![]()

- PLUS Acquisition Complete; Agreements in Place to Increase Glass House’s Projected California Dispensary Footprint to 10 Locations

- First Sale from 5.5 million sq. ft. SoCal Cultivation Facility Expected in June 2022

- Glass House has the potential to reach a revenue run rate of $200M+ within the next 12 months1

- Conference Call to be Held May 12, 2022 at 5:00 p.m. ET

LONG BEACH, Calif. and TORONTO, May 12, 2022 /CNW/ – Glass House Brands Inc. (“Glass House” or the “Company”) (NEO: GLAS.A.U) (NEO: GLAS.WT.U) (OTCQX: GLASF) (OTCQX: GHBWF), one of the fastest-growing, vertically integrated cannabis companies in the U.S., today reported financial results for its first quarter ending March 31, 2022.

First Quarter 2022 Highlights

(Unless otherwise stated, all results and dollar references are in U.S. dollars)

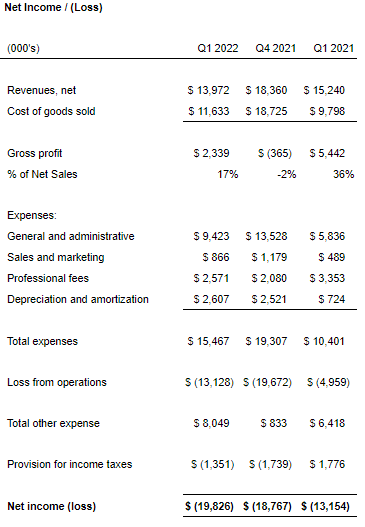

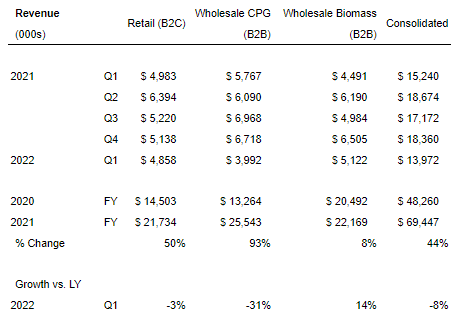

- Net Sales decreased 8% to $14.0 million from $15.2 million in Q1 2021 and declined 24% sequentially from $18.4 million in Q4 2021.

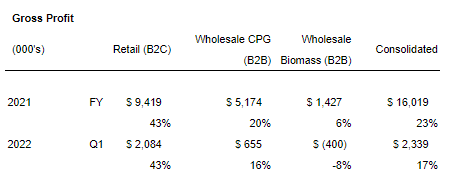

- Gross Profit was $2.3 million compared to $5.4 million in Q1 2021 and $(0.4) million in Q4 2021.

- Gross Margin was 17%, compared to 36% in Q1 2021 and (2)% in Q4 2021.

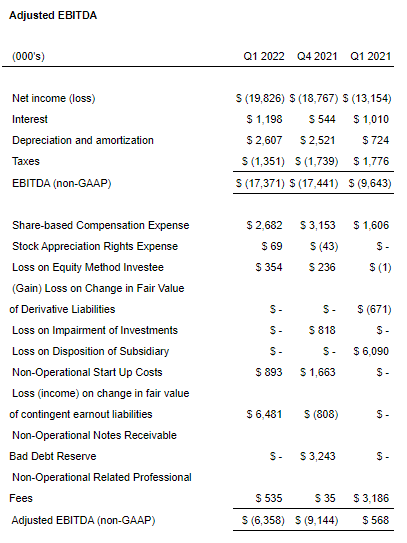

- Adjusted EBITDA2 was $(6.4) million, compared to $0.6 million Q1 2021 and $(9.1) million in Q4 2021.

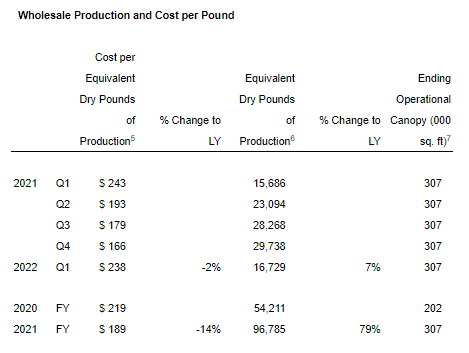

- Cost per Equivalent Dry Pound of Production decreased 2% versus the first quarter of last year to $238.

- Equivalent Dry Pound Production was 16,729 pounds, up 7% year-over-year.

