering directly to the public at a price of $0.10 per share. There is no minimum number of shares that we must sell in our direct offering, and therefore no minimum amount of proceeds will be raised. No arrangements have been made to place funds into escrow or any similar account. Upon receipt, offering proceeds will be deposited into our operating account and used to conduct our business and operations. We are offering the shares without any underwriting discounts or commissions. The purchase price is $0.10 per share. If all 20,000,000 shares are not sold within 180 days from the date hereof, (which may be extended an additional 90 days in our sole discretion), the offering for the balance of the shares will terminate and no further shares will be sold. We intend for our Common Stock to be sold by our Officer and Director, T.J. Magallanes and Valerie Baugher. Such person will not be paid any commissions for such sales.

The S-1 clearly describes the company’s financial prospects: “We currently expect that our cash on hand, and our cash flow from operations will not be sufficient to meet our anticipated cash requirements. As such, the Company will need to raise additional capital through equity or debt transactions.” So, there is a motive and a means. It also still had the same “medial marijuana” mistake in the officer bios!

SIGO’s most recent quarter ended on July 31, and it is required to file its 10-Q by mid-September. With the disclosures to date, the company likely won’t be reporting any sales and will, consequently, show another operating loss. It has already disclosed at least some of the debt it issued in order to cover the loss, so the filing will provide a more complete balance sheet update and perhaps resolution to some of the unresolved issues, like the amount of space it will be leasing, the grocery store product and the CBD supplement. With the fiscal year ending on 10/31, the revenue that the company has disclosed from August won’t be reported officially until late January, when the 10-K annual filing is due.

In summary, SIGO is a startup run by people associated with another failed cannabis penny stock, OPMZ. The company is undercapitalized but has the ability to sell shares to the public, and it will likely do so. It has become highly promotional, talking about big growth ahead despite not having the resources yet to pay for the necessary investments and also about paying a dividend at the same time as it describes itself as needing to raise additional capital to meet its anticipated cash requirements.

4mm newly minted shares representing over 99% of the float but acquired for just $11,000 ($0.00275 per share) ten months ago were registered to be sold and likely have been, enabling Brian Weigel of Novus Group LLC to pocket millions before Novus was acquired by OPMZ, the former employer of SIGO’sofficers .

This company is a questionable penny stock story with a market cap of $82mm. With a tight float and lots of hype, the stock has gone parabolic. One never knows how far momentum stock traders will push it, but, with SIGO ready to unload 20mm shares, which will increase the float by 5X over time, it’s not hard to imagine how this will end.

Bottom-Line:

SIGO appears to be extremely overvalued, a startup business that isn’t yet sustainable but is valued at $82mm. With a relatively small float, the number of shares that can trade compared to the total shares outstanding or the fully-diluted shares, which would include the convertible preferreds, SIGO has run up way beyond a valuation that can be justified by its economics. The company has been issuing very bullish statements since it finalized its ability to sell shares, and the stock price has run up dramatically. SIGO, in desperate need for funding, has a registration statement that allows it to sell shares, and it likely will, which will ultimately expand the tradable float and put significant pressure on the price over time. Caveat emptor!