![]()

Glass House Brands Reports Second Quarter 2022 Financial Results

- SoCal Farm first harvest was in May, and Glass House single month July production was almost equal to output for all of Q2

- Record low quarterly cost per pound of $158 at Casitas and Padaro farms in Q2¹

- Net cash used in operating activities was $7.8 million, a 50% sequential improvement compared to Q1 2022

- Glass House is poised to nearly triple its revenue run rate to $200M+ by 2023²

- Glass House has entered into an agreement to buy Natural Healing Center’s flagship Grover Beach dispensary

- Announcing a preferred equity offering of US$26.5 million

- Conference Call to be Held August 11, 2022 at 5:00 p.m. ET

Second Quarter 2022 Highlights

(Unless otherwise stated, all results and dollar references are in U.S. dollars)

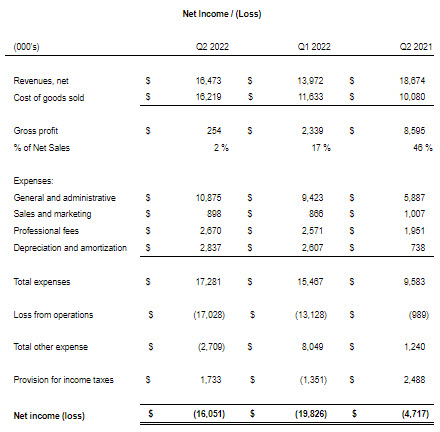

- Net Sales of $16.5 million decreased 12% from $18.7 million in Q2 2021 and increased 18% sequentially from $14.0 million in Q1 2022.

- Gross Profit was $0.3 million compared to $8.6 million in Q2 2021 and $2.3 million in Q1 2022.

- Gross Margin was 2%, compared to 46% in Q2 2021 and 17% in Q1 2022.

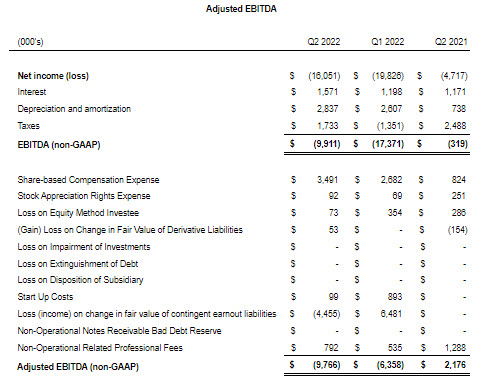

- Adjusted EBITDA³ was $(9.8) million, compared to $2.2 million in Q2 2021 and $(6.4) million in Q1 2022.

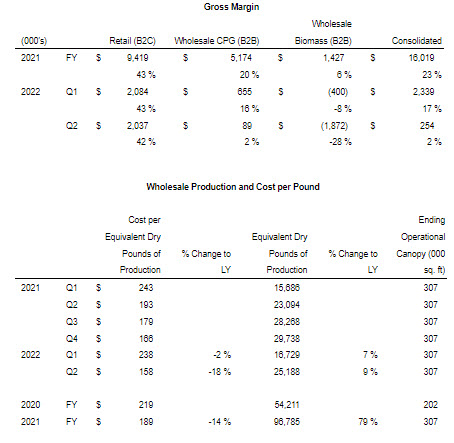

- Cost per Equivalent Dry Pound of Production¹,⁴ was $158 at Casitas and Padaro farms, a decrease of 18% compared to Q2 2021 and down 34% sequentially versus Q1 2022.

