![]()

ScottsMiracle-Gro Announces Record Full Year Results as Fourth Quarter Sales Exceed Expectations in U.S. Consumer Segment

- U.S. Consumer segment sales increase 11% in fiscal 2021; decline 28% in Q4

- Full-year Hawthorne sales increase 39%, decline 2% in Q4 despite growth in the U.S.

- Full-year GAAP earnings of $9.03 per share; Q4 loss of $0.87 per share

- Non-GAAP adjusted full-year EPS of $9.23; Q4 adjusted loss of $0.82 per share

- Fiscal 2022 guidance: Non-GAAP adjusted EPS $8.50 to $8.90; sales growth 0 to 3%

- Company announces intent for share repurchases of $300 million in fiscal 2022

MARYSVILLE, Ohio, Nov. 03, 2021 (GLOBE NEWSWIRE) — The Scotts Miracle-Gro Company (NYSE: SMG), the world’s leading marketer of branded consumer lawn and garden as well as indoor and hydroponic growing products, today released record full year financial results driven by a company-wide sales increase of 19 percent and continued growth in all major operating segments.

The Company also established guidance for fiscal 2022 that includes non-GAAP adjusted earnings of $8.50 to $8.90 per share on company-wide sales growth of 0 to 3 percent, both of which will be aided by a second pricing action in the U.S. Consumer segment to mitigate commodity inflation. The Company also said it plans to repurchase up to another $300 million in shares during fiscal 2022.

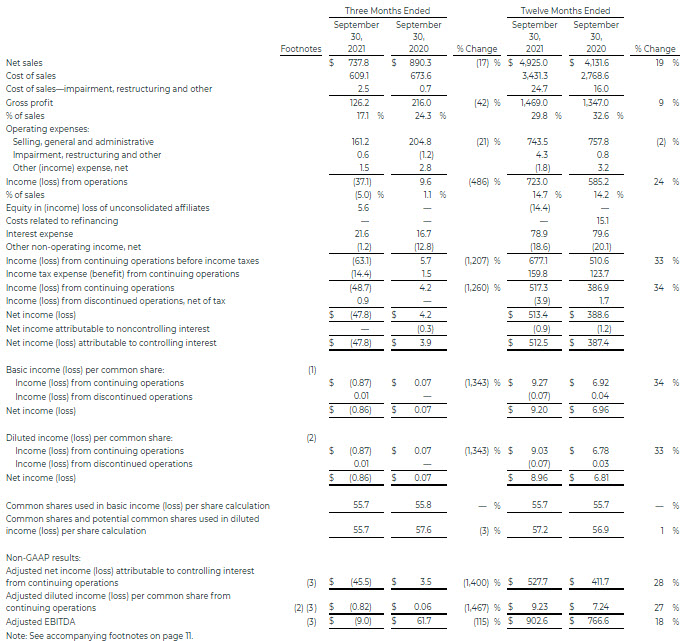

For the year ended September 30, 2021, company-wide sales increased 19 percent to a record $4.93 billion, compared with $4.13 billion a year earlier. GAAP earnings from continuing operations were $9.03 per diluted share, compared with $6.78 per diluted share in the prior year. Non-GAAP adjusted earnings, which are the basis of the Company’s guidance and exclude impairment, restructuring, and other non-recurring items, were $9.23 per diluted share compared with $7.24 per diluted share a year ago.

Company-wide sales in the fourth quarter declined by 17 percent to $737.8 million. The Company reported a GAAP loss in the quarter of $0.87 per share compared with earnings last year of $0.07 per diluted share. The adjusted loss in the quarter was $0.82 per share compared with earnings of $0.06 per diluted share a year ago.

“The continued engagement by consumers throughout the lawn and garden season drove full-year U.S. Consumer sales 11 percent higher on a full-year basis on top of last year’s 25 percent growth,” said Jim Hagedorn, chairman and chief executive officer. “Consumer purchases of our products at our largest retail partners – as measured in units – were up 6 percent for the full year, with growth in every major product category. When compared to 2019, consumer purchases are up 21 percent and suggest a level of consumer enthusiasm that we expect to carry into the 2022 lawn and garden season.

