Comparing Cannabis Stocks? Beware of Biological Assets

How accounting complexities can skew true profitability

Guest post by Steven Looi and Michael Miller of Initiative Capital

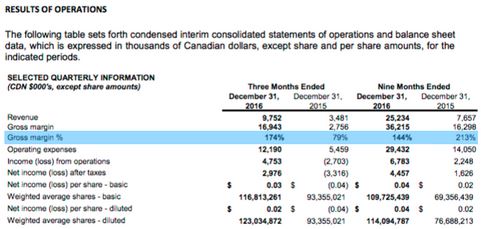

When Canopy Growth Corp. (TSX: WEED) reported their most recent earnings for the quarter ending December 31, 2016, they did something that was both ordinary for a cannabis producer and extraordinary for virtually any other company: They produced a gross margin above 100%. To be specific, they posted a gross margin of 173.74% by generating revenues of $9.752 million with an apparent gross profit of $16.943 million. If this seems confusing, the fact that Canopy posted a gross margin of 383.13% in one quarter in 2015 must really be a head-scratcher, after all, how is this even possible?

Accountants and analysts will tell you that no matter the price of which you sell something, you can only get so close to a gross margin of 100%. Even software companies with their de minimis product delivery costs don’t hit gross margins of 100%, let alone exceed them by a few hundred percentage points. This begs the question, how has Canopy, and more importantly, an entire industry worth billions found a way to seemingly defy financial gravity? Whether you are a current investor or considering adding a cannabis producer to your portfolio, the devil of accounting is in the details, and the devil’s name is IFRS.

Canada has no shortage of publicly traded licenced producers of cannabis including Aurora Cannabis Inc. (TSXV: ACB), Aphria Inc. (TSXV: APH), and Canopy, to name a few. Like Canopy, both Aurora and Aphria have reported historic gross margins in excess of 100%, with Aurora achieving a gross margin of 153.01% on their annual statements ending June 30th, 2016, while Aphria managed to hit a dizzying 499.34% gross margin for the quarter ending February 28, 2015. As it turns out, the source of these enormous gross margins has little to do with the pent-up demand for adult-use cannabis (although it is an indirect factor), but is primarily a result of the mandated accounting standards for Canadian public companies. Unlike US public companies that report their financials using US GAAP as set out by the Financial Accounting Standards Board (FASB), Canadian companies report their financials using International Financial Reporting Standards (IFRS) as set out by the International Accounting Standards Board (IASB). Though there are considerable differences between the two that go beyond the scope of this article, the root cause of financial oddities for cannabis producers comes from a section of IFRS, specifically IAS 41, that sets the accounting standards for agricultural activity and biological assets.

Under IAS 41, producers of cannabis are required to recognize the fair value of their biological assets (cannabis plants) less the cost to sell them, on their income statement prior to having sold the product or even lining up a potential purchaser. If this sounds completely absurd, I assure you, its because it is. What makes it even more challenging is that the fair value of a cannabis plant is something that changes as it grows, matures, and flowers, meaning that licenced producers need to constantly adjust this figure throughout the plant’s life cycle. Creating even more confusion is that IAS 41 does not dictate where on the income statement this recognition of fair value must occur.

Canadian cannabis producers seem to have set the standard of recognizing this fair value above the gross profit line, leading to the direct impact on gross margin noted earlier. However, companies like Bedrocan Cannabis Corp., which used to trade under (TSXV: BED) and is now part of Canopy, elected to recognize this fair value below the gross margin line. The reasons for the adoption of this early recognition policy could be an article unto itself, however, a key reason is that IAS 41 was heavily influenced by some of the largest agricultural producers that typically had captive markets for their produce (i.e. wheat, grain, corn) through co-ops and governments. They also had relatively reliable pricing information through established futures markets that allowed them to determine their crops’ fair value.

The implication for IAS 41 is that some of the traditional hallmark financial ratios used to analyze the performance and profitability of a company cannot necessarily be taken at face value from a cannabis producer’s income statement. Ratios linked to gross margins, EBITDA, operating income, net income, and even working capital are all impacted by what can be dramatic unrealized swings in the fair value of a company’s biological assets. More importantly, the source of these swings in biological assets will not always be readily apparent to an analyst or investor who takes a cursory look at the numbers. The primary reason that companies today are experiencing such dramatic increases in their biological assets is that they are ramping up production to meet both the rapid rise in demand from medical patients, (that grew from 75,166 to 98,360 between June 30 and September 30, 2016 representing a 30.77% increase over one quarter), and the anticipated adult use market.

This is not the whole story, however, and just because a company has an increase in their biological assets, it does not mean they are bringing new production capacity online. Reasons that a producer may document a considerable increase in their biological assets could include something as simple as refilling an existing grow room that was previously shut down or the timing of their grow cycle at the end of an accounting period.

Licenced producers are not just susceptible to increases in their biological asset values as the market grows; declines in fair values are also a reality that can create a prima facie impression of weak performance for an otherwise profitable company. Reasons for declines in biological asset values could range from a critical issue such as the outbreak of powdery mildew or spider mites that devastate a crop and require its culling, however, if could also be something as mundane as the timing of the crop cycle. Whether a swing is positive or negative, an overwhelming factor that controls the amplitude of these swings is the fair value equation that these companies adopt. Factors that influence these equations range from expected sales prices, per plant yield rates, attrition rates due to disease, and whether the head grower woke up in a good mood that morning. Ultimately, the unique fair value equation that is set by each company and susceptible to change over time as grow practices evolve and facilities expand represents a known unknown in the value swings of biological assets.

As the legal cannabis market evolves and investors look to select companies with best practices, they will need to be wary of how biological assets can impact some of the more conventional ratios on which they rely. Licenced producers have tried to help in this regard by providing investors with adjusted gross margin and EBITDA figures in their management discussion and analysis reports. Investors should be wary though and take note of what exactly is baked into each company’s ‘adjusted figures’ before making these comparisons as these are non-IFRS and non-GAAP metrics. Simply put, one company’s adjusted gross margin may not be the same as another company’s adjusted gross margin.

Finally, a critical consideration for investors is that the way biological assets are treated in Canada under IFRS varies considerably from how they are treated in the United States under US GAAP. The concept of initial fair value recognition does not exist under US GAAP, which instead uses the historical cost of the biological assets. The implication of this is that should a large publicly traded producer make their way to the major American exchanges, simply comparing their financials side-by-side with a Canadian producer will be insufficient, and necessary adjustments will have to be made before setting up a true comparison.

About the authors:

Michael Miller and Steven Looi are founding members of Initiative Capital, a cannabis venture fund based in Toronto, Canada.

Michael is a multi-disciplinary venture capitalist and a regular adviser to early-stage companies looking for guidance on valuation, raising capital, and long-term positioning. A frequent writer on the emerging cannabis industry, Michael’s writings can be found in leading trade and consumer publications.

Prior to co-founding Initiative Capital, Steven was an entrepreneur with international reach having launched and successfully exited from businesses in both China and Canada. With experience founding, operating, and managing software, pharma, and urban agricultural companies, Steven brings a multifaceted approach to the challenges of the cannabis industry. Steven has been a regular fixture at industry events in both Canada and the United States in his capacity as a cannabis angel for emerging companies.