- Equivalent Dry Pound Production was 25,188 pounds, up 9% year-over-year and 51% sequentially.⁴

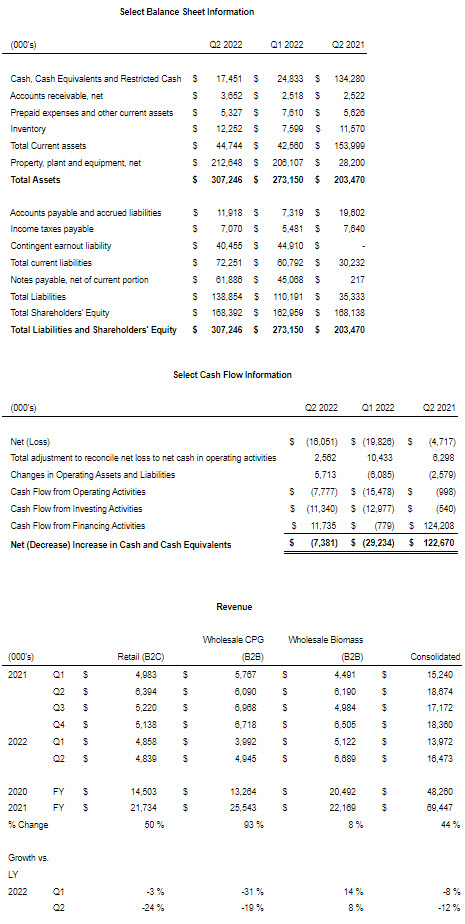

- Cash balance was $17.5 million at quarter-end compared to $24.8 million at Q1 2022 quarter end.

LONG BEACH, Calif. and TORONTO, Aug. 11, 2022 /CNW/ – Glass House Brands Inc. (“Glass House” or the “Company”) (NEO: GLAS.A.U) and (NEO: GLAS.WT.U) (OTCQX: GLASF) and (OTCQX: GHBWF), one of the fastest-growing, vertically integrated cannabis companies in the U.S., today reported financial results for its second quarter ending June 30, 2022.

Management Commentary

“We continued to make solid progress against our strategic growth priorities during the second quarter, “stated Kyle Kazan, Chairman and CEO of Glass House Brands, “The initial harvest from our SoCal farm was completed in late May followed by the first sales of cannabis grown at the facility in June, both well ahead of schedule and significantly faster than the previous ramp up of our Casitas and Padaro farms. Over the past few years, our Casitas and Padaro farms have established a strong reputation for consistently growing high quality cannabis at a low cost. So, I can’t emphasize enough how thrilled we are that the SoCal farm is already producing cannabis with a higher and more consistent quality than the Casitas and Padaro farms. In addition, it has shown particular promise at growing high quality genetics at extremely close to indoor quality. Volume has ramped quickly and in July we produced 22,000 pounds of biomass across all three facilities, compared to a total of 25,000 pounds in the entire second quarter.”

“In April, we closed the acquisition of the PLUS Products business, becoming the first California operator with top five brands in both flower and edibles.⁵ We are now the only edibles company that controls the process from plant to product, and our marketing team is already developing products that leverage our unique ability to make self-grown strain-specific products. We are swiftly integrating PLUS into our organization and in the short few months since closing, it has been accretive to our financials and shown potential to be a strong contributor to Glass House’s overall cash flow generation. We expect to realize synergies in distribution of both Glass House Farms and PLUS in the second half of this year and we have major product innovations planned for the fourth quarter.”

“Our aggressive retail expansion also remains firmly on track and we are on pace to have at least 11 dispensaries by year-end 2022, up from three just over a year ago when we started our life as a public company. We closed our acquisition of the remaining 50% equity stake in The Pottery Dispensary in July and expect to open three new Farmacy locations in the fourth quarter. In May, we announced the acquisition of three Natural Healing Center (“NHC”) dispensaries and we are moving forward on closing these acquisitions. In addition, we are very happy to announce that we have agreed to acquire Natural Healing Center’s flagship Grover Beach store for $15.9 million, with $8.1m of the purchase price in assumed debt, $7.7 million in stock and $0.1 million in cash net of working capital. The Grover Beach store is the crown jewel of NHC’s dispensaries and netted US$16m in revenues in 2021. It is one of only four total dispensaries in Grover Beach and is the No. 1 taxpayer in the city, given its high sales volume and strong cash flow generation. The deal multiple based on the annualized EBITDA of the Grover Beach store in the first half of 2022 is 4.8x.⁶”

We are poised to almost triple our revenue run rate to $200 million by 2023². Our competitive position remains strong as we continue to leverage the efficiency of our model to deliver high-quality cannabis at the lowest cost of production.

