![]()

CORPORATE PARTICIPANTS

Najim Mostamand, Director of Investor Relations

Nick Kovacevich, Co-founder, Chairman, Chief Executive Officer

Chris Tedford, departing Chief Financial Officer

Stephen Christoffersen, incoming Chief Financial Officer

Jason Vegotsky, President, Chief Revenue Officer

CONFERENCE CALL PARTICIPANTS

Vivien Azer, Cowen

Aaron Grey, Alliance Global Partners

Bobby Burleson, Canaccord

Scott Fortune, Roth Capital Partners

Greg Gibas, Northland Securities

Gordon Johnson, GLJ Research

PRESENTATION

Operator

Greetings, and welcome to the KushCo Holdings Fiscal Second Quarter 2020 Earnings Conference Call.

At this time all participants are in a listen only mode. A question-and-answer session will follow the formal presentation. If anyone should require Operator assistance, please press star, zero on your telephone keypad. Please note, this conference is being recorded.

I will now turn the conference over to your host, Mr. Najim Mostamand, KushCo’s Director of Investor Relations. Mr. Mostamand, please go ahead.

Najim Mostamand

Good afternoon, and welcome to the KushCo Holdings Fiscal Second Quarter 2020 Earnings Conference Call. A replay of this call will be archived on the Investor Relations section of the KushCo Holdings website, ir.kushco.com.

Before we begin, please let me remind you that, during the course of this conference call, Management may make forward looking statements. These forward looking statements are based on current expectations that are subject to a number of risks and uncertainties that may cause actual results to differ materially from expectations. These risks are outlined in the Risk Factors section of our SEC filings. Any forward looking statements should be considered in light of these factors. Please also note as a Safe Harbor, any outlook we present is as of today and Management does not undertake any obligation to revise any forward looking statements in the future.

With me on the call today are our Co founder, Chairman & CEO Nick Kovacevich, our departing CFO Chris Tedford, our incoming CFO Stephen Christoffersen, and our President and CRO Jason Vegotsky.

With that, I would now like to hand the call over to Nick.

Nick?

Nick Kovacevich

Thanks Najim, and thank you all for attending our Fiscal Second Quarter 2020 earnings call.

I know these are difficult and unfamiliar times for everyone, so I appreciate you all continuing to make the time, wherever you are, to learn more about, not only our recent results, but more excitingly, where we’re headed next, which we believe is ultimately on the right track to achieve positive Adjusted EBITDA.

We have a lot to cover today, so I’ll jump right into the agenda. First, I’ll provide some introductory remarks and go over some of our Fiscal Q2 2020 highlights, some of which we’ve already shared last month when we pre announced our revenue for the quarter. Then I’ll hand it over to Chris, who will share some final remarks as he passes the baton to Stephen; after that, Stephen will take us through the financial summary for Q2; and we’ll finish it off with a deep dive of our new strategic plan of getting to positive Adjusted EBITDA, before we open it up for Q&A.

So with that said, let’s turn to Slide 5 of the supplemental earnings slides, which if you haven’t downloaded them already, you can do so by visiting the Financial Results page of our IR website at ir.kushco.com.

Despite a challenging market backdrop, we are pleased with how we executed according to our plan.

Despite a challenging market backdrop, we are pleased with how we executed according to our plan.

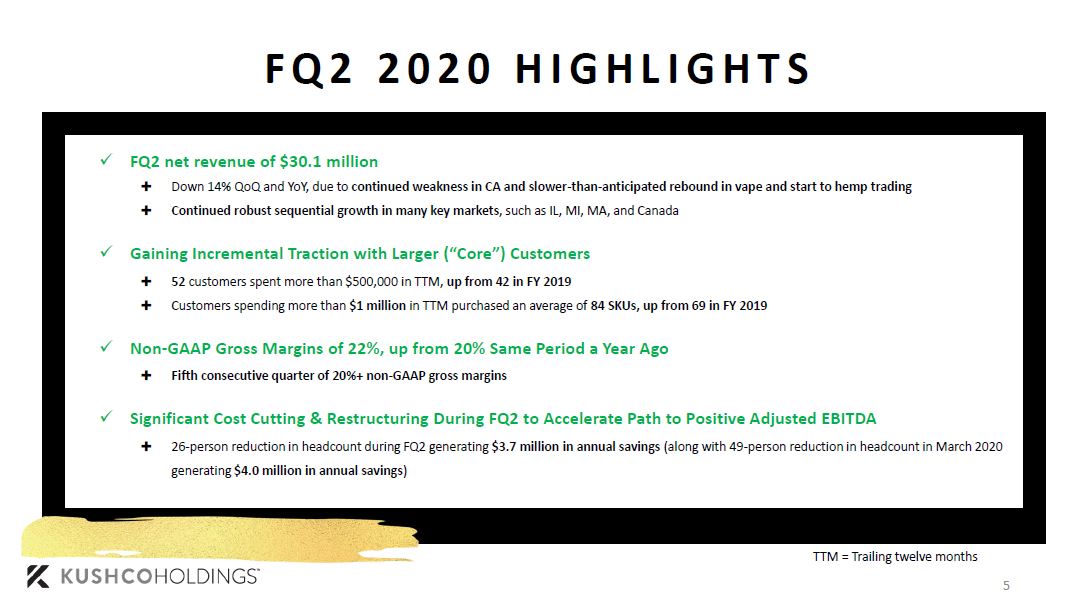

First and foremost, we generated revenue of $30.1 million during fiscal Q2, which was right in line with our preannouncement. Revenue was down 14% year over year and Q over Q, due to a number of factors, the main ones being a slower than anticipated rebound in vape, following the illicit market vape crisis; a slower start to our hemp trading business; and continued weakness in the California market, which is only being exacerbated by the recent COVID 19 pandemic. Frankly, it’s the last driver that accelerated our decision to roll out this new strategic plan to get to positive Adjusted EBITDA as quickly as we can, which we’ll go into later on this call.

Despite the overall market decrease in revenue, there were several positive takeaways from this quarter, including some trends that we’re encouraged to see forming. For one, we saw continued robust sequential growth in many of our key markets, such as Illinois, Michigan, Massachusetts, and Canada, which all nearly doubled or tripled in sales quarter over quarter. We also continued to gain traction with our larger core customers, adding new customers and cross selling deeper into this base. During the trailing twelve months ended fiscal Q2, we had 52 customers who spent more than $500,000 with us, versus just 42 a couple of quarters ago. What’s more is that these larger customers continue to purchase more SKUs from us, as the average SKU count purchased per customer continues to climb, reaching 84 SKUs in Q2 versus 69 a couple of quarters ago.

Next I want to talk about our gross margins. Because of some of the restructuring costs this quarter, our gross margins for fiscal Q2 were actually negative, which Stephen will go into more detail on his remarks. On a non GAAP basis, however, which excludes these restructuring costs, we achieved 22% gross margins, up from 20% in the same year ago quarter. It’s worth noting that this is the fifth quarter in a row where we achieved non GAAP gross margins above the 20% mark.

