![]()

Glass House Brands Reports Third Quarter 2021 Financial Results

- Net Revenue Increased 29% Year-over-Year

- Completed acquisition of 5.5 million square foot cultivation facility, positioning company for considerable future growth

- Conference Call to be Held November 11, 2021, at 5:00 p.m. ET

LONG BEACH, Calif and TORONTO, Nov. 11, 2021 /CNW/ – Glass House Brands Inc. (“Glass House” or the “Company”) (NEO: GLAS.A.U and GLAS.WT.U) (OTCQX: GLASF and GHBWF), one of the fastest-growing, vertically integrated cannabis companies in the U.S., today reported financial results for its third quarter ending September 30, 2021 (“Q3 2021”).

Third Quarter 2021 Highlights

(Unless otherwise stated, all results are in U.S. dollars)

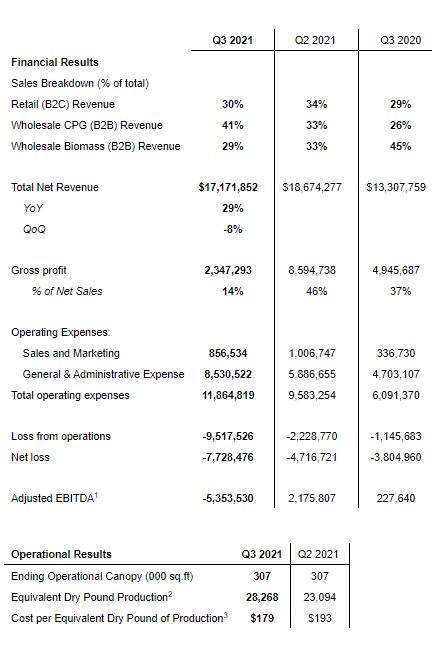

- Net Sales increased 29% to $17.2 million from $13.3 million in Q3 2020 and declined 8% sequentially from $18.7 million in Q2 2021.

- Glass House Farms, the Company’s house cannabis brand, was the No. 1 ranked brand by sales in California in Q3 2021 and is the No. 2 brand YTD Q3 2021 according to BDSA.

- Equivalent Dry Pound Production was a record high 28,268 pounds in Q3 2021, up 30% year-over-year and 22% sequentially.

- Cost per Equivalent Dry Pound of Production fell 7% sequentially to $179.

- Gross Profit was $2.3 million compared to $4.9 million in Q3 2020 and $8.6 million in Q2 2021.

- Gross Margin of 14% compared to 37% in Q3 2020, and 46% in Q2 2021.

- Adjusted EBITDA1 of $(5.4) million compared to $0.2 million in Q3 2020 and $2.2 million from Q2 2021.

- Adjusted EBITDA Margin1 was (31)% compared to 2% in Q3 2020, and 12% in Q2 2021.

- YTD Q3 2021 Net Sales grew 63% to $51.1 million from 31.3 million in Q3 2020.

- YTD Q3 2021 Adjusted EBITDA1 was $(2.6) million from (1.4) million in Q3 2020.

- Cash balance was $28.9 million at quarter-end.

Management Commentary

Kyle Kazan, Glass House Chairman and CEO, stated: “The California market is now in the long-awaited process of commoditization, and this will be difficult for all who have operations in the Golden State. It is a necessary step in the maturation of the market and similar to what happened in Colorado, Washington and Oregon. We are leaning into this period by focusing on significantly lowering our COGS through scale and automation at our newly purchased Camarillo facility as we believe that highest quality at the lowest production costs in California will be the big winner. It also should be noted that as a value investor for 30 years, challenging environments offer the most compelling acquisition opportunities. We are uniquely positioned in California to be a value add and, in many cases, a savior for struggling companies which would benefit from our vertically integrated platform.”

In spite of the market conditions, we executed on a number of key strategic objectives during the quarter, building on our solid foundation and strengthening our position as one of the leading companies in the world’s largest cannabis market.

Kyle Kazan, Glass House Chairman and CEO

Kyle Kazan, Glass House Chairman and CEO

We recently closed on our 5.5 million square foot SoCal cultivation facility, which provides us with the size and scale necessary to grow the highest quality craft cannabis with the lowest cost of production, and to do so in a sustainable, environmentally friendly manner.

Mr. Kazan added, “The California wholesale market faced considerable pricing challenges, as a result of overproduction in the third quarter. While we expect the weakness in pricing to persist in the near term, we have proven the strength of our efficient operating model and the ability of our team to navigate a rapidly changing industry. Our Glass House Farms brand was the top-selling cannabis flower brand in California in Q3 2021 according to BDSA, and we believe that the best operators, such as ourselves, will thrive despite the difficult market conditions.”