At Hawthorne, we continued to use our competitive advantages to drive 39 percent segment growth on a full-year basis despite a 2 percent decline in the fourth quarter. While we saw expected pressure on Hawthorne’s Q4 results due to a widely publicized over-supply of cannabis in California, sales of hydroponic supply products in the U.S. increased more than 10 percent on an apples-to-apples basis and we remain focused on the long-term opportunities to expand our leadership in this rapidly evolving industry.

Jim Hagedorn, chairman and chief executive officer

Jim Hagedorn, chairman and chief executive officer

“At Hawthorne, we continued to use our competitive advantages to drive 39 percent segment growth on a full-year basis despite a 2 percent decline in the fourth quarter. While we saw expected pressure on Hawthorne’s Q4 results due to a widely publicized over-supply of cannabis in California, sales of hydroponic supply products in the U.S. increased more than 10 percent on an apples-to-apples basis and we remain focused on the long-term opportunities to expand our leadership in this rapidly evolving industry.

“As we look to fiscal 2022, we have continued confidence in our strategy and ability to drive long-term shareholder value,” Hagedorn continued. “Certain macro issues beyond our control may present challenges we haven’t faced for a while, but I’m confident in our team’s ability to execute. We expect to continue pursuing acquisition opportunities throughout the year and remain committed to using our financial flexibility to return cash to shareholders. That is why, in addition to the $113 million of share repurchases in fiscal ’21, we plan to repurchase as much as another $300 million in 2022.”

Fourth quarter details

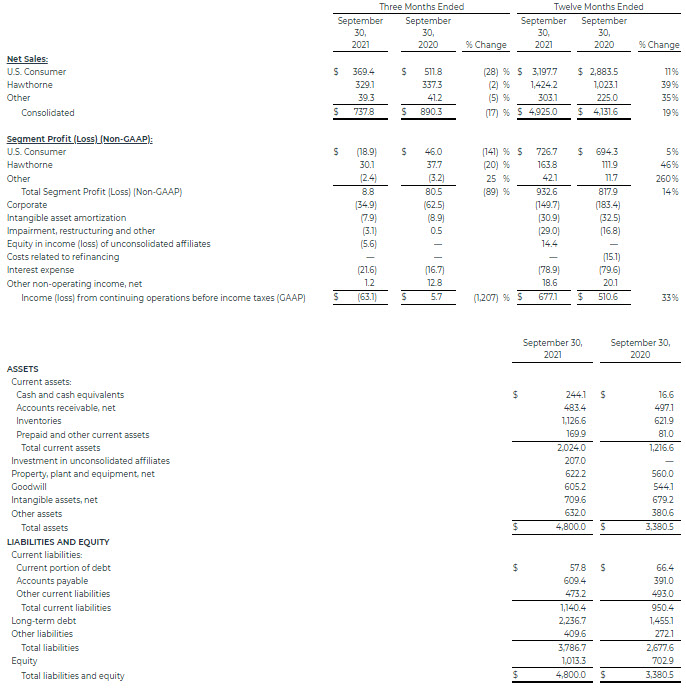

Company-wide sales declined 17 percent to $737.8 million. U.S. Consumer, which was facing a 92 percent growth comparison from fiscal 2020, decreased 28 percent to $369.4 million. Hawthorne sales declined 2 percent to $329.1 million due to declines in the European and Canadian businesses. Due to a shift in the fiscal calendar, the fourth quarter had six fewer days than a year ago which negatively impacted the quarter by $54 million. Excluding the calendar impact U.S. Consumer sales declined 23 percent and Hawthorne sales increased 5 percent, including a more than 10 percent increase in sales of hydroponic products in the U.S.