Next I want to talk about the cost cutting and restructuring that we’re doing to accelerate our path toward positive Adjusted EBITDA.

Perhaps most importantly, Q2 was best defined by the significant progress we made in right sizing our business as part of our newly unveiled strategic plan to accelerate our path to positive Adjusted EBITDA. We began the execution of this plan during fiscal Q2, and since then we have been hard at work executing a comprehensive restructuring process that rationalizes all aspects of our operations, including significantly reducing our overhead, implementing tighter expense controls, consolidating our warehouses, reducing our inventory, and drastically altering our sales strategy to focus more on growing predictable, creditworthy, and financially stronger customers.

During fiscal Q2, we completed a 26 person reduction in headcount, which generated approximately $3.7 million in annual savings. Just shortly after the quarter had ended, we completed another reduction in force, this time for 49 employees, which generated $4 million in annual savings. Altogether, we have right sized our workforce by nearly 50% since the start of the fiscal year in September, which altogether generates approximately $12 million in cost savings: a huge lever that we pulled to help us move closer to our goal of positive Adjusted EBITDA.

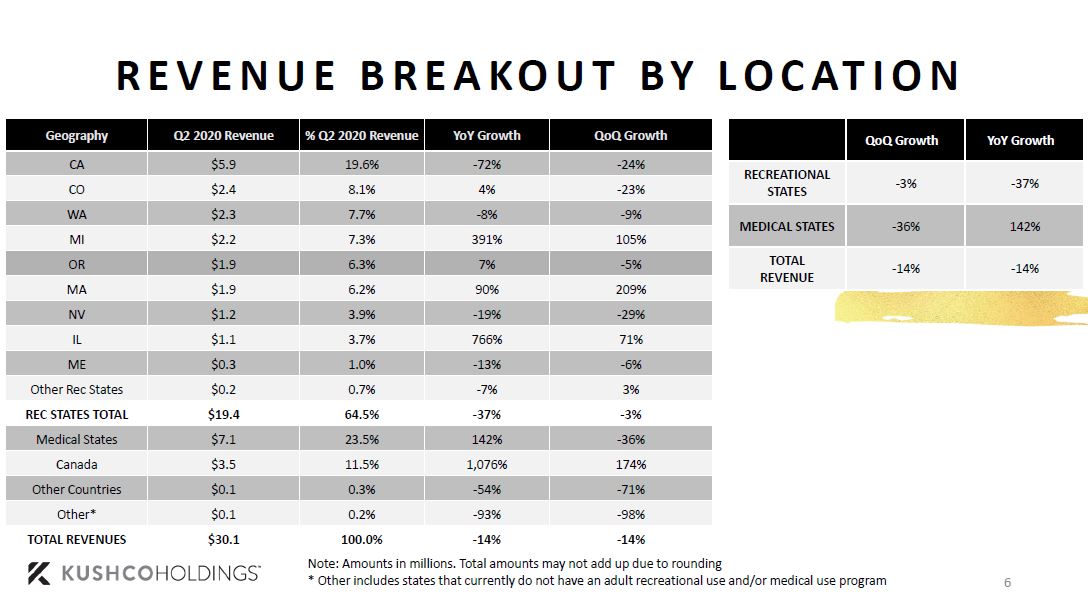

Next I’d like to turn your attention to Slide 6, where we look at our geographic sales breakout. As we mentioned in our pre announcement last month, California continues to struggle, while most of the more established markets, such as Colorado, Washington, Oregon and Nevada, have taken a little bit more time to recover from some of the headwinds exiting Calendar ’19, including the illicit market vape crisis, especially for Washington which still had its flavor ban in place throughout most of our fiscal Q2.

Next I’d like to turn your attention to Slide 6, where we look at our geographic sales breakout. As we mentioned in our pre announcement last month, California continues to struggle, while most of the more established markets, such as Colorado, Washington, Oregon and Nevada, have taken a little bit more time to recover from some of the headwinds exiting Calendar ’19, including the illicit market vape crisis, especially for Washington which still had its flavor ban in place throughout most of our fiscal Q2.

We expect California, which was down 24% sequentially in Q2, to continue struggling in the near future, as the issues of a robust illicit market and a complicated and onerous tax structure do not appear to be resolving soon, even with some encouraging developments, such as the rise of delivery in municipalities that currently do not allow a retail storefront, which, to remind you, is still over 70% of the municipalities.

Frankly, it’s because of this current dynamic that we have accelerated our focus out of California, where the majority of MSOs have purposefully stayed away from, and we continue to go deeper with these MSOs that have been expanding in other states, especially seeing success in the limited license states, like Florida, Illinois, or Massachusetts, where these operators have more of a competitive moat.

This strategic shift should ensure that we continue to ride the growth wave as we go deeper and wider with these customers in these markets. Not only will this shift our focus away from our home state, it will reduce our impact of a slower growth on the business. And it will also align perfectly with the strategy of going deeper with core customers, who are often much more creditworthy and are able to pay their invoices, something that we unfortunately have not seen a lot of in California recently.

In these more emerging markets, MSOs are seeing a lot of progress, and we believe we can directly benefit from their growth. For example Michigan, which went adult rec legal at the start of fiscal Q2, we saw our sales more than double, quarter over quarter. Massachusetts also had a very strong quarter, especially when the state removed its temporary vape ban at the start of our fiscal Q2, which helped us more than triple our sales in that market, quarter over quarter. Moving down the list, Illinois also had another strong quarter, nearly doubling sequentially, as we all saw the tremendous opening that market had in just its first few months of being adult rec legal.

One area that we did not see the quarter over quarter growth that we were expecting is in our medicinal markets, where revenues were actually down 36% sequentially. This was actually driven more by timing rather than anything else, as we had secured some very large vape orders from a few leading MSOs; however, because of the Chinese New Year holiday being extended due to the spread of COVID 19, and the related production and shipment delays that this extension caused, we were not able to get these products in and shipped out during fiscal Q2. The good news is that these products are actually now en route from China, and we expect those orders to appear in our fiscal Q3 results.

At a more high level perspective, we are continuing to see meaningful progress in many medical states, particularly in Arizona, Florida, Maryland, Pennsylvania, Ohio, and Oklahoma, which all experienced healthy year over year growth during fiscal Q2. Looking ahead, we expect revenue from these states to continue to trend higher, especially if some of them, like potentially Arizona and Pennsylvania, are able to legalize adult use this election cycle.

The last market I wanted to touch on, which performed exceptionally well during Q2, was Canada, which nearly tripled in sales sequentially to $3.5 million, representing the third quarter in a row that we were able to generate over $1 million in that market. We have talked on previous calls about the slow, laboring start that the country has had, not only in terms of our business but in the general market as well. There’s been an overabundance of supply, a lack of new stores coming online and a delayed Rec 2.0 rollout that has made this market very challenging for many, including us; but we’re fortunate to have seen that some of our early investments to establish deeper relationships with leading LPs is now finally starting to pay off.