Mr. Kazan concluded, “We have also significantly strengthened our senior management team with the appointments of Mark Vendetti, as our new Chief Financial Officer, and Erik W. Thoresen as Chief Business Development Officer. With our expanding cultivation and production footprint, a market-leading brand portfolio, strengthened senior management team, and solid balance sheet, we anticipate ending 2021 on a strong footing, more ready than ever to execute on the growth opportunities ahead of us. All in all, this was a solid quarter for us in almost every aspect, but the temporary and very difficult market conditions dragged on our revenue, margins and EBITDA.”

Q3 2021 Financial and Operational Metrics

Third Quarter 2021 Operational Highlights

- Completed acquisition of 5.5 million square foot Southern California greenhouse facility

- Bird’s Eye View of the SoCal Greenhouse Facility

- Co-Signatory to the Weldon Project’s letter to U.S. President Biden urging a full pardon for all federal nonviolent marijuana offenders

- Appointed Mark Vendetti as Chief Financial Officer

- Appointed Erik W. Thoresen as Chief Business Development Officer

Subsequent Events

- Awarded the Cannabis & Tech Today “2021 Sustainable Leadership Award for Energy Use”

- Glass House Brands files suit against Element 7 to enforce transfer of contractually committed licenses

- Glass House Brands Appoints John Brebeck as Vice President of Investor Relations

Planned Participation in Broker and Industry Conferences

- November 16th – Jefferies Virtual West Coast Consumer Conference

- December 16th – CannaVest West Institutional Capital Forum

Revenue for the three months ended September 30, 2021 (“Q3 2021”), was $17.2 million, representing an increase of $3.9 million or 29% from $13.3 million for the three months ended September 30, 2020 (“Q3 2020”). The wholesale CPG business was the key engine of revenue growth, increasing 103%. It was driven primarily by the Glass House Farms brand which almost tripled in revenue compared to the prior year period. Successful marketing and distribution of the product, as well as a large increase in canopy under operation – mainly from the Company’s second greenhouse facility – supported the growth. Wholesale biomass revenue fell 18% despite a more than doubling of unit volume sales as flower wholesale prices fell by 48%, negatively impacting revenue by $4.1 million. Retail revenues increased by $1.4 million or 37% with the addition of a new dispensary which opened in Q1 2021.

Cost of goods sold in Q3 2021 was $14.8 million, an increase of $6.5 million, or 77%, compared with $8.4 million in Q3 2020. Q3 2021 gross profit was $2.3 million, representing a gross margin of 14%, compared with a gross profit of $4.9 million, representing a gross margin of 37% in Q3 2020. Cost of goods sold in Q3 2021 increased as a result of higher unit volume related to higher sales and inventory valuation adjustments that occurred in Q3 2021. Year-to-date gross margin of 32% in 2021 compares to a prior year gross margin of 38%. The drop in gross margin from 2020 to 2021 was driven by the previously mentioned $4.1 million drop in wholesale cannabis revenue due to lower wholesale cannabis prices.

Total operating expenses in Q3 2021 were $11.9 million, an increase of $5.8 million, or 95%, compared to total expenses of $6.1 million in Q3 2020. General and administrative expenses in Q3 2021 and Q3 2020 were $8.5 million and $4.7 million, respectively, an increase of $3.8 million, or 81%. The increase in general and administrative expenses is primarily attributed to stock-based compensation from going public, increased insurance costs, and costs to support operational expansion in the areas of cultivation, retail and corporate activities. Professional fees in Q3 2021 and Q3 2020 were $1.7 million and $0.4 million, respectively, an increase of $1.3 million, or 384%. Sales and marketing expenses in Q3 2021 and Q3 2020 were $0.9 million and $0.3 million, respectively, an increase of $0.5 million, or 154%. The increase in sales and marketing expenses is primarily attributed to the increase in the Company’s efforts related to digital media, consumer and retail education, brand events, and activations.

Q3 2021 adjusted EBITDA, a non-GAAP measure that excludes depreciation and amortization, interest expense, income taxes, share-based compensation, (income) loss on equity method investments, (gain) loss on change in fair value of derivative liabilities, acquisition-related professional fees, and loss on disposition of subsidiary was a loss of $5.4 million compared to $0.2 million in Q3 2020. The decrease in adjusted EBITDA was driven primarily by lower gross margin and higher operating expenses in the quarter. YTD Q3 2021 Adjusted EBITDA was $(2.6) million compared to $(1.4) million in Q3 2020.1

Cash and cash equivalents, were $28.9 million as of September 30, 2021, compared to $4.5 million as of September 30, 2020.

Financial results and analyses are available on the Company’s investor relations website (https://ir.glasshousegroup.com/) and SEDAR (www.sedar.com).