Kyle Kazan, Chairman and CEO of Glass House Brands

Kyle Kazan, Chairman and CEO of Glass House Brands

We are announcing today a new preferred equity financing to provide additional capital to solidify our balance sheet and we expect to be free cash flow positive by the first quarter of next year, excluding capital expenditures for facility expansion.

Second Quarter 2022 Operational Highlights

- Glass House Brands Completes Acquisition of PLUS, a Leading California Edibles Brand

- Glass House Brands to Acquire Remaining Equity, Property Ownership in The Pottery Dispensary

- Glass House Brands to Acquire Three Natural Healing Center Dispensaries

- Glass House Brands Completes First SoCal Harvest Ahead of Schedule

Subsequent Events

- Glass House Brands Completes the Acquisition of the Remaining Equity Ownership in The Pottery Dispensary

Media Highlights

- Cannacribs Episode – Largest High Tech Cannabis Green House in USA: Glass House Farms

Preferred Equity Offering of $26.5 million

Glass House is announcing a private placement of preferred equity shares (the “GHB Preferred Shares”) with a target raise of approximately $26.5 million. We intend to use $10 million of the proceeds to retire the bridge loan from WhiteHawk, and the remainder for working capital, including cap ex to complete the buildout of the new Farmacy stores. Glass House currently has received $10.7 million in cash-in-hand and signed agreements, and additional commitments of $8.7 million for a total of $19.4 million of GHB Preferred Shares. Additionally, the Company will convert the existing $23.5 million of preferred equity issued by the Company’s subsidiary, GH Group Inc. in 2021 into the GHB Preferred Shares to create a $50 million series. The Company currently has commitments to convert $22.5 million of the $23.5 million of existing GH Group preferred equity. Holders of the GHB Preferred Shares will be entitled to a 20% dividend which gradually increases to 25% by year four. The dividend will be paid quarterly with 10% in cash and the additional amount accruing to the principal. In addition, with each $10 of preferred equity investment, the holder will receive 2 warrants of Glass House, each warrant being exercisable to acquire one share of Glass House at a price of $5 for a term of 5-years following issuance. The first closing of the preferred equity share offering, subject to the approval of the NEO Exchange, is expected to occur by the end of August 2022. A final close is targeted for thirty to sixty days thereafter.

The management team is confident this incremental capital will provide the necessary runway to reach free cash flow positive operations in early 2023, excluding expansion capex. Despite the continued difficult market conditions, we are reaffirming this guidance.

Q2 2022 Financial Results Discussion

Total revenue for Q2 2022 was $16.5 million, a 12% decline versus Q2 2021 and 18% sequential growth versus Q1 2022.

Wholesale revenue of $6.7 million increased 8% versus Q2 2021 and grew 31% sequentially versus Q1 2022. We sold almost 20,000 lbs which is 38 percent more equivalent dry weight in Q2 this year than last year. Demand for Glass House-grown product is strong and inventories are low. The increase in weight available for sale was driven by a 9 percent increase in production versus last year and additional weight available to sell due to lower than anticipated need for biomass for CPG sales. Average pricing was 13 percent lower than last year but would have been much lower if our greenhouses hadn’t produced a much higher percentage of flower this quarter than the same quarter last year.

Retail revenue in Q2 of $4.8 million was flat to Q1, which was slightly below overall market growth of 1%. On a year-on-year basis, retail revenue was down 10% year-over-year on a normalized basis, excluding the $1 million loyalty program true-up in Q2 2021.