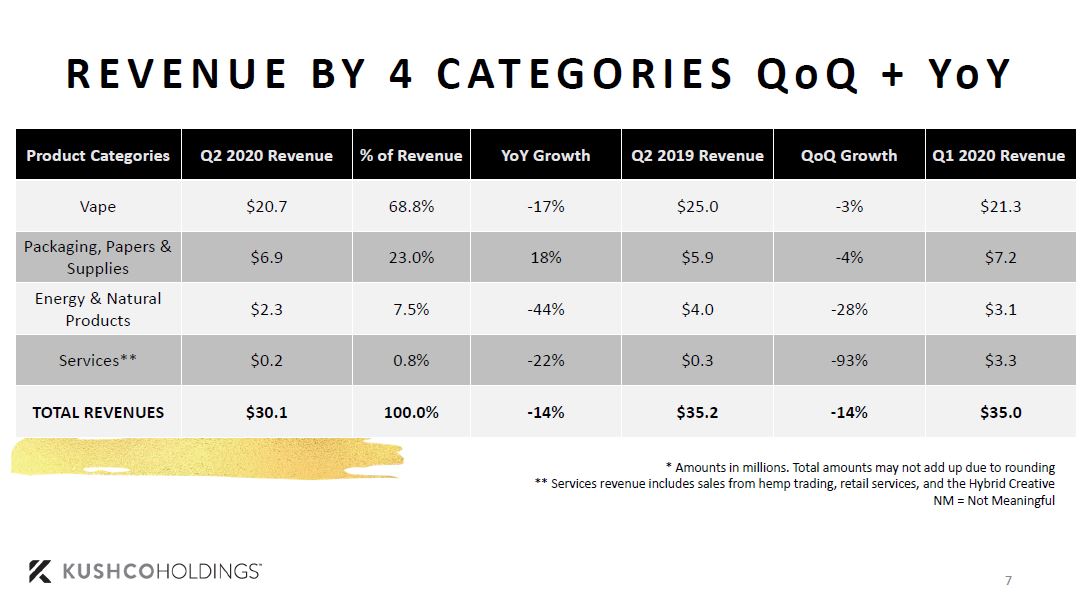

Next I’d like to dive into Slide 7, which is our product mix.

First we’ll start with vape. Vape was fairly flat in fiscal Q2, largely driven by the slower than anticipated rebound I mentioned earlier. This slower rebound is consistent with some of the broader market data we’re seeing, which shows that, while vape is rebounding in terms of market share, it’s not necessarily back to pre vape crisis levels yet. Obviously, with a few vape bans having still been in place during our fiscal Q2, both here in the States but also in Canada, our flat Q2 vape number was somewhat to be expected.

First we’ll start with vape. Vape was fairly flat in fiscal Q2, largely driven by the slower than anticipated rebound I mentioned earlier. This slower rebound is consistent with some of the broader market data we’re seeing, which shows that, while vape is rebounding in terms of market share, it’s not necessarily back to pre vape crisis levels yet. Obviously, with a few vape bans having still been in place during our fiscal Q2, both here in the States but also in Canada, our flat Q2 vape number was somewhat to be expected.

As we’ve talked about already before, the illicit market vape crisis and the cash crunch it brought really put a lot of our customers in California either out of business or quite nearly so, leaving us not only with a reduced customer base and revenue level for vape, but also a decent amount of receivables that then became more challenging to collect as the whole situation unfolded.

Stephen will be going over some of the financial commentary regarding the write downs we took in Q2, but essentially given the dynamics in California, we decided to take a more conservative and prudent approach to writing down receivables that at this point we don’t perceive to have a high probability of being collectible.

The dynamics around our vape sales are a big part in what’s driving our strategic shift. We traditionally sold a lot of vape products to a lot of customers. However, many of those customers are becoming too financially risky to extend credit to. Therefore, we’ve been more focused on growing vape sales with our core customers, which are leading MSOs and LPs. We are very pleased to see continued growth in our vape business with this group, and expect going forward our vape business to be more stable and consistent as it will be anchored by this premier group of customers.

Next, I want to take a look at our Packaging, Papers & Supplies bucket.

Packaging, like vape, held up well during fiscal Q2 compared to the prior quarter. With our new strategy, we expect our packaging business to continue to grow, while being anchored by a more premier group of customers, utilizing higher margin custom packaging that’s stickier in nature, and focusing less on carrying a wide variety of stock SKUs, which will also drastically increase our inventory turns.

This shift in inventory strategy, from one that previously required a ton of inventory and warehouse space to now requiring a smaller level of inventory and a more consolidated warehouse footprint, will free up a considerable amount of cash that we can reapportion toward these growth initiatives that our core customers are demanding.

With our previously mentioned strategic shift toward the MSOs, LPs, and leading brands, we do expect some turnover on the smaller end of the customer spectrum, as we emphasize more transactions with them that are cash based for stock items, and are completed through our customer service support line rather than a dedicated sales rep. However, we do expect to retain a good chunk of this business; it’s just going to be done in a manner that’s much more efficient and profitable for the Company.

Overall, we were pleased with our packaging results from this quarter, and we are excited about the future of this category, given our new strategic direction.

Next I’d like to dive into our Services bucket, which was down significantly compared to the previous quarter. This was obviously a big area of disappointment for us, as we were hoping for continued momentum in this promising bucket. However, a few developments have occurred in the past months that made it more challenging to grow this category.

For one, the prices of hemp biomass have come down dramatically since we launched the hemp trading division, as the market remains saturated with supply. Though this has been improving as of late, prices are still very low, incentivizing many farmers to either stay put, liquidate their crop, or simply not re plant after they’re done harvesting the current crop.

Secondly, we have been seeing major processors going out of business or declaring bankruptcy. Many of them had a Field of Dreams mentality of build it and they will come, but sadly that just hasn’t happened and these processors have spent a ton of money without the revenue coming in to support their high cost structures.

Lastly, we continue to see the FDA stall with respect to their decision on how they want to regulate CBD in ingestibles. To date, there simply hasn’t been any guidance that major retailers can rely on, which has constricted the biggest bottleneck of the CBD industry: retail. While we’re seeing modest success with our Retail Services division with tinctures and topicals, as well as some ingestibles in several non FDM channels, the big unlock will obviously be when the FDA comes out with clear and comprehensive guidance that gives the industry the much needed boost to grow at a sustainable level.

But even though the revenues from this category are currently not where we like them to be at, or where we ultimately expect them to be, there were some positive takeaways and developments from this quarter that we’re encouraged to see materializing.

As we mentioned in our press release last month, we have been able to get a few of our CBD brands into various convenience and conventional retailers, including one of the nation’s largest drugstore chains. Brands that see the value in KushCo ultimately recognize that we’re bringing them the opportunity to open up the retail channels and open up that bottleneck that we mentioned. Our early but modest success is only an initial indicator of what can really be possible through our unique platform which services the entire seed to sale process.

In addition, despite the lower dollar amounts of transactions in our hemp trading division, we’re actually seeing an uptick in the number of transactions overall. So, even though we’re seeing fewer home runs, so to speak, we are getting a lot more base hits. This activity has been very encouraging in the sense that it has required very little if any capital, has solidified our presence in this arena, and has opened the door to new opportunities within our ecosystem to cross sell additional products and services.