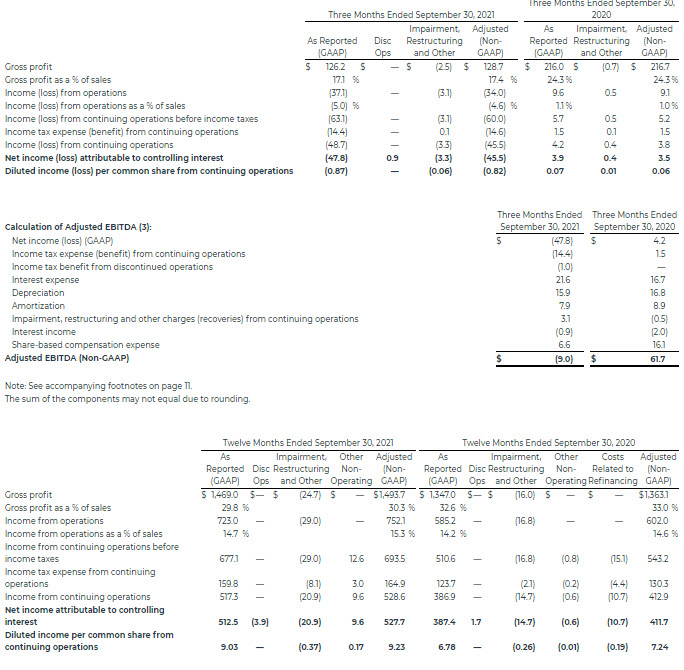

For the quarter, the GAAP and non-GAAP adjusted gross margin rate was 17.1 percent and 17.4 percent, respectively, compared with 24.3 percent in the prior year. The decline was driven primarily by a year-over-year decline in fixed cost leverage as well as higher distribution costs. Pricing and decreased promotional activity net of increased material costs helped to offset the decline.

“Commodity prices were a headwind throughout fiscal ’21 but were partially offset in the quarter by price increases in our U.S. Consumer segment that took effect in August,” said Cory Miller, chief financial officer. “We have communicated to our retail partners that we will take additional pricing actions effective in January as we continue to battle higher costs from urea, resin, grass seed and other commodities.”

SG&A was $161.2 million, a 21 percent decrease from 2020, due to lower accruals for annual incentive compensation payments and lower corporate spending. Interest expense increased nearly $5 million on a year-over-year basis to $21.6 million. The Company said its leverage ratio at the end of the quarter was approximately 2.7 times average debt-to-EBITDA.

The Company reported a loss from continuing operations of $48.7 million, or $0.87 per share, compared with income from continuing operations of $4.2 million, or $0.07 per diluted share. The non-GAAP adjusted loss in the quarter, which excluded impairment, restructuring, as well as other non-recurring items, was $45.5 million, or $0.82 per share, compared with adjusted net income of $3.5 million, or $0.06 per diluted share in 2020. The fourth quarter is historically a loss quarter for ScottsMiracle-Gro due to the seasonal nature of the U.S. Consumer segment. The Company’s unprecedented fourth quarter growth in fiscal 2020 allowed it to report a profit in the period for the first time in 15 years.

Fiscal 2021 details

Company-wide sales on a full year basis increased 19 percent to $4.93 billion compared with $4.13 billion a year ago. Sales in the U.S. Consumer segment increased 11 percent, to $3.20 billion due to strong consumer demand throughout the year. Hawthorne sales increased 39 percent to $1.42 billion due to strong growth in all category segments in both emerging and legacy markets.

The GAAP gross margin rate on a year-to-date basis was 29.8 percent. The non-GAAP adjusted rate was 30.3 percent. These compare with 32.6 and 33.0 percent, respectively, last year. The decrease was driven primarily by higher-than-expected distribution and input costs, as well as unfavorable segment mix. The decline was partially offset by improved fixed cost leverage.

SG&A was $743.5 million, a 2 percent decrease from 2020, due to lower accruals for annual and long-term incentive compensation. Interest expense was essentially flat at $78.9 million.