CPG revenue jumped 24% sequentially but decreased 19% from last year. Glass House CPG business is mainly in the flower category and is being impacted by declines in the cannabis market. The quarter also includes about 2 months of PLUS edibles revenue of $1.7 million which helped comparisons to prior periods. During the quarter, significant progress was made cleaning up aged inventory and re-balancing strain management issues that impacted sales in Q1 and Q2. This came at the price of heavy discounting, resulting in the level of discounting reaching 41 percentage points of gross sales, versus the prior 4 quarters of about 10%. Cleaner inventory to start Q3 should reduce markdowns to levels closer to other recent quarters.

Gross profit was $0.3 million, or 2%, compared to $8.6 million, or 46%, in Q2 2021 and $2.3 million, or 17% in Q1 2022. Our Q2 2022 gross margin when compared to our Q1 2022 gross margin was negatively impacted by two major factors. The first was the high level of CPG markdowns within the quarter, which hurt revenue and margin by $1.7 million. During the quarter, Wholesale spent $2.2M of start-up expenses related to the commencement of commercial operation at the SoCal farm.

General and Administrative expenses were $10.9 million, compared to $5.9 million in the prior year period or $9.4 million in Q1 2022. The $1.5 million sequential increase is primarily attributable to a $1.1 million increase in stock compensation, and salary and benefits related to the PLUS acquisition and $0.2 million associated with the increased cost of cannabis licenses. The full integration of PLUS will occur mainly during the 3rd quarter. Most of the SG&A expenses from PLUS employees will be eliminated, with the exception of those related to the sales team.

Sales and marketing expenses were $0.9 million, compared to $1.0 million in the prior year period and were flat compared to Q1 2022.

Professional fees were $2.7 million, compared to $2.0 million in the prior year period and $2.6 million in Q1 2022. In Q2 2022, increased legal fees due to acquisitions and deal-related costs were offset by a reduction in accounting fees related to year-end audit expenses in Q1 which did not occur in Q2.

Depreciation of $2.8 million compared to $0.7 million in the prior year period and $2.6 million in Q1 2022. Very little of the CapEx spending in the quarter was placed into service.

Adjusted EBITDA²,³ loss widened by $3.4 million to $9.8 million in the second quarter compared to a loss of $6.4 million in Q1 2022. The major impact was from gross margin, which fell to 2 percent from 17 percent in the first quarter of 2022.

As of June 30, 2022, the Company had $17.5 million in cash including $3 million of restricted cash. This was down from $24.8 million in Q1 2022. Net cash used in operating activities was $7.8 million, a 50% sequential improvement compared to Q1 2022, reflecting effective management of working capital. Capex was $7.6 million during Q2 2022, a sequential decline of 41% compared to Q1 2022 as phase one of the Camarillo facility was largely completed.

In addition, we are providing the following new guidance for the balance of the year. Glass House has a long-term target of reducing cultivation cost to $100 per pound.1,4 The management team is now ready to provide projections for the average cost of production across all 3 farms of $150 per pound for Q3 and $125 per pound for Q4 of this year.1,4 Please note that the SoCal farm is completing its ramp up through Q3. The projected improvement to $125 per pound in Q4 represents a 25% reduction from Q4 last year.1,4

Lastly, with the commercial startup of the SoCal farm and full quarter of PLUS edibles, we are providing revenue guidance for Q3. In Q3, we expect to achieve revenues of between $27M and $30M for the quarter which is a 64% to 82% increase vs. Q2 this year. This assumes the wholesale pricing we are currently experiencing in Q3 remains constant through the balance of the quarter. Our Q4 revenue target is $50M and assumes Q4 wholesale pricing remains consistent with Q3 and includes revenue from our NHC acquisition as well as a partial quarter for our new Farmacy stores.

As we are almost halfway through the third quarter, our primary focus is on execution for the balance of the year. We have the pieces already in place to achieve $200M2 in run rate revenue as we exit the year and to become free cash flow positive in early 2023. With our base business, SoCal’s 630,000 square feet of cultivation joining our existing 307,000 square feet of cultivation, the addition of PLUS, 4 Natural Healing Center dispensaries, and 4 new Farmacy dispensaries, we are well positioned to be successful in California and to deliver against our financial goals.