We also launched our Kush Commodities website, which has made it easier for sellers and growers to display their products on line, and for buyers to place bids on the purchase of those products. The website has already processed a few orders without any human interaction, creating a more automated and efficient exchange that customers can rely on.

Overall, we continue to see a significant opportunity within this higher margin and cash flow accretive category, and once the market is in a position to expand again, we will be operating with a solid track record, reputation, and platform, which can help us stand out from the crowd even further.

Lastly, I want to take a look at our Energy & Natural Products bucket.

This business was affected in Q2 because a lot of the brands and operators are still temporarily halting their production of oil. However, we expect for it to stabilize and bounce back as we see the demand for concentrates and vape pens gradually rising back to pre vape crisis levels.

We’re also seeing a shift from butane to ethanol, where we’ve capitalized actually on selling ethanol here in Q3 to some cannabis processors that are now processing hand sanitizer. We’re going to continue to ramp up our ethanol line, while strategically continuing to offer butane in key markets where we can be profitable.

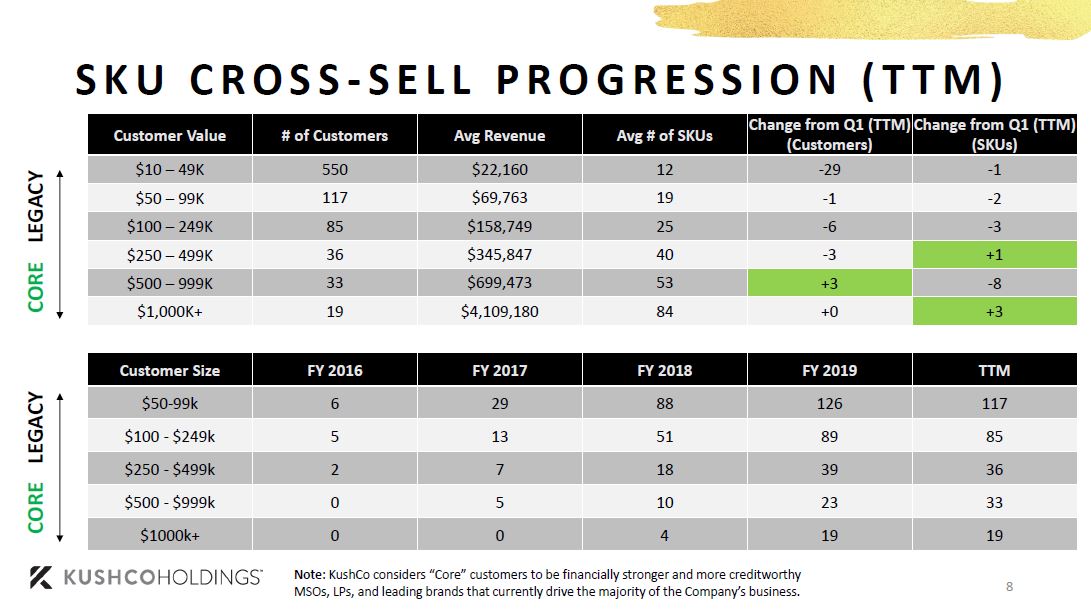

Next, I want to turn everyone’s attention to Slide 8, where we look at our cross sell progression. This is a familiar slide and a familiar theme for many of you who have been following the KushCo story, but it bears repeating that we continue to gain traction in not only securing larger customers, who we call now our core customers, but that we are also cross selling these customers more and more SKUs, as they continue to grow.

As I mentioned earlier, we had 52 customers purchasing more than $500,000 with us on a TTM basis; versus only 42, two quarters ago. And, on the other end of the spectrum, which is consistent with our new strategic plan, you’re seeing a little bit of an inverse effect, with smaller customers either churning, struggling to buy more with us, getting acquired, or simply going out of business. It’s data like this which makes it all the more clear as to the need for our strategic shift in the business to be more entrenched with our core customers.

As I mentioned earlier, we had 52 customers purchasing more than $500,000 with us on a TTM basis; versus only 42, two quarters ago. And, on the other end of the spectrum, which is consistent with our new strategic plan, you’re seeing a little bit of an inverse effect, with smaller customers either churning, struggling to buy more with us, getting acquired, or simply going out of business. It’s data like this which makes it all the more clear as to the need for our strategic shift in the business to be more entrenched with our core customers.

Lastly, before we dive into the new plan, I wanted to turn it over to Chris for some brief final remarks. As you all know, Chris will be leaving us later this week, but on behalf of everyone at the Organization, I wanted to thank him for his service and what he has contributed to KushCo during these past 18 months. Through his hard work and efforts, we have become a much stronger, more focused, and more streamlined organization, particularly in our finance department. Perhaps just as important, Chris has created a solid platform, team and process for Stephen to pick up as the new CFO moving forward.

So, thank you again, Chris. You’ll be missed, and we wish you nothing but the best in the next stage of your career.

Chris Tedford

Thanks, Nick.

It’s truly been a tremendous honor and pleasure to serve as the KushCo CFO during this dynamic period within the cannabis and CBD industry, and to be an integral part of the transformation the Company has experienced during my tenure.

As Nick mentioned, I’m very fortunate to have helped build and strengthen many core competencies within this organization, particularly the finance function, which I am extremely proud to have worked alongside a long list of highly talented colleagues and employees that will undoubtedly continue to deliver exceptional value for the Company.

I’d like to thank Nick, the KushCo leadership team and its Board for this incredibly valuable opportunity. It’s been a challenging yet exciting ride, and I’ve definitely enjoyed my time here at the Company.

Everybody please stay safe and be well.

I’ll now turn the call over to Stephen to walk through his prepared remarks.

Stephen Christoffersen

Thank you, Chris.

I just want to start off by thanking Chris for the work that he has done and the strong team that he has built. Especially during these past few weeks, I am grateful for his guidance and support, and for him working hand in hand with me to help shorten the learning curve in what is obviously a very critical and evolving role. So, thank you, Chris for everything you’ve done for the Company; we wish you nothing but the best on your next endeavor.

Before I begin my financial summary, I just want to share a little bit about myself for those that are unfamiliar. My name is Stephen Christoffersen and I joined the Company back in 2018 as the EVP of Corporate Development. Prior to doing so, I was sitting on the same side of the desk as many of you on the call, as a buy side portfolio manager, so I can appreciate where you all are coming from, and will continue to work tirelessly to ensure we can enhance shareholder value. Before that, I was the CFO of a start up beef jerky company, where I learned a lot about the CPG world which the cannabis industry is slowly trying to emulate. During that time, I also advised on several M&A and fundraising activities for various seed and growth stage companies.

At KushCo, I’ve been fortunate enough to have helped launch our hemp trading and retail services divisions, secure our line of credit, and help on various capital raising efforts. I am ready and excited to serve our employees, customers, and shareholders in this new and enhanced role, and welcome the opportunity to meet and work with anyone on the call who I haven’t already.

