iAnthus Announces Execution of Support Agreement for a Recapitalization Transaction

iAnthus Announces Execution of Support Agreement for a Recapitalization Transaction

NEW YORK and TORONTO, July 13, 2020 /PRNewswire/ – iAnthus Capital Holdings, Inc. (“iAnthus” or the “Company”) (CSE: IAN) (OTCQX: ITHUF), which owns, operates, and partners with regulated cannabis operations across the United States, announced today that it has entered into a Restructuring Support Agreement (as defined below) with 100% of its Secured Lenders (as defined below) and over 91% of the Unsecured Debentureholders (as defined below) to effect a proposed recapitalization transaction (the “Recapitalization Transaction”), as well as provide Interim Financing (as defined below) of $14 million.

The Recapitalization Transaction is expected to significantly reduce the Company’s outstanding indebtedness and annual interest costs, improve its capital structure and liquidity, and result in an enhanced financial foundation for the Company. Assuming completion of the Recapitalization Transaction, the Company’s pro forma outstanding indebtedness will be reduced from $168.7 million (excluding fees and accrued and unpaid interest thereon) as at June 30, 2020 to $101.4 million (excluding $20 million of Preferred Equity (as defined in the schedule to this news release and more fully described below)).

Pursuant to the terms of the Restructuring Support Agreement, the Recapitalization Transaction will be implemented pursuant to arrangement proceedings commenced under the British Columbia Business Corporations Act (“BCBCA”) or, only if necessary, the Companies’ Creditors Arrangement Act (“CCAA”). The Recapitalization Transaction, if consummated, is expected to have the following key elements:

- The Secured Debentures (as defined below), after the completion of the Recapitalization Transaction, will be amended to (i) reduce the principal balance from $97.5 million, plus accrued and unpaid interest and fees, to $85 million, (ii) reduce the interest rate by 5% per annum; (iii) eliminate cash pay interest; (iv) extend the original maturity date by over four years and (v) remove the conversion feature;

- The $60 million principal amount of Unsecured Debentures (as defined below), plus accrued and unpaid interest and fees, will be exchanged and no longer be outstanding;

- The Company will issue an aggregate of $20 million of Preferred Equity to the Secured Lenders ($5 million) and Unsecured Debentureholders ($15 million) with a maturity date of five years and no cash pay dividends (or other form of consideration on substantially similar economic terms);

- The Secured Lenders, on the one hand, and the Unsecured Debentureholders, on the other hand, will each be issued an equal amount of common shares of the Company (“Common Shares”) such that each will own 48.625% of the Common Shares upon completion of the Recapitalization Transaction (50% each if completed through CCAA Proceedings (as defined below)), allocated pro rata among the holders thereof in accordance with the principal amount of the applicable debt held by each such holder prior to the closing time;

- Only if the Recapitalization Transaction is consummated through the Arrangement Proceedings (as defined below), the existing holders at the time of completion (the “Existing Shareholders”) of Common Shares will retain 2.75% of the ownership of the Common Shares (the “Common Shareholder Interest”). If the Recapitalization Transaction is completed through CCAA Proceedings, the Existing Shareholders will not receive a recovery and the Common Shareholder Interest will instead be allocated equally as among the Secured Lenders and Unsecured Debentureholders;

- All existing options and warrants of the Company will be cancelled upon completion of the Recapitalization Transaction, and the Company anticipates allocating an amount of equity to be made available for management, employee, and director incentives; and

- Obligations to employees, customers and suppliers will not be affected by the Recapitalization Transaction and are expected to continue to be satisfied in the ordinary course.

Subject to compliance with the Restructuring Support Agreement, the Secured Lenders and Initial Consenting Unsecured Debentureholders (as defined below) will forbear from further exercising any rights or remedies in connection with any events of default of the Company now or hereafter occurring under their respective agreements and will stop any current or pending enforcement actions respecting same.

A more detailed summary of the key terms of the Recapitalization Transaction is attached as a schedule to this news release and the full text of the Restructuring Support Agreement will be made available on SEDAR.

All references to currency in this news release are in U.S. dollars.