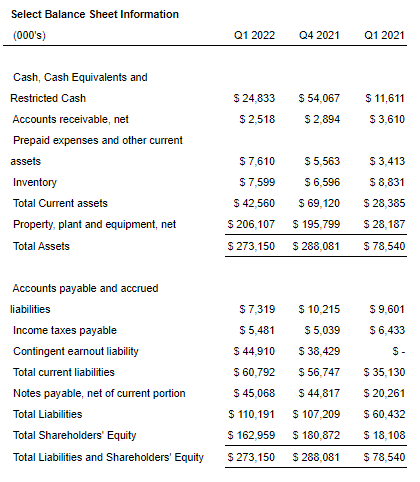

- Cash balance was $24.8 million at quarter-end, compared to $54.1 million at year-end 2021.

Management Commentary

“We reached a major milestone in the first quarter with the March 11th receipt of all necessary licenses to begin operations at our 5.5 million square foot SoCal facility. We immediately commenced cultivation activities, which included an initial transfer of approximately 30,000 clones from the Company’s nearby cultivation facility in Santa Barbara, California. Since then, we have expanded planting into the second section of the nursery and have moved several batches of plants into Greenhouse Six for the flowering and upcoming harvest. Early results have been good and we look forward to enjoying our first harvest from the SoCal facility before the end of June, roughly 9 months after the start of the retrofit,” said Kyle Kazan, Glass House Chairman and CEO. “Although wholesale pricing has improved slightly this year, it still remains extremely competitive. We are approaching one year since the steep decline in prices began, and the cumulative effect of low prices over the past 8-9 months is creating real distress for many operators. This is precisely why we set our sights on, and eventually purchased the SoCal facility.”

Being able to survive in difficult pricing environments is part of our strategy. Our goal is to not only survive but to thrive going forward. I expect that the most efficient growers will persevere, and that pricing will be flat and slowly rebound, but not to the levels we saw pre-commoditization.

Kyle Kazan, Glass House Chairman and CEO

Kyle Kazan, Glass House Chairman and CEO

For clarity, we are not experiencing a demand issue, as that remains strong. Our push now is to lean into our first phase expansion at SoCal to position the Company to achieve positive margins, even if this low pricing continues for a prolonged period.

“Subsequent to quarter-end, we announced three important developments that bolstered both our product portfolio and retail operations, including the completion of our PLUS acquisition, which established us as the only company with a top 5 position in both the Flower and Edibles segments in the California market based on BDSA and Headset data. We are incredibly excited to begin our work with the PLUS team to expand the presence of their premium products in our own retail stores and across our distribution network.”

“We also announced that the Company has entered into a binding Letter of Intent (“LOI”) to acquire the remaining equity and property ownership interests in The Pottery dispensary, located on L.A.’s Venice Boulevard. Over the past year, The Pottery has been cited by several publications, such as LA Weekly, Thrillist, the L.A. Times and Angeleno, as being one of the best high-end dispensaries in Southern California. We are excited to add The Pottery as our fourth wholly-owned dispensary in the State, and are looking forward to recognizing its incremental revenue in our financial results.”

“Finally, we announced definitive agreements with Natural Healing Center and its affiliates (collectively, “NHC”) to acquire a 100% equity interest in three retail assets: two operating retail dispensaries and one dispensary slated to open in Q3 2022. NHC is one of the pre-eminent dispensary chains in California, located in the Central Coast area. This acquisition will advance us further in our goal of becoming one of the largest retailers in the State; provide incremental outlets for our flower sales as the SoCal facility comes online; and add further support to our CPG business, including PLUS, our recently acquired and leading cannabis edibles company based in California. It also represents an immediate opportunity to drive significant expansion in our gross margin profile. Glass House-branded products currently represent approximately 5% of NHC’s revenue,3 versus an average of approximately 25% in Glass House owned or operated stores. We were attracted to these retail licenses because each of these permits is domiciled in a limited license jurisdiction of California. For example, Lemoore has two licenses in total, Morro Bay has two licenses in total, and Turlock has three licenses in total. We do not believe the city governments in these three NHC locations will issue more licenses any time soon.”

“We are now poised to execute a dramatic transformation in the size of our retail dispensary business this summer. Along with the ongoing ramp-up of Phase I production at our SoCal facility and the addition of PLUS, this further reinforces our trajectory to becoming cash flow positive by early 2023. Glass House had $21.7 million in retail revenues from its three wholly-owned dispensaries in 2021. With the addition of NHC’s three dispensaries to our portfolio, plus The Pottery and our new Farmacy dispensaries in Isla Vista, Santa Ynez and Eureka that are all slated to open in late Q3, we will have the potential to nearly triple our annual retail dispensary revenues to more than $60 million.4 The increased retail footprint will also provide a significant revenue opportunity for our CPG business including PLUS. Furthermore, we expect incremental Wholesale Biomass revenues from Phase I of the SoCal Facility to reach $50-75 million by early 2023. With our recent addition of PLUS’ $14 million in annual revenues on top of that, Glass House now has the potential to reach a revenue run rate in excess of $200 million within the next 12 months,1 versus the Company’s 2021 revenue of $69 million.”