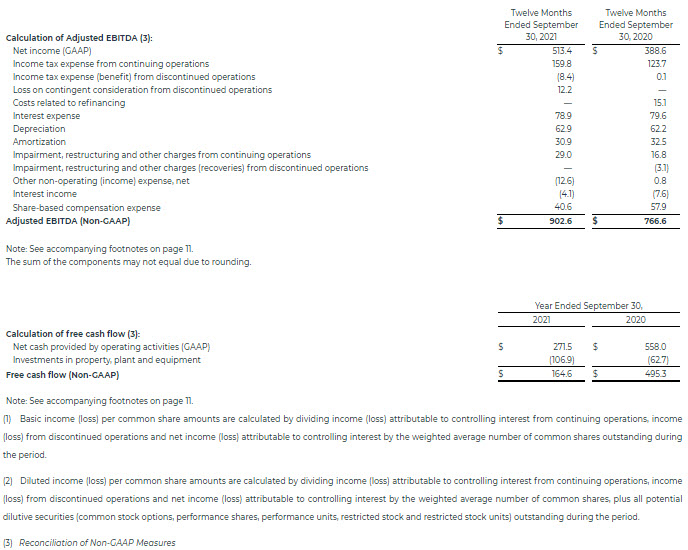

GAAP income from continuing operations was $517.3 million, or $9.03 per diluted share, compared with $386.9 million, or $6.78 per diluted share in the prior year. Non-GAAP adjusted earnings, which excluded impairment, restructuring, as well as other non-recurring items, were $527.7 million, or $9.23 per diluted share, compared with $411.7 million, or $7.24 per diluted share a year ago.

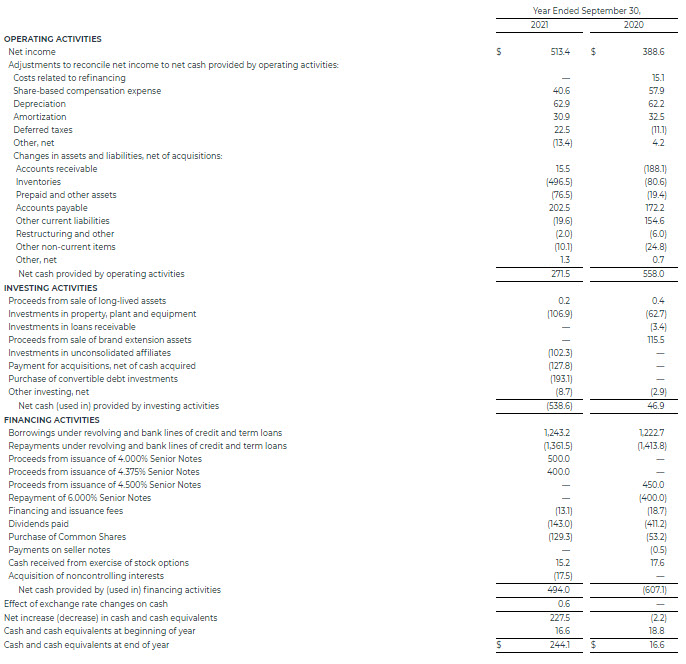

“Free cash flow, defined as operating cash flow minus capital expenditures, was $165 million and was driven lower year-over-year by key investments in CapEx and building and maintaining record-high inventory levels to provide superior service to our customers,” Miller said. “Those headwinds were somewhat offset as we worked with several of our major vendors and partners on extended payment terms.”

Fiscal 2022 outlook

The Company established guidance for fiscal 2022 based on expected company-wide sales growth of 0 to 3 percent. It expects U.S. Consumer segment sales to be 0 to minus 4 percent. Hawthorne sales are expected to grow approximately 8 to 12 percent with most of the growth expected in the second half of the year.

Non-GAAP adjusted earnings per share are anticipated to be in a range of $8.50 to $8.90 with the gross margin rate declining approximately 100 to 150 basis points. SG&A is expected in a range of minus 6 to plus 1 percent. Interest expense is expected to increase approximately $25 million.

“In our U.S. Consumer segment, high-single digit pricing actions are expected to offset potential unit volume declines,” Miller said. “While continued levels of consumer engagement and retailer support remain encouraging, we are taking a prudent approach to setting our full year volume assumptions and establishing guidance.

“At Hawthorne, we expect the current over-supply of cannabis to put negative pressure on our growth rate through the rest of the calendar year and into the second quarter, at which point we anticipate a more normal growth rate.”

Management will outline its 2022 expectations in more detail during its scheduled conference call with the investment community at 9 a.m. Eastern time today.