In connection with the Recapitalization Transaction, the Company and certain of its subsidiaries (collectively, the “Subsidiaries”) have entered into a restructuring support agreement (the “Restructuring Support Agreement”) with all of the holders (the “Secured Lenders”) of the 13% senior secured convertible debentures (the “Secured Debentures”) issued by iAnthus Capital Management, LLC (“iAnthus SubCo”), the Company’s U.S. wholly-owned subsidiary, and certain holders (the “Unsecured Debentureholders”) of the 8% convertible unsecured debentures (the “Unsecured Debentures”) issued by the Company and which hold in the aggregate over 91% of the principal amount of Unsecured Debentures (the “Initial Consenting Unsecured Debentureholders”). Pursuant to the Restructuring Support Agreement, the Secured Lenders and the Initial Consenting Unsecured Debentureholders have, among other things, agreed to support the Recapitalization Transaction and vote in favour of (i) the plan of arrangement (the “Plan of Arrangement”) to be filed by the Company in connection with proceedings (the “Arrangement Proceedings”) to be commenced under the BCBCA, or (ii) subject to the terms of the Restructuring Support Agreement, proceedings (the “CCAA Proceedings”) commenced by the Company for approval of a plan of compromise and arrangement under the CCAA.

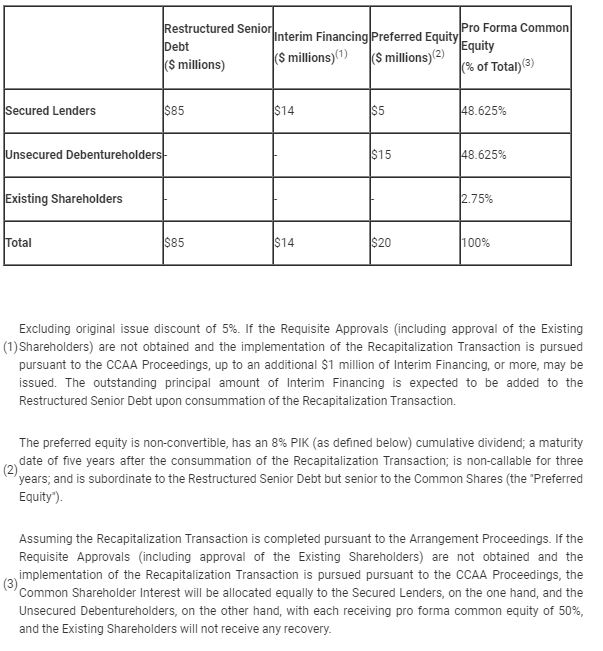

In connection with the Recapitalization Transaction, certain of the Secured Lenders have agreed to provide interim cash financing of $14 million (the “Interim Financing”) to iAnthus SubCo on substantially the same terms as the Restructured Senior Debt (as defined in the schedule to this news release), with a 5% original issue discount (i.e., the principal is to be grossed up to approximately $14.7 million), which is expected to be funded to iAnthus SubCo within three business days of execution of the Restructuring Support Agreement. If the Recapitalization Transaction is pursued pursuant to the CCAA Proceedings, up to an additional $1 million of Interim Financing, or more, may be obtained from the Secured Lenders.

If the Recapitalization Transaction is implemented pursuant to the Arrangement Proceedings, upon closing of the Recapitalization Transaction, the Secured Lenders and the Unsecured Debentureholders are expected to hold an aggregate of 97.25% of the Common Shares then outstanding and the Existing Shareholders will collectively own 2.75% of the then outstanding Common Shares. However, if the Recapitalization Transaction is implemented pursuant to the CCAA Proceedings, upon consummation of the Recapitalization Transaction, the Secured Lenders and the Unsecured Debentureholders are expected to hold all of the Common Shares then outstanding and the Existing Shareholders would not receive any recovery.

As initially disclosed in the Company’s news release dated April 6, 2020, iAnthus’ special committee of the board of directors (the “Special Committee”) initiated a Strategic Alternatives Review Process and hired Canaccord Genuity Corp. as its financial advisor. The Special Committee, supported by its legal and financial advisors, worked expeditiously to complete the review of a range of strategic alternatives. After an extensive review and consultation process with its legal and financial advisors, the Company’s board of directors (the “Board”) concluded that the Recapitalization Transaction represents the best available alternative to improve the Company’s capital structure and to maximize and preserve value for the Company and its stakeholders.