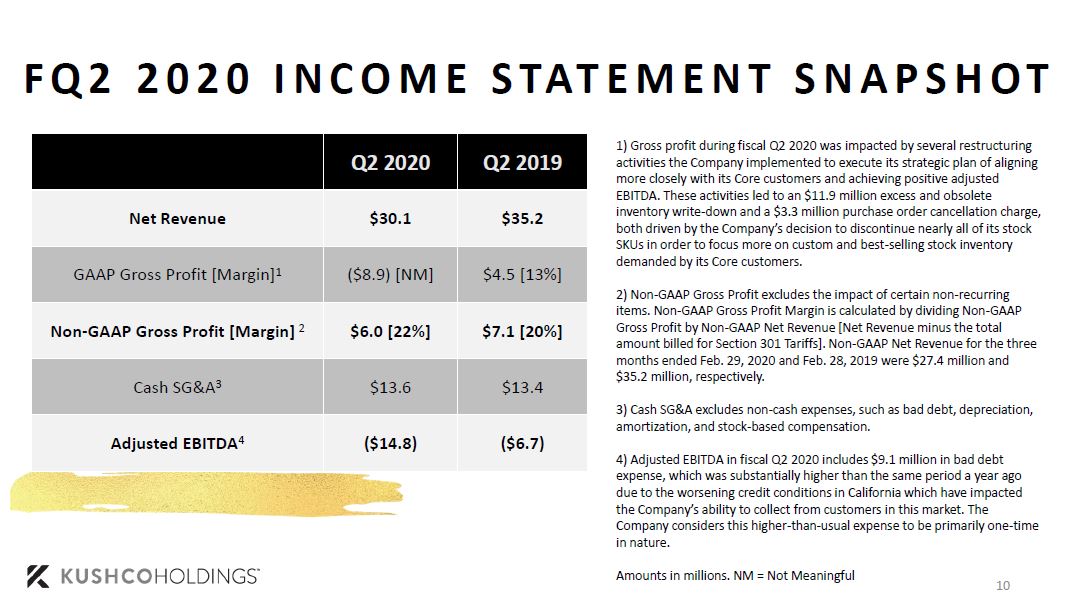

With that, let me turn to the financial summary, beginning on Slide 10, which displays a snapshot of our income statement for Fiscal Q2 2020. As Nick mentioned, we have a lot to cover on this call, especially as it relates to the new strategic plan, but also as it relates to the restructuring activities we implemented in the second quarter. Starting at the top, total net revenue decreased 14% year over year and quarter over quarter to $30.1 million. The quarter over quarter decrease was driven by lower sales of our energy and natural products and hemp trading services.

Starting at the top, total net revenue decreased 14% year over year and quarter over quarter to $30.1 million. The quarter over quarter decrease was driven by lower sales of our energy and natural products and hemp trading services.

As a reminder, because of our sales trends in the first half of Fiscal 2020, as well as the emerging developments of COVID 19, last month we removed our revenue guidance for the fiscal year.

On a GAAP basis, gross profit for the second quarter decreased to negative $8.9 million, from positive $4.5 million in Q2 2019. The decrease was driven by several restructuring charges we took during the quarter to right size the business and better align it with our new strategic plan. These charges included an approximately $11.9 million charge to E&O inventory, and a roughly $3.3 million charge for purchase order cancellations. I’ll now spend a brief moment going over each of these.

With respect to the inventory write downs, given our enhanced focus on MSOs, LPs, and leading brands, who largely purchase custom inventory versus stock items, we made the decision to discontinue nearly all stock items with the exception of our top 60 best selling SKUs. All inventory that was not aligned with this new inventory strategy was written down to its liquidation value, and as I’ll touch on later, with this substantial reduction in inventory, we concluded that we do not need a majority of our warehouse footprint either.

As it relates to the purchase order cancellation charges, a vast majority was due to the credit with one of our vendors, which we could have used had we purchased a certain volume of pre rolled cones from this vendor. Given the previously mentioned shift in inventory strategy, however, we will no longer be focusing on purchasing and selling these types of pre rolled cones, and as such we will not be purchasing the minimum volume of products required for this vendor to issue this credit back to us.

On a non GAAP basis, excluding the impact of the China trade tariffs and these inventory write downs and purchase order cancellations, gross profit was approximately positive $6 million, or 22% of net revenue, compared to 20% in Q2 2019. For a more complete reconciliation of GAAP to non GAAP financial information, please visit the reconciliation table at the end of this presentation or in our Q2 earnings release.

SG&A expense for the second quarter of our Fiscal ’20 was approximately $27.2 million, which was up approximately $8.4 million compared to the prior year second quarter. The increase was driven mainly by the significant year over year increase in bad debt expense, which totaled $9.1 million for the quarter. The major uptick in bad debt expense was largely due to the worsening credit conditions in California, which have impacted our ability to collect amounts owed by customers in this market. This just demonstrates why we have moved so rapidly to shift away from this customer group to the more optimal group: that we can build a sustainable and profitable business for years to come.

Now, let’s look at our cash SG&A, which excludes non cash expenses such as bad debt, stock based comp, depreciation and amortization. Cash SG&A in Q2 2020 was approximately $13.6 million, compared to $15.1 million in the previous quarter, and $13.4 million in the same period a year ago. As we’ve previously indicated via press release, we have significantly reduced our headcount by nearly 50% since September 2019, and this has been complemented by a substantial reduction in our third party consulting costs. As a result, we expect cash SG&A to significantly come down in the second half of Fiscal ’20.

The next slide item I wanted to cover on the income statement is Restructuring Costs. This $7.3 million expense was related to severance costs and asset impairment charges associated with both recent reductions in force as well as warehouse facilities that we are currently planning to consolidate. Now let me spend a moment briefly going over each of these.

As it relates to the severance piece, we previously mentioned that we are implementing a more efficient and automated approach toward doing business with our smaller customers, one that requires substantially fewer dedicated sales representatives and other related headcount. In addition, because our new strategy focuses on fewer overall customers, we determined that certain positions are no longer essential to the execution of our go forward strategy. As a result, we underwent two reductions in force, as Nick had mentioned previously. The reduction in force during Q2 resulted in 26 terminations and approximately $379,000 in severance related restructuring costs.

Looking at the asset impairment charges related to our warehouse consolidation, we were currently in the process of negotiating with our landlords to terminate leases and exit the impacted warehouses. With these planned facility closures, we determined that our fixed assets at these closing facilities required an impairment charge. We also determined that our product molds and tooling are now no longer necessary assets, given the Company’s shift to focusing exclusively on custom and best selling stock inventory, requiring an additional impairment charge. As a result, we recognized a total impairment charges of $3.9 million for these fixed assets during the second quarter. Given the decision to consolidate facilities, we determined that we would incur an impairment charge to our right of use assets. This charge was approximately $3 million in Fiscal Q2 2020.

To summarize, these are all the items that got lumped into the $7.3 million restructuring costs for the quarter. But we expect a much cleaner financial picture and much leaner and stronger business moving forward.