Financial results and analyses will be available on the Company’s investor relations website (https://ir.glasshousegroup.com/) and SEDAR (www.sedar.com).

Unaudited Q2 2022 Financial and Operational Metrics

Conference Call

Conference Call

The Company will host a conference call to discuss the results on today, August 11, 2022 at 5:00 p.m. Eastern Time.

Webcast: Click here

Dial-In Number: 1-888-664-6392

Conference ID: 77242140

Replay: 1-888-390-0541

Replay Code: 242140 #

(replay available until 12:00 midnight Eastern Time Thursday, August 18, 2022)

Non-GAAP Financial Measures

Glass House defines EBITDA as Net Loss (GAAP) adjusted for interest and financing costs, income taxes, depreciation, and amortization. Adjusted EBITDA is defined as EBITDA excluding share-based compensation, stock appreciation rights expense, loss (income) on equity method investments, change in fair value of derivative liabilities, change in fair value of contingent liabilities, acquisition related professional fees, and non-operational start-up costs.

EBITDA and Adjusted EBITDA are presented because management has evaluated the financial results both including and excluding the adjusted items and believe that the supplemental non-GAAP financial measures presented provide additional perspective and insights when analyzing the core operating performance of the business. Such supplemental non-GAAP financial measures are not standardized financial measures under U.S. GAAP used to prepare the Company’s financial statements and might not be comparable to similar financial measures disclosed by other companies and, thus, should only be considered in conjunction with the GAAP financial measures presented herein.

The Company has provided a table above that provides a reconciliation of the Company’s net loss to Adjusted EBITDA for the three months ended June 31, 2022 compared to three months ended June 31, 2021 and three months ended December 31, 2021.

Footnotes and Sources:

- Cost per Equivalent Dry Pound of Production, is the application of a subset of Costs of Goods Sold for cannabis biomass production (including all expenses from nursery and cultivation to curing and trimming – the point at which product is ready for sales as wholesale cannabis or to be transferred to CPG) applied to the Company’s metric of dry production which includes all dry production (flower, smalls and trim) plus equivalent dry weight for wet weight and fresh frozen that is not converted into dry goods by the Company.

- Company has the potential to achieve monthly revenues that annualize to $200 million. The statement assumes the following in potential incremental revenues from each source: 1) Annualized Camarillo (SoCal farm) Phase I wholesale biomass sales of $50-75 million; 2) The four NHC dispensaries generate annualized revenues of $40 million; 3) The Pottery generates annualized revenues of $3.9 million; 4) PLUS maintains its pre-acquisition annualized revenues of $14 million per year; 5) The Isla Vista, Santa Ynez, and Eureka dispensaries are opened on schedule in Q4 2022 and that they produce an average of $5 million in annual revenues each; 5) That the Company’s core business that existed prior to the addition of these new revenue sources is able to deliver $69 million in revenue.

- EBITDA and Adjusted EBTIDA are non-GAAP financial measures. Please see “Non-GAAP Financial Measures” herein for further information and for a reconciliation of Adjusted EBITDA to the closest GAAP measure.

- Includes all dry production (flower, smalls and trim) plus equivalent dry weight for wet weight and fresh frozen not converted into dry weight by the Company.

- BDS Analytics

- Based on seller’s unaudited management prepared financials.

About Glass House

Glass House is one of the fastest-growing, vertically integrated cannabis companies in the U.S., with a dedicated focus on the California market and building leading, lasting brands to serve consumers across all segments. From its greenhouse cultivation operations to its manufacturing practices, from brand-building to retailing, the company’s efforts are rooted in the respect for people, the environment, and the community that co-founders Kyle Kazan, Chairman and CEO, and Graham Farrar, President, instilled at the outset. Through its portfolio of brands, which includes Glass House Farms, Forbidden Flowers, and Mama Sue Wellness, Glass House is committed to realizing its vision of excellence: outstanding cannabis products, produced sustainably, for the benefit of all. For more information and company updates, please visit www.glasshousebrands.com and https://ir.glasshousebrands.com/contact/email-alerts/.