“After an extensive review process, consultation with our financial and legal advisors and careful consideration of our available options, the Special Committee has recommended, and the Board has unanimously approved, the proposed Recapitalization Transaction,” said Robert Whelan, Chair of the Special Committee. “We believe that the Recapitalization Transaction allows iAnthus to move forward with a stronger capital structure.”

The decline in the overall public equity cannabis markets that began in Q2 2019, coupled with the extraordinary market conditions that began in Q1 2020 due to COVID-19, have negatively impacted the financing markets and have caused significant liquidity constraints for the Company.

Randy Maslow, President and Interim CEO

Randy Maslow, President and Interim CEO

The shared objectives of the Company and its creditors are to significantly reduce the outstanding indebtedness and annual interest costs, improve the Company’s capital structure and liquidity, and provide a stable financial foundation for the Company to capitalize on its national licensure footprint and build-out our expanding business.

Completion of the Recapitalization Transaction through the Arrangement Proceedings will be subject to, among other things, requisite stakeholder approval of the Plan of Arrangement at meetings expected to be held in September 2020, such other approvals as may be required by the Supreme Court of British Columbia (the “Court”), approval of the Plan of Arrangement by the Court and the receipt of all necessary regulatory and stock exchange approvals (collectively, the “Requisite Approvals”). If the Requisite Approvals are obtained, the Plan of Arrangement will bind all Secured Lenders, Unsecured Debentureholders and Existing Shareholders.

Certain of the Secured Lenders (funds affiliated with Gotham Green Partners, LLC (“Gotham”)) may be considered “related parties” as such term is defined in Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions (“MI 61-101”). Accordingly, the Interim Financing with the Secured Lenders and the Recapitalization Transaction may be “related party transactions” as defined in MI 61-101. The Company will rely on the exemption from the formal valuation requirement at section 5.5(b) of MI 61-101 (Issuer Not Listed on Specified Markets) in respect of the Interim Financing and the Recapitalization Transaction, and the exemption from minority approval requirement at Section 5.7(e) of MI 61-101 (Financial Hardship) in respect of the Interim Financing. The Company’s decision to rely on the financial hardship exemption was made upon the recommendation of the Special Committee, all of whose members are independent directors free from interest in the Interim Financing and unrelated to the parties involved in such transaction. The Company did not file a material change report 21 days prior to the expected closing of the Interim Financing as the structure of the transaction and details of the participation of the Secured Lenders had not been confirmed at that time. Due to the Company’s liquidity constraints, the Board believes it is reasonable and necessary in the circumstances to complete the Interim Financing and the Recapitalization Transaction within the available financing windows.

This news release provides only summary information with respect to the Restructuring Support Agreement and the proposed Recapitalization Transaction. Readers are urged to consult the full text of the Restructuring Support Agreement, a copy of which will be filed by the Company on SEDAR (www.sedar.com). Further information about the Recapitalization Transaction will also be made available on SEDAR and the Company’s website (www.ianthus.com). Additional information and key dates in connection with the implementation of the Recapitalization Transaction, including with respect to the Arrangement Proceedings, will be made publicly available by the Company.

Advisors

iAnthus’ legal advisors in connection with the Recapitalization Transaction are McMillan LLP and Duane Morris LLP, and its financial advisor is Canaccord Genuity Corp.

The legal advisors for Gotham in connection with the Recapitalization Transaction are Davies Ward Phillips & Vineberg LLP, SkyLaw Professional Corporation and Honigman LLP. The Initial Consenting Unsecured Debentureholders’ legal advisor in connection with the Recapitalization Transaction is Cassels Brock & Blackwell LLP and legal advisor for Oasis Investments II Master Fund Ltd., one of the Unsecured Debentureholders, is Stikeman Elliott LLP.

Financial Statements Update

Further to the Company’s news release dated June 17, 2020, iAnthus did not file the following continuous disclosure documents (collectively, the “Required Filings”) prior to the filing deadline on June 15, 2020:

- audited annual financial statements for the year ended December 31, 2019;

- management’s discussion and analysis relating to the audited financial statements for the year ended December 31, 2019; and

- certification of the foregoing filings as required by National Instrument 52-109 Certification of Disclosure in Issuers’ Annual and Interim Filings.