Turning to the next item, on a GAAP basis, net loss for fiscal Q2 was approximately $44.4 million or negative $0.40 per share, as compared to a net loss of approximately $8.9 million or negative $0.10 per share in Q2 2019.

On a non GAAP basis, excluding the impact of certain non recurring charges, such as the restructuring charges that I went over, as well as the other non cash gains and losses, our net loss for the quarter was approximately $17.5 million, or negative $0.16 per share as compared to a negative $0.09 per share in Q2 2019.

Last but not least on this slide, Adjusted EBITDA was equal to negative $14.8 million, compared to a negative $6.8 million in Q2 2020 and negative $6.7 million in Q2 2019. Adjusted EBITDA loss was higher this quarter compared to the prior quarter because of the roughly $9.1 million in bad debt expense that is considered a normal part of business, but should really be considered one time in nature in our opinion. If you exclude this expense, Adjusted EBITDA loss for fiscal Q2 would have been around $5.7 million, which more accurately demonstrates that we are moving closer to our target of positive Adjusted EBITDA. Later, I will walk through a couple different scenarios of how we can get there.

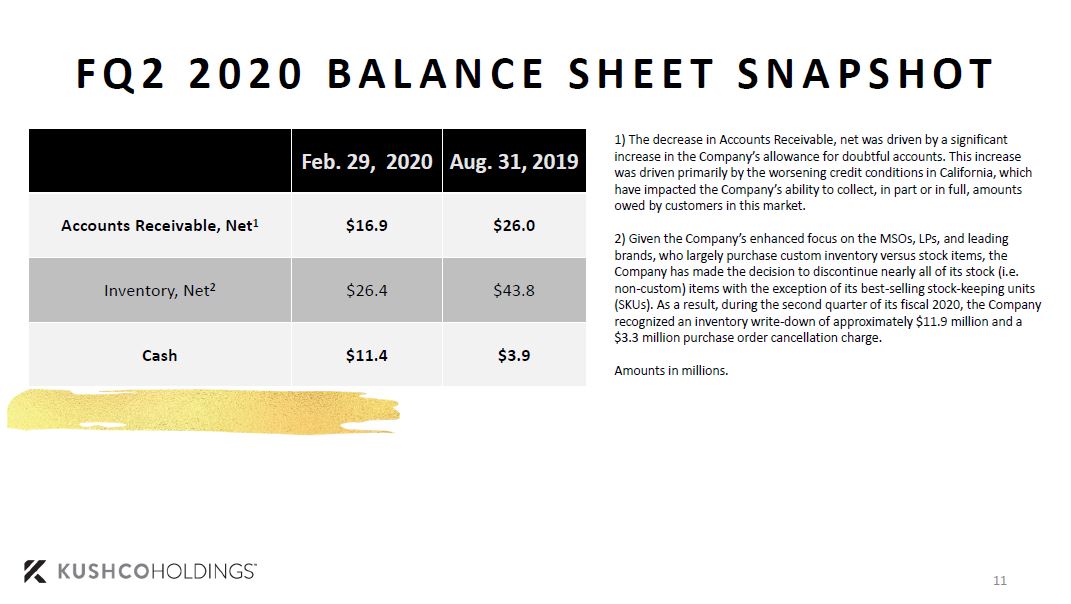

Turning now to Slide 11, which provides a snapshot of our balance sheet as of the end of the fiscal Q2. First, you’ll notice that accounts receivable was down significantly from the end of Q4 2019, driven primarily by the increase in allowance for doubtful accounts, which I touched on earlier, due to the deteriorating credit conditions in California. We can’t stress enough how much we are tightening our credit standards, and we are laser focused on only extending credit going forward to our top tier customers.

First, you’ll notice that accounts receivable was down significantly from the end of Q4 2019, driven primarily by the increase in allowance for doubtful accounts, which I touched on earlier, due to the deteriorating credit conditions in California. We can’t stress enough how much we are tightening our credit standards, and we are laser focused on only extending credit going forward to our top tier customers.

Our total inventory as of the end of Q2 was approximately $26.4 million, compared to approximately $43.8 million as of Q4 2019. The major driver for the reduction was the previously mentioned excess & obsolete inventory write down. We are becoming much smarter about the type of inventory we are purchasing, making sure that it is closely aligned to the more custom products for our top tier customers, as well as the very high velocity stock inventory items. We are very pleased that the inventory we have in stock today is of much better quality and turning faster than the inventory we had just a few weeks ago.

Last, on this slide, I wanted to touch on our cash position, which was approximately $11.4 million as of the end of fiscal Q2. During the quarter, we completed a registered direct offering which yielded approximately $15 million in net cash proceeds. While we were fortunate to capitalize on an opportunity to raise more capital from a largely existing shareholder base, we recognize that the capital markets have dried up for many, and we need to operate under the mindset that there won’t be another dollar of equity capital for us to achieve our goal of positive Adjusted EBITDA. We believe we’re in a good cash position to reach that goal on our own, given our healthy cash position and line of credit. But beyond these liquidity sources, I’m looking for additional ways, as CFO, to drive our current cash flow from operations.

One of my main priorities is to enhance our collection efforts. I believe there are areas where we can go even deeper and make sure that we can get paid on time. This includes tightening our credit terms from our non core customer base, partnering with outside agencies who work on a success based commission, and trying to recoup value from excess and obsolete inventory, among other measures that we are considering and putting forth into action. These efforts, along with our continued cash SG&A reductions through right sizing our headcount, facilities, and consulting costs, should ultimately give us the cash flow needed to support our business as it reaches closer toward positive Adjusted EBITDA and self sustainability.

With that, I’ll turn it back to Nick to kick off our discussion for our new strategic plan.

Nick Kovacevich

Thanks, Stephen.

Now we are going to turn our attention to the last portion of our prepared remarks, which focuses on our new strategic plan to accelerate our path to positive Adjusted EBITDA. We have talked about it a lot already, so we’ll try to keep this brief and focus more on bringing all the pieces together so that everyone knows our go forward strategy and can see the ways that we can get to our goal of positive Adjusted EBITDA.