First Quarter 2022 Operational Highlights

- Glass House Brands Receives Licenses to Operate SoCal Greenhouse Facility

Subsequent Events

- Glass House Brands Completes Acquisition of PLUS, a Leading California Edibles Brand

- Glass House Brands to Acquire Remaining Equity, Property Ownership in The Pottery Dispensary

- Glass House Brands to Acquire Three Natural Healing Center Dispensaries

Q1 2022 Financial Results Discussion

Total revenue for Q1 2022 was $14.0 million. These results represent a 24% decline versus Q4 2021 and an 8% decline versus Q1 2021.

Wholesale revenue of $5.1 million increased 14% vs. Q1 last year but declined 21% versus Q4 2021. The first quarter typically reports the lowest production and the highest costs, primarily because of decreased sunlight and sunlight intensity in the winter. A second key factor continues to be wholesale prices, which were healthy through the first half of 2021 but declined rapidly in Q3 2021 and have remained depressed. Despite a slight recovery in Q1 2022 from Q4 2021, wholesale prices remain well below the level they were in the comparative quarter of last year.

Q1 2022 dry weight equivalent sales increased 41% compared to the same quarter of last year, indicating continued strong demand for wholesale product. The increase in weight available for sale was driven by a 7% increase in production versus Q1 2021 and lower than anticipated sales and production in CPG. Average pricing was 19% lower than Q1 2021 but was supported by the production of a much higher percentage of flower this quarter compared to the same period last year.

Retail sales continued its steady performance with revenue of $4.9 million in the first quarter, falling 3% year-on-year and 5% sequentially.

Lastly, Q1 2022 CPG revenue decreased 31% compared to last year and 41% sequentially. The CPG business is mainly in the flower category and is being impacted by the declines in the overall California cannabis market. In addition, the Company did not manage inventory properly and did not achieve expected sell-through with retail customers, resulting in the need to increase discounting by 6 percentage points of gross sales over normal levels. Even with this drop in CPG revenue, Glass House Farms remained the No. 1 flower brand in Q1 2022 by BDSA Analytics and No. 2 by Headset.

Gross margin for the first quarter of 2022 was $2.3 million, or 17%, versus -2% in the fourth quarter of last year and 36% in Q1 2021.The primary difference between gross margin percentage in Q1 2021 compared to Q1 2022 is the decline in wholesale prices, which resulted in a $3.6 million decrease in revenue. Adjusting for this impact, Q1 2022 margin would have increased to 34%.

General and Administrative expenses were $9.4 million, compared to $13.5 million in Q4 2021. The $4.1 million decrease is primarily attributable to a $3.2 million reserve for non-operational bad debt established in Q4 2021 and a $0.8 million reduction in expenses in Q1 2022 compared to Q4 2021, which were related to the start-up of the SoCal facility and new dispensary openings.

Sales and marketing expenses were $0.9 million, a $0.3 million decrease from Q4 2021, primarily driven by a decrease in trade marketing and promotions.

Professional fees were $2.6 million, compared to $2.1 million in Q4 2021, with the increase primarily related to audit expenses incurred as part of the Company’s 2021 year-end audit.

Depreciation in Q1 2022 of $2.6 million was essentially flat compared to Q4 2021 as very little of the capex spending in the quarter was placed into service.

Adjusted EBITDA2 loss improved by $2.7 million to $6.4 million in the first quarter, compared to a loss of $9.1 million in Q4 2021. Almost the entire improvement was from Gross Margin, which increased to 17% from negative 2% in the fourth quarter of 2021.

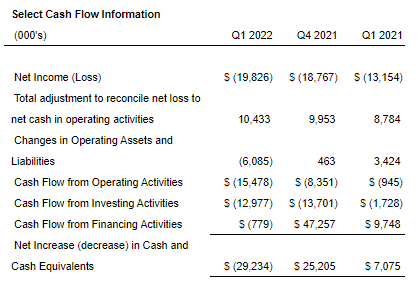

As of March 31, 2022, the Company had $24.8 million in cash including $3 million of restricted cash. This was down from $54.1 million in Q4 2021. Operating cash flow was negative $16 million, a decrease from negative $8 million in the fourth quarter of 2021. Increased use of working capital due mostly to inventory changes account for $6 million of the difference. Capex spending during Q1 2022 was $12 million with the majority spent at SoCal.