As a result, further to the Company’s news release dated June 23, 2020, the Company is subject to a cease trade order (the “CTO”) issued by the Ontario Securities Commission on June 22, 2020. The CTO affects trading in all securities of the Company by securityholders of the Company, in each jurisdiction in Canada in which the Company is a reporting issuer and will remain in effect until such time as the Company has made the Required Filings. If the Required Filings are made within 90 days of the date of the CTO, such filings would constitute the Company’s application to have the CTO revoked. The Company expects to file the Required Filings on or before the 90-day deadline.

The issuance of any securities of iAnthus remains subject to the terms of the CTO.

About iAnthus

iAnthus owns and operates licensed cannabis cultivation, processing and dispensary facilities throughout the United States, providing investors diversified exposure to the U.S. regulated cannabis industry. Founded by entrepreneurs with decades of experience in operations, investment banking, corporate finance, law and healthcare services, iAnthus provides a unique combination of capital and hands-on operating and management expertise. iAnthus currently has a presence in 11 states and operates 35 dispensaries (AZ-4, MA-1, MD-3, FL-16, NY-3, CO-1, VT-1 and NM-6 where iAnthus has minority ownership). For more information, visit www.iAnthus.com.

COVID-19 Risk Factor

The Company may be impacted by business interruptions resulting from pandemics and public health emergencies, including those related to COVID-19. An outbreak of infectious disease, a pandemic, or a similar public health threat, such as the recent outbreak of COVID-19, or a fear of any of the foregoing could adversely impact the Company by causing operating, manufacturing, supply chain, and project development delays and disruptions, labor shortages, travel, and shipping disruption and shutdowns (including as a result of government regulation and prevention measures). It is unknown whether and how the Company may be affected if such a pandemic persists for an extended period of time, including as a result of the waiver of regulatory requirements or the implementation of emergency regulations to which the Company is subject. Although the Company has been deemed essential and/or has been permitted to continue operating its facilities in the states in which it cultivates, processes, manufactures, and sells cannabis during the pendency of the COVID-19 pandemic, there is no assurance that the Company’s operations will continue to be deemed essential and/or will continue to be permitted to operate. The Company may incur expenses or delays relating to such events outside of its control, which could have a material adverse impact on its business, operating results, financial condition, and the trading price of the Company’s common shares.

SCHEDULE

KEY TERMS OF RECAPITALIZATION TRANSACTION

All references to currency are in US dollars.

Summary Table of Treatment of Affected Parties

Pursuant to the Recapitalization Transaction and as described above, the Secured Lenders, the Unsecured Debentureholders and the Existing Shareholders of iAnthus are to be allocated and issued, approximately, the amounts of Restructured Senior Debt (as defined below), Interim Financing, Preferred Equity (as defined below) and percentage of the pro forma common equity, as presented in the following table:

Revised Capital Structure

The capital structure of iAnthus will be revised in accordance with the following terms:

- The outstanding Secured Debentures will be amended to reflect the following:

- The principal balance will be reduced to $85 million (the “Restructured Senior Debt”), which will be increased by the amount of the Interim Financing;

- First lien, senior secured position over all assets of the Company and the Subsidiaries; and

- Non-convertible; payment in kind (“PIK”) interest at an 8% annual interest rate; maturity date of five years after the consummation of the Recapitalization Transaction; and non-callable for three years.

- The Unsecured Debentures will be exchanged for the Equity Consideration (as defined below) and Preferred Equity granted to the Unsecured Debentureholders.

- The Secured Lenders will be issued their pro rata share of $5 million of Preferred Equity.

- The Unsecured Debentureholders will be issued their pro rata share of $15 million of Preferred Equity.

- The Secured Lenders, on one hand, and the Unsecured Debentureholders, on the other hand, shall each be issued an equal amount of Common Shares from treasury (“Equity Consideration”) that, when added together with the Common Shareholder Interest (as defined below), equals 100% of the total issued and outstanding common shares of the Company at the effective time of the arrangement (prior to any anticipated dilution from any MIP (as defined below)).

- The Existing Shareholders will retain 2.75% ownership of the common equity.

- A to-be-determined amount of equity will be made available for management, employee, and director incentives, as determined by the New Board (as defined below) following consummation of the Recapitalization Transaction (the “MIP”).