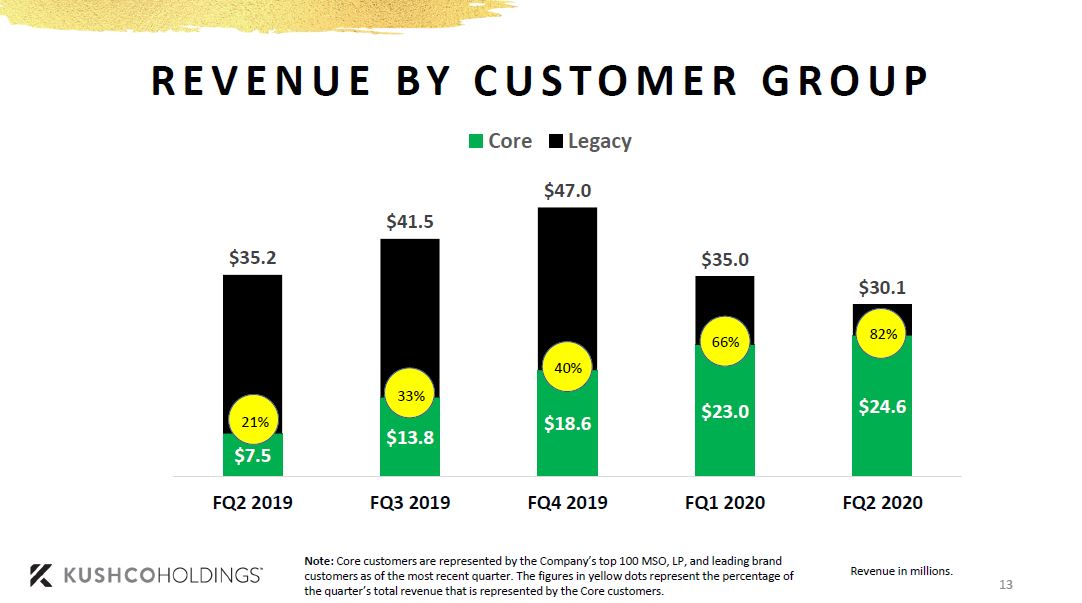

To start this discussion, I’d like to turn your attention to Slide 13, which provides a breakdown of our total revenue by Core versus Legacy customers. If I were to explain the rationale for our strategy in a single picture, this would probably be it.

As you can see, as the quarters have progressed, more and more of our revenue is being driven by a Core group of elite customers, even in the midst of macro headwinds that have brought the total revenue down. In Q3 2019, prior to the start of the illicit market vape crisis, only 33% or $13.8 million of our total revenue that quarter was driven by these core customers. But, following the onset of the crisis and the liquidity challenges it created, especially for the vast majority of our smaller customers, our growth, much like that of the industry, was challenged, and we knew we had to shift quickly to more established, financially stronger and more creditworthy customers.

As you can see, as the quarters have progressed, more and more of our revenue is being driven by a Core group of elite customers, even in the midst of macro headwinds that have brought the total revenue down. In Q3 2019, prior to the start of the illicit market vape crisis, only 33% or $13.8 million of our total revenue that quarter was driven by these core customers. But, following the onset of the crisis and the liquidity challenges it created, especially for the vast majority of our smaller customers, our growth, much like that of the industry, was challenged, and we knew we had to shift quickly to more established, financially stronger and more creditworthy customers.

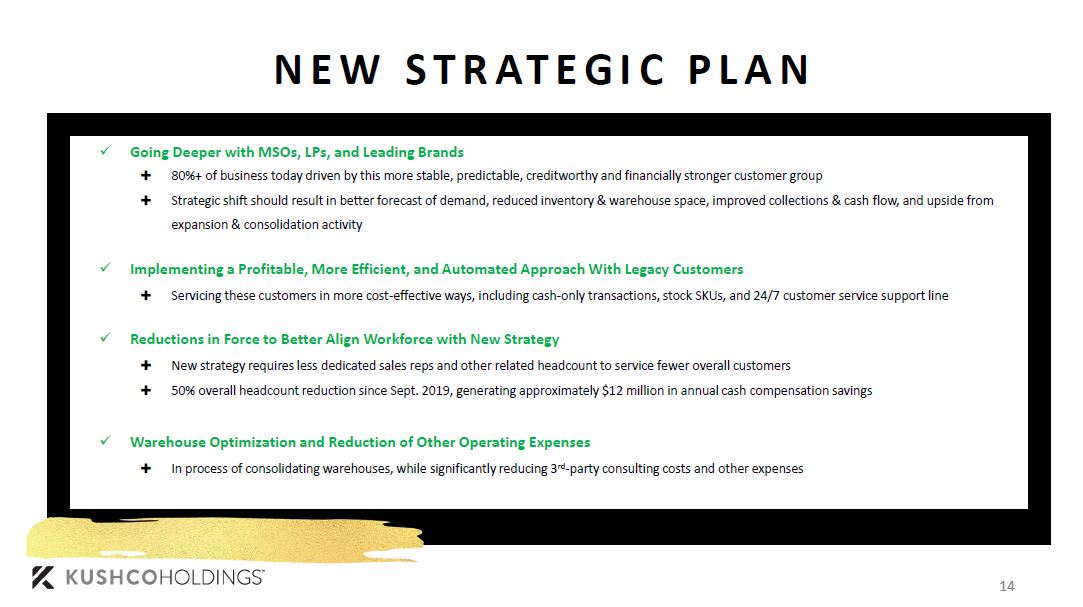

The good news is that we have been able to secure many of the top MSOs, LPs, and leading brands, which made up 82% of our business in fiscal Q2. Now we just need to make sure the rest of our business, from a cost perspective, is aligned with that strategy, and you are seeing a lot of that here with the cost cutting and right sizing activity. Now I’ll turn your attention to Slide 14, which summarizes a lot of the steps we took and are taking to make sure that the rest of our business is aligned with this new strategy. For the sake of time, I won’t go through all of these bullet points, but I will just call out a few. Namely, this strategy should result in a better forecast of demand, has and will significantly reduce our inventory and warehouse space, should improve our collections and cash flow, and perhaps most importantly gives us that upside to grow in a meaningful way again once the industry starts to turn and these core customers ramp up their consolidation and expansion activity.

Now I’ll turn your attention to Slide 14, which summarizes a lot of the steps we took and are taking to make sure that the rest of our business is aligned with this new strategy. For the sake of time, I won’t go through all of these bullet points, but I will just call out a few. Namely, this strategy should result in a better forecast of demand, has and will significantly reduce our inventory and warehouse space, should improve our collections and cash flow, and perhaps most importantly gives us that upside to grow in a meaningful way again once the industry starts to turn and these core customers ramp up their consolidation and expansion activity.

The other thing I wanted to call out is that we are still servicing our smaller customers, and are happily doing so, but we have to be smart about how we do it. We have to cut out our old ways, because this industry isn’t about building empires and focusing on growth at all costs anymore. It’s about how we can build a sustainable and long lasting business. We understand this might lead to some attrition, as some of our cash strapped customers may look elsewhere for credit terms or for better high touch service. But the customers that do stay with us recognize the value we bring, not only from a service but also from an offering perspective, and that we stand ready to grow alongside them, but we can’t be left holding the bag if things go awry.

Last but not least, when the revenue is outside of our control, we want to focus on what is within our control, and as you can see here we certainly have done that, namely with the headcount reductions. We are now not only leaner and a stronger organization that can take advantage of this market shakeout, but also an organization that can self sustain and control our own destiny by improving profitability and cash flow metrics. That is what our focus has been and what it will continue to be, until we achieve and after we achieve our stated goal of positive Adjusted EBITDA.

And so, let me now turn it back to Stephen to bring it all home and walk you through the different scenarios that can help get us to that goal.

Stephen Christoffersen

All right. Thanks Nick.