Conference Call and Webcast Scheduled for 9 a.m. ET Today, November 3

The Company will discuss results during a webcast and conference call today at 9:00 a.m. Eastern Time. Conference call participants should call 1-866-337-5532 (Conference Code: 7088156). A live webcast of the call will be available on the investor relations section of the Company’s website at http://investor.scotts.com. An archive of the webcast will remain available for at least 12 months. In addition, a replay of the call can be heard by calling 1-888-203-1112. The replay will be available for 15 days.

About ScottsMiracle-Gro

With approximately $4.9 billion in sales, the Company is one of the world’s largest marketers of branded consumer products for lawn and garden care. The Company’s brands are among the most recognized in the industry. The Company’s Scotts®, Miracle-Gro® and Ortho® brands are market-leading in their categories. The Company’s wholly owned subsidiary, The Hawthorne Gardening Company, is a leading provider of nutrients, lighting and other materials used in the indoor and hydroponic growing segment. For additional information, visit us at www.scottsmiraclegro.com.

The Company divides its operations into three reportable segments: U.S. Consumer, Hawthorne and Other. U.S. Consumer consists of the Company’s consumer lawn and garden business located in the geographic United States. Hawthorne consists of the Company’s indoor and hydroponic gardening business. Other primarily consists of the Company’s consumer lawn and garden business in geographies other than the United States. In addition, Corporate consists of general and administrative expenses and certain other income and expense items not allocated to the business segments. This identification of reportable segments is consistent with how the segments report to and are managed by the chief operating decision maker of the Company.

During the first quarter of fiscal 2021, the Company changed its internal organization structure such that AeroGrow International, Inc. (“AeroGrow”) is now managed by and reported within the U.S. Consumer segment. Within the U.S. Consumer segment, AeroGrow is integrated into the Company’s overall direct to consumer focus and strategy. AeroGrow was previously managed by and reported within the Hawthorne segment. The prior period amounts have been reclassified to conform with the new organization structure.

The performance of each reportable segment is evaluated based on several factors, including income (loss) from continuing operations before income taxes, amortization, impairment, restructuring and other charges (“Segment Profit (Loss)”), which is a non-GAAP financial measure. Senior management uses Segment Profit (Loss) to evaluate segment performance because they believe this measure is indicative of performance trends and the overall earnings potential of each segment.

The following tables present financial information for the Company’s reportable segments for the periods indicated:

Use of Non-GAAP Measures

To supplement the financial measures prepared in accordance with U.S. generally accepted accounting principles (“GAAP”), the Company uses non-GAAP financial measures. The reconciliations of these non-GAAP financial measures to the most directly comparable financial measures calculated and presented in accordance with GAAP are shown in the tables above. These non-GAAP financial measures should not be considered in isolation from, or as a substitute for or superior to, financial measures reported in accordance with GAAP. Moreover, these non-GAAP financial measures have limitations in that they do not reflect all the items associated with the operations of the business as determined in accordance with GAAP. Other companies may calculate similarly titled non-GAAP financial measures differently than the Company, limiting the usefulness of those measures for comparative purposes.

In addition to GAAP measures, management uses these non-GAAP financial measures to evaluate the Company’s performance, engage in financial and operational planning and determine incentive compensation because it believes that these measures provide additional perspective on and, in some circumstances are more closely correlated to, the performance of the Company’s underlying, ongoing business.

Management believes that these non-GAAP financial measures are useful to investors in their assessment of operating performance and the valuation of the Company. In addition, these non-GAAP financial measures address questions routinely received from analysts and investors and, in order to ensure that all investors have access to the same data, management has determined that it is appropriate to make this data available to all investors. Non-GAAP financial measures exclude the impact of certain items (as further described below) and provide supplemental information regarding operating performance. By disclosing these non-GAAP financial measures, management intends to provide investors with a supplemental comparison of operating results and trends for the periods presented. Management believes these measures are also useful to investors as such measures allow investors to evaluate performance using the same metrics that management uses to evaluate past performance and prospects for future performance. Management views free cash flow as an important measure because it is one factor used in determining the amount of cash available for dividends and discretionary investment.