- All existing warrants and options of the Company will be cancelled upon consummation of the Recapitalization Transaction.

- The Common Shares may be consolidated pursuant to a yet-to-be decided consolidation ratio.

The form of the Preferred Equity provided to the Secured Lenders and Unsecured Debentureholders and described herein is subject to tax planning and may instead be subordinated unsecured debt of the Company or other form of consideration that is agreed to by the Secured Lenders, each of the Initial Consenting Unsecured Debentureholders and the Company, on substantially similar economic terms.

Transaction Implementation

The Recapitalization Transaction will be pursued pursuant to the Arrangement Proceedings, unless CCAA Proceedings are commenced in accordance with the terms of the Restructuring Support Agreement. If the Recapitalization Transaction is completed through CCAA Proceedings, the Existing Shareholders will not receive a recovery and the Common Shareholder Interest will instead be allocated equally as among the Secured Lenders and Unsecured Debentureholders.

Interim Financing

The Secured Lenders will provide $14 million of Interim Financing to iAnthus SubCo, on substantially the same terms as the Restructured Senior Debt, with a 5% original issue discount (principal to be grossed up). The Interim Financing will be funded to iAnthus SubCo within three business days of execution of the Restructuring Support Agreement. In the event of the CCAA Proceedings, the Interim Financing amount will be increased by up to $1 million, or more. The amounts of the Interim Financing advanced to the Company will be converted into and the principal balance will be added to the Restructured Senior Debt upon consummation of the Recapitalization Transaction.

Governance and Management

iAnthus will (i) use commercially reasonable efforts to optimize operations of its business, including controlling and monitoring costs (the “Optimization Efforts”), (ii) engage an advisor to assist the Company in connection with the Optimization Efforts, and (iii) permit the Initial Consenting Unsecured Debentureholders to appoint one person as an observer to participate in meetings of the board of directors.

Upon implementation of the Recapitalization Transaction, the board of directors (the “New Board”) will be constituted as follows: (i) three nominees by the Secured Lenders; (ii) three nominees by the Initial Consenting Unsecured Debentureholders; and (iii) a new CEO as the seventh member of the New Board, to be agreed upon by the Secured Lenders’ and Initial Consenting Unsecured Debentureholders’ nominees.

Standstill and Dismissal of Litigation Claims Involving iAnthus and Oasis

iAnthus has agreed to discontinue with prejudice its litigation claim which it made on February 27, 2020 against Oasis (regardless of whether the Recapitalization Transaction is consummated), and Oasis has agreed, while the Restructuring Support Agreement is in effect, not to take any steps in connection with its counterclaim against iAnthus. In addition, iAnthus and Oasis have agreed that the counterclaim by Oasis against iAnthus will be dismissed as a condition of closing of the Recapitalization Transaction. For further details on these litigation claims, see iAnthus’ news releases dated February 27, 2020 and March 16, 2020.

Waiver of Events of Default and Withdrawal of Enforcement Steps

Subject to the terms of the Restructuring Support Agreement, the Secured Lenders and the Consenting Unsecured Debentureholders agree to forbear from further exercising any rights or remedies in connection with any events of default that now exist or may in the future arise under any of the purchase agreements in respect of the Secured Debentures and all other agreements delivered in connection therewith, the purchase agreements in respect of the Unsecured Debentures and all other agreements delivered in connection therewith, and any other agreement to which the Collateral Agent (as defined under the Secured Debenture), Secured Lenders or Initial Consenting Unsecured Debentureholders are party with the Company (the “Defaults”), and shall take such steps as are necessary to stop any current or pending enforcement efforts in relation thereto. Upon consummation of the Recapitalization Transaction and subject to the terms of the Restructuring Support Agreement, the Collateral Agent, Secured Lenders and Consenting Unsecured Debentureholders are expected to irrevocably waive all Defaults and take all steps required to withdraw, revoke and/or terminate any enforcement efforts in relation thereto.

Furthermore, the Restructuring Support Agreement contemplates that usual and customary releases in connection with the implementation of the Recapitalization Transaction will be obtained by the parties to the Restructuring Support Agreement, among others, in connection with the Common Shares, the Secured Debentures, the Unsecured Debentures and the Recapitalization Transaction.