10-K season just came to an end for cannabis stocks. Actually, to be precise, extra innings came to an end, as the filings were due 03/31 for companies with years ending in December with the ability to extend to April 17th. One of the filings that caught my attention was Axim Biotechnologies (OTC: AXIM), which filed its 10-K yesterday along with many others who waited until the last minute.

AXIM’s stock had a tremendous 2016 and is up dramatically over the past year despite a recent decline from an all-time high in January:

The 10-K updated on the number of shares outstanding, and there are 52.57mm as of April 15th. Additionally, there are another 1mm shares of preferred shares that convert 1:1 to common, giving the company 53.57mm shares outstanding before considering the convertible notes ($1.85mm that converts at $0.2201 would add 8.4mm shares, while $216,100 convertible at $0.10 adds another 2.16mm shares for a total of 10.56mm shares). This gives the company a market cap of $712mm. Adding in those convertible notes would boost it to 64.13mm shares for a market cap of $853mm.

As of year-end, the company had assets of just $1.45mm but liabilities of $3.82mm. In 2016, sales fell from $49,139 in 2015 to just $47,059 as the company continues to struggle with marketing its CanChew CBD gum. It reported an operating loss of $3.76mm and a net loss of $5.8mm. The company used $1.29mm to fund its operations in 2016 and ended the year with just $713K in cash.

While the company is pursuing drug development, it spent only $235,579 on R&D in 2016, down 50% from the $571,455 it spent in 2015. For comparison, GW Pharma (NASDAQ: GWPH) spent $129mm in FY16 on R&D. Zynerba (NASDAQ: ZYNE) spent almost $17mm (and has a lower market cap than AXIM despite having Phase 2 trials funded and underway).

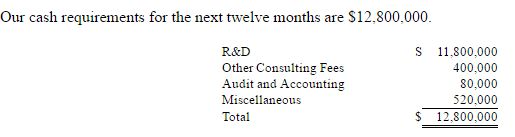

If this isn’t enough to give pause, consider that the company says it needs to raise $12.8mm over the next year:

The company has a market cap that is insane in my view and has been unable to raise money on reasonable terms to date. Holders of AXIM should expect substantial dilution, in my view, if the company is actually able to raise the $12.8mm it needs. If it can’t raise the money, then it surely isn’t worth over $700mm.