SoCal Cultivation Facility Update

Construction at the Company’s newly acquired cultivation facility located in Camarillo, California (the “SoCal Facility”) commenced in late September. Phase 1 of the construction includes approximately 500,000 square feet of nursery and propagation facility with ebb & flood systems to allow for efficient automated plant handling. Phase 1 will also include an approximately 900,000 square foot Kubo Ultra Clima high-efficiency greenhouse, adding approximately 600,000 square feet of new flower canopy to the Company’s existing operational footprint. In addition, the Company is constructing a processing center and a new distribution center to support Phase 1 of the SoCal Facility and the future retrofit of the four remaining greenhouses.

The Company is also moving ahead with the required licensing of the SoCal Facility, having already received Cannabis Zoning Clearance from the local municipality and having completed and submitted all California State license applications needed for Phase 1 operations. The Company expects cultivation activities to commence in the second quarter of 2022 and the first harvest and sale of cannabis from the facility to occur in the second half of 2022.

Retail Rollout Update

Glass House remains well-positioned to continue investing in and expanding its retail presence. The Company’s goal is unchanged: to operate the largest retail footprint in the state and to create exceptional retail experiences for its customers. In the coming months, the Company will remain focused on exploring new opportunities and potential targets to scale our retail network through a mix of acquisitions, new license wins, and partnerships. Glass House will also continue developing its 5 new licenses in Dunsmuir, Hesperia and Eureka (via E7), and in Santa Barbara (Glass House Brands licenses). We currently plan to brand all five of our new properties as Farmacy locations, and the Company expects to have them open before the end of Q2 2022. Glass House’s new Santa Barbara dispensaries will be in prime locations and are being designed to provide a fabulous customer experience. Regarding the E7 properties, Glass House is excited about Eureka, which extends its retail reach into the heart of the Emerald Triangle, and the Dunsmuir location, which is located on Main Street in a beautiful old bank building in a town that views the Company’s dispensary as an attractive addition to a downtown area in the midst of a revival.

Q4 2021 Outlook

Regarding the projections provided in the Outlook section of the Company’s listing prospectus dated May 6, 2021, filed at the time of the de-SPAC and listing, Glass House no longer expects to achieve the 2021 and 2022 revenue and profitability targets set at that time. Factors include the dramatic drop in cannabis pricing that has occurred in recent months, the delay in closing the purchase of the SoCal facility versus the Company’s original expectations, and the developments noted in its November 4th, 2021 press release regarding Element 7.

The Company anticipates Q4 2021 revenues to be flat to down slightly compared to Q3 2021 revenues of $17.2M. This outlook assumes that the current difficult operating conditions in California will remain unchanged at least through the end of the calendar year, with no improvement in Cannabis wholesale prices, as well as a continuation of the sequential trend from Q3 of flat to declining California retail sales. Regarding the operating outlook for 2022, Glass House plans to provide some basic guidance during its Q4 2021 results call, at which time the Company’s budgeting process for 2022 will be complete and Q1 2022 operating conditions in the California cannabis market will be known.

Conference Call

The Company will host a conference call to discuss the results on Thursday, November 11th, at 5:00 p.m. Eastern Time.

Date: November 11, 2021

Time: 5:00 p.m. ET

Webcast: Click Here

Dial-In Number: 1-(888)-664-6392

Conference ID: 49715794

Replay: 1-(888)-390-0541

Replay Code: 71579#

Available until 12:00 midnight Eastern Time Thursday, November 18, 2021

About Glass House

Glass House is one of the fastest-growing, vertically integrated cannabis companies in the U.S., with a dedicated focus on the California market and building leading, lasting brands to serve consumers across all segments. From its greenhouse cultivation operations to its manufacturing practices, from brand-building to retailing, the company’s efforts are rooted in the respect for people, the environment, and the community that co-founders Kyle Kazan, Chairman and CEO, and Graham Farrar, President, instilled at the outset. Through its portfolio of brands, which includes Glass House Farms, Forbidden Flowers, and Mama Sue Wellness, Glass House is committed to realizing its vision of excellence: outstanding cannabis products, produced sustainably, for the benefit of all. For more information and company updates, visit www.glasshousegroup.com.

Notes:

1. Refers to a non-GAAP financial measure or an additional line item or subtotal in financial statements. Please see the discussion and reconciliations of non-GAAP financial measures included under the heading “Non-GAAP Financial Measures” in the Company’s Management’s Discussion & Analysis for the Third Quarter ended September 30, 2021, which is available on the Company’s investor relations website (https://ir.glasshousegroup.com/) and on SEDAR at www.sedar.com.

2. Includes all dry production (flower, smalls and trim) plus equivalent dry weight for wet weight and fresh frozen not converted into dry weight.

3. Includes all expenses from nursery and cultivation to curing and trimming – the point at which product is ready for sales as wholesale Cannabis or to be transferred to CPG.