Exclusions from Non-GAAP Financial Measures

Non-GAAP financial measures reflect adjustments based on the following items:

- Impairments, which are excluded because they do not occur in or reflect the ordinary course of the Company’s ongoing business operations and their exclusion results in a metric that provides supplemental information about the sustainability of operating performance.

- Restructuring and employee severance costs, which include charges for discrete projects or transactions that fundamentally change the Company’s operations and are excluded because they are not part of the ongoing operations of its underlying business, which includes normal levels of reinvestment in the business.

- Costs related to refinancing, which are excluded because they do not typically occur in the normal course of business and may obscure analysis of trends and financial performance. Additionally, the amount and frequency of these types of charges is not consistent and is significantly impacted by the timing and size of debt financing transactions.

- Discontinued operations and other unusual items, which include costs or gains related to discrete projects or transactions and are excluded because they are not comparable from one period to the next and are not part of the ongoing operations of the Company’s underlying business.

The tax effect for each of the items listed above is determined using the tax rate and other tax attributes applicable to the item and the jurisdiction(s) in which the item is recorded.

Definitions of Non-GAAP Financial Measures

The reconciliations of non-GAAP disclosure items include the following financial measures that are not calculated in accordance with GAAP and are utilized by management in evaluating the performance of the business, engaging in financial and operational planning, the determination of incentive compensation, and by investors and analysts in evaluating performance of the business:

Adjusted gross profit: Gross profit excluding impairment, restructuring and other charges / recoveries.

Adjusted income (loss) from operations: Income (loss) from operations excluding impairment, restructuring and other charges / recoveries.

Adjusted income (loss) from continuing operations before income taxes: Income (loss) from continuing operations before income taxes excluding impairment, restructuring and other charges / recoveries and costs related to refinancing.

Adjusted income tax expense (benefit) from continuing operations: Income tax expense (benefit) from continuing operations excluding the tax effect of impairment, restructuring and other charges / recoveries and costs related to refinancing.

Adjusted income (loss) from continuing operations: Income (loss) from continuing operations excluding impairment, restructuring and other charges / recoveries and costs related to refinancing, each net of tax.

Adjusted net income (loss) attributable to controlling interest from continuing operations: Net income (loss) attributable to controlling interest excluding impairment, restructuring and other charges / recoveries, costs related to refinancing and discontinued operations, each net of tax.

Adjusted diluted income (loss) per common share from continuing operations: Diluted net income (loss) per common share from continuing operations excluding impairment, restructuring and other charges / recoveries and costs related to refinancing, each net of tax.

Adjusted EBITDA: Net income (loss) before interest, taxes, depreciation and amortization as well as certain other items such as the impact of the cumulative effect of changes in accounting, costs associated with debt refinancing and other non-recurring or non-cash items affecting net income (loss). The presentation of adjusted EBITDA is intended to be consistent with the calculation of that measure as required by the Company’s borrowing arrangements, and used to calculate a leverage ratio (maximum of 4.50 at September 30, 2021) and an interest coverage ratio (minimum of 3.00 for the twelve months ended September 30, 2021).

Free cash flow: Net cash provided by (used in) operating activities reduced by investments in property, plant and equipment.

For the three and twelve months ended September 30, 2021, the following items were adjusted, in accordance with the definitions above, to arrive at the non-GAAP financial measures:

- The COVID-19 pandemic has had, and continues to have, an impact on financial markets, economic conditions, and portions of the Company’s business and industry. The Company has actively addressed the pandemic’s ongoing impact on its employees, operations, customers, consumers, and communities, by, among other things, implementing contingency plans, making operational adjustments where necessary, and providing assistance to organizations that support front-line workers. During the three and twelve months ended September 30, 2021, the Company incurred costs of $2.5 million and $25.0 million, respectively, in the “Cost of sales—impairment, restructuring and other” line in the Condensed Consolidated Statements of Operations and incurred costs of $0.6 million and $4.2 million, respectively, in the “Impairment, restructuring and other” line in the Condensed Consolidated Statements of Operations associated with the COVID-19 pandemic primarily related to premium pay. These direct and incremental costs were excluded from the Company’s non-GAAP financial measures because they are not comparable from one period to the next and are not expected to be part of the ongoing operations of the Company’s underlying business.