Financial results and analyses will be available on the Company’s investor relations website (https://ir.glasshousegroup.com/) and SEDAR (www.sedar.com).

Unaudited Q1 2022 Financial and Operational Metrics

Conference Call

The Company will host a conference call to discuss the results on Thursday, May 12, 2022 at 5:00 p.m. Eastern Time.

Webcast: Click here

Dial-In Number: 1-888-664-6392

Conference ID: 74529115

Replay: 1-888-390-0541

Replay Code: 529115 #

(replay available until 12:00 midnight Eastern Time Thursday, May 19, 2022)

Non-GAAP Financial Measures

Glass House defines EBITDA as Net Loss (GAAP) adjusted for interest and financing costs, income taxes, depreciation, and amortization. Adjusted EBITDA is defined as EBITDA excluding share-based compensation, stock appreciation rights expense, loss (income) on equity method investments, change in fair value of derivative liabilities, change in fair value of contingent liabilities, acquisition related professional fees, and non-operational start-up costs.

EBITDA and Adjusted EBITDA are presented because management has evaluated the financial results both including and excluding the adjusted items and believe that the supplemental non-GAAP financial measures presented provide additional perspective and insights when analyzing the core operating performance of the business. Such supplemental non-GAAP financial measures are not standardized financial measures under U.S. GAAP used to prepare the Company’s financial statements and might not be comparable to similar financial measures disclosed by other companies and, thus, should only be considered in conjunction with the GAAP financial measures presented herein.

The Company has provided a table above that provides a reconciliation of the Company’s net loss to Adjusted EBITDA for the three months ended March 31, 2022 compared to three months ended March 31, 2021 and three months ended December 31, 2021.

Footnotes and Sources:

- This statement means that at some point within the next twelve months, the Company has the potential to achieve monthly revenues that annualize to $200 million. The statement assumes the following in potential incremental revenues from each source: 1) Annualized Camarillo (SoCal facility) Phase I wholesale biomass sales of $50-75 million; 2) The three NHC dispensaries generate annualized revenues of $25 million; 3) The Pottery generates annualized revenues of $3.9 million; 4) PLUS maintains its pre-acquisition annualized revenues of $14 million per year; 5) The Isla Vista, Santa Ynez, and Eureka dispensaries are opened on schedule in Q3 2022 and that they produce an average of $5 million in annual revenues each; 5) That the Company’s core business that existed prior to the addition of these new revenue sources is able to deliver $69 million in revenue.

- Adjusted EBITDA is a non-GAAP financial measure. Please see “Non-GAAP Financial Measures” herein for further information and for a reconciliation of Adjusted EBITDA to the closest GAAP measure.

- Based on NHC’s unaudited management prepared financials.

- This statement assumes that: 1) the three NHC dispensaries generate annual revenues of $25 million; 2) the Pottery generates annual revenues of $3.9 million; 3) the Isla Vista, Santa Ynez, and Eureka dispensaries are opened on schedule in Q3 2022 and that they produce an average of $5 million in annual revenues each; 4) that the Company’s existing three dispensaries deliver at least $21.7 million in revenue, same as in 2021.

- Cost per Equivalent Dry Pound of Production (“CEDPP”), is the application of a subset of Costs of Goods Sold for cannabis biomass production (including all expenses from nursery and cultivation to curing and trimming – the point at which product is ready for sales as wholesale cannabis or to be transferred to CPG) applied to the Company’s metric of dry production which includes all dry production (flower, smalls and trim) plus equivalent dry weight for wet weight and fresh frozen that is not converted into dry goods by the Company.

- Includes all dry production (flower, smalls and trim) plus equivalent dry weight for wet weight and fresh frozen not converted into dry weight by the Company.

- Operational Canopy is cultivation (non-nursery) canopy actually utilized by the Company for cannabis production and is not equivalent to licensed canopy.

About Glass House

Glass House is one of the fastest-growing, vertically integrated cannabis companies in the U.S., with a dedicated focus on the California market and building leading, lasting brands to serve consumers across all segments. From its greenhouse cultivation operations to its manufacturing practices, from brand-building to retailing, the company’s efforts are rooted in the respect for people, the environment, and the community that co-founders Kyle Kazan, Chairman and CEO, and Graham Farrar, President, instilled at the outset. Through its portfolio of brands, which includes Glass House Farms, Forbidden Flowers, and Mama Sue Wellness, Glass House is committed to realizing its vision of excellence: outstanding cannabis products, produced sustainably, for the benefit of all. For more information and company updates, please visit www.glasshousebrands.com and https://ir.glasshousebrands.com/contact/email-alerts/.