- On December 31, 2020, pursuant to the terms of the Contribution and Unit Purchase Agreement between the Company and Alabama Farmers Cooperative, Inc. (“AFC”), the Company acquired a 50% equity interest in the Bonnie Plants business through a newly formed joint venture with AFC (“Bonnie Plants, LLC”) in exchange for a cash payment of $100.7 million, forgiveness of the Company’s outstanding loan receivable with AFC and termination of the Company’s options to increase its economic interest in the Bonnie Plants business. The Company’s loan receivable with AFC, which was previously recognized in the “Other assets” line in the Condensed Consolidated Balance Sheets, had a carrying value of $66.4 million on December 31, 2020 and the Company recognized a gain of $12.5 million during the first quarter of fiscal 2021 to write-up the value of the loan to its closing date fair value in the “Other non-operating income, net” line in the Condensed Consolidated Statements of Operations. The Company’s interest in Bonnie Plants, LLC had an initial fair value of $202.9 million and is recorded in the “Investment in unconsolidated affiliates” line in the Condensed Consolidated Balance Sheets. The Company’s interest is accounted for using the equity method of accounting, with the Company’s proportionate share of Bonnie Plants, LLC earnings subsequent to December 31, 2020 reflected in the Condensed Consolidated Statements of Operations.

For the three and twelve months ended September 30, 2020, the following items were adjusted, in accordance with the definitions above, to arrive at the non-GAAP financial measures:

- Costs associated with the COVID-19 pandemic during the three months ended September 30, 2020 were not material. During the twelve months ended September 30, 2020, the Company incurred costs of $15.5 million in the “Cost of sales—impairment, restructuring and other” line in the Condensed Consolidated Statements of Operations and incurred costs of $3.9 million in the “Impairment, restructuring and other” line in the Condensed Consolidated Statements of Operations associated with the COVID-19 pandemic primarily related to premium pay.

- During the three and twelve months ended September 30, 2020, the Company received zero and $2.6 million, respectively, from the final settlement of escrow funds related to a previous Hawthorne acquisition that was recognized in the “Impairment, restructuring and other” line in the Condensed Consolidated Statements of Operations.

- On October 23, 2019, the Company redeemed all of its outstanding 6.000% Senior Notes for a redemption price of $412.5 million, comprised of $0.5 million of accrued and unpaid interest, $12.0 million of redemption premium, and $400.0 million for outstanding principal amount. The $12.0 million redemption premium was recognized in the “Costs related to refinancing” line in the Condensed Consolidated Statements of Operations during the first quarter of fiscal 2020. Additionally, the Company had $3.1 million in unamortized bond issuance costs associated with the 6.000% Senior Notes, which were written-off during the first quarter of fiscal 2020 and were recognized in the “Costs related to refinancing” line in the Condensed Consolidated Statements of Operations.

- The Company recognized insurance recoveries of zero and $1.5 million related to the previously disclosed legal matter In re Morning Song Bird Food Litigation during the three and twelve months ended September 30, 2020, respectively, in the “Income (loss) from discontinued operations, net of tax” line in the Condensed Consolidated Statements of Operations.

Forward Looking Non-GAAP Measures

In this earnings release, the Company presents its outlook for fiscal 2022 non-GAAP adjusted EPS. The Company does not provide a GAAP EPS outlook, which is the most directly comparable GAAP measure to non-GAAP adjusted EPS, because changes in the items that the Company excludes from GAAP EPS to calculate non-GAAP adjusted EPS, described above, can be dependent on future events that are less capable of being controlled or reliably predicted by management and are not part of the Company’s routine operating activities. Additionally, due to their unpredictability, management does not forecast the excluded items for internal use and therefore cannot create or rely on a GAAP EPS outlook without unreasonable efforts. The timing and amount of any of the excluded items could significantly impact the Company’s GAAP EPS. As a result, the Company does not provide a reconciliation of guidance for non-GAAP adjusted EPS to GAAP EPS, in reliance on the unreasonable efforts exception provided under Item 10(e)(1)(i)(B) of Regulation S-K.