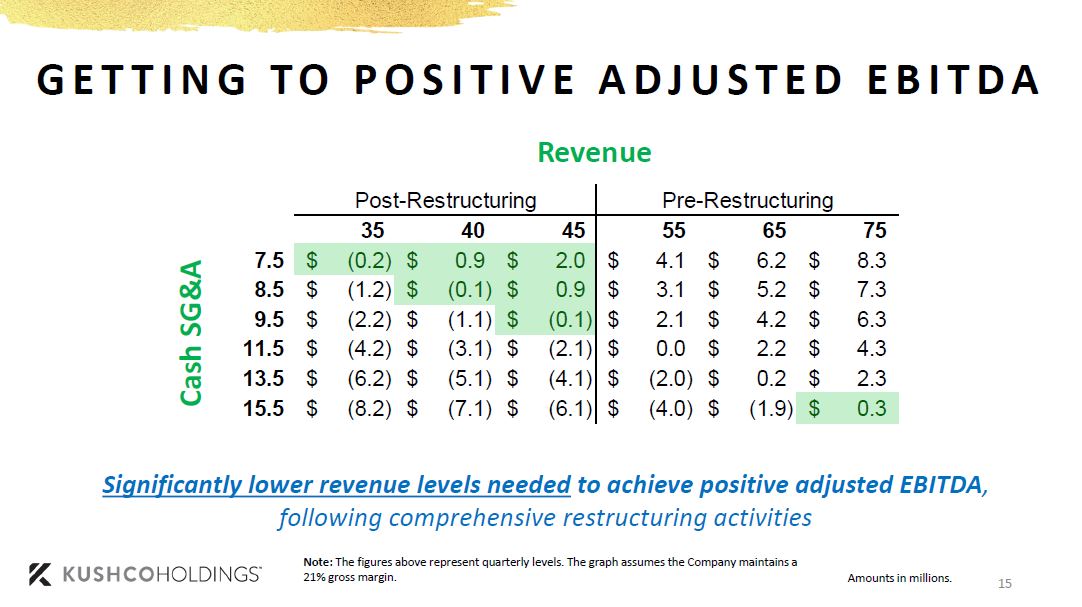

Let’s wrap it up by turning here to Slide 15, which outlines several different scenarios for how we can get to our goal of positive Adjusted EBITDA.

At the top, from left to right, there are different quarterly revenue levels; and on the left, from top to bottom, there are different quarterly SG&A levels. In the middle, of course, are the possible Adjusted EBITDA results that could occur under different combinations of the revenue and cash SG&A, assuming we maintain a 21% gross margin, which is a good historical precedent.

At the top, from left to right, there are different quarterly revenue levels; and on the left, from top to bottom, there are different quarterly SG&A levels. In the middle, of course, are the possible Adjusted EBITDA results that could occur under different combinations of the revenue and cash SG&A, assuming we maintain a 21% gross margin, which is a good historical precedent.

The big takeaway here is that with the restructuring activities that we are undertaking, we will have significantly lowered the revenue bar to achieve positive Adjusted EBITDA.

If you look at the bottom right most cell, you’ll see that the $15.5 million in cash SG&A, we would need to generate roughly $75 million in revenue in order to achieve our goal. Fifteen-point-five million dollars is not an arbitrary number. It’s virtually the amount of cash SG&A we reported in fiscal Q1, underscoring the tremendous revenue climb we would have had to achieve in order to reach that goal.

Simply, with everything that’s been going on from a macro perspective, those quarterly revenue levels are just not achievable within this current fiscal year, which is why, as Nick mentioned, we are focused on things we can control, which are our costs.

After all these restructuring activities are complete, we expect cash SG&A to drop from $15.5 million in Fiscal Q1 2020 to between $7.5 million and $8.5 million in Fiscal Q4 2020, which is even lower than the $9.5 million in Fiscal Q4 2020 we had previously forecasted. This now puts us in a much more feasible position of only having to achieve between $35 million and $45 million revenue to hit our same goal of positive Adjusted EBITDA.

We really wanted to bring this all together to show how we’re looking at the business, what’s probable from a financial standpoint, and where we can pull back the most from a cost perspective without impairing our sales outlook. Fortunately, because we’re already aligned with the core customers from a revenue standpoint, it made a ton of sense to align the rest of the business with these customers as well, which significantly reduces our costs.

We think these results are very achievable within the next couple quarters, and are hyper focused on executing the remainder of our right sizing activities, while going deeper with our core customers.

With that, I’d like to turn it over to the Operator for the Q&A session.

Operator

Thank you. We’ll now be conducting a question-and-answer session. If you like to be placed in the question queue, please press star, one on your telephone keypad. A confirmation tone will indicate your line is in the question queue. You may press star, two if you’d like to remove your question from the queue. For participants using speaker equipment, it may be necessary to pick up your handset before pressing star, one. One moment please while we poll for questions.

Our first question today is coming from Vivien Azer from Cowen, your line is now live.

Vivien Azer

Hi. Thank you. Good afternoon. Appreciate all the detailed disclosure, and in particular the restructuring outlook.

So just starting with that, the revenue outlook that you guys have laid out here would imply an improvement in the back half. Some of that inventory maybe accounts for some of that, in terms of kind of the missed orders from a timing perspective. But just wanted to dig in, given the uncertain current backdrop, why you didn’t take a more conservative view in terms of scenario analysis you offered on Slide 15. Thanks.

Nick Kovacevich

Thanks Vivien. I think you did hit it on the head. We have a little bit of revenue coming in from Q2 that didn’t hit moving into Q3, so we feel we’re starting off in a pretty good place, plus we all saw the big run up in March.

But we gave a scenario just showing kind of our new path to profitability. We’re not necessarily guiding to those revenue numbers, because of the uncertainty. We know that things are changing on the fly here. Massachusetts decided to ban. Ontario banned. Now they’re not banning, they’re allowing delivery. So it’s really impossible for anyone to predict how this is really going to play out throughout the coronavirus. So we’re not going to play that game. But we’re going to control what we can control, and we’re cutting costs down to a certain point that it becomes a very achievable revenue threshold.

Now, will these outside factors potentially influence it in the wrong direction? Maybe, we just don’t know.

We can only control what we can control. We feel very confident about our core customer revenue base and being able to get growth from that customer base. We feel very confident about getting our costs in line to where we outlined it, $7.5 million to $8.5 million in SG&A. Outside of that, your conclusion’s as good as ours, because we just don’t know how things are going to change here in these next few months.

Vivien Azer

That seems reasonable.

Just, sticking with some of the really interesting detail that you guys offered in the deck, on Slide 13, the revenue mix, so what you now define as your core customer versus legacy group, is certainly encouraging, just in terms of the predictability of the revenues. But I do think it begs the question, like how does that influence how you think about your TAM, like the addressable market now? Because there are a far more finite number of, you know, large, you know, multi outlet established multi state MSOs; so like where do you think you are from a penetration level? SKU growth aside, right, recognizing that even if you like got to 100% of the customers that you would want to deal with, you could still grow that business because you’d grow with them. But just in terms of the customer base itself, where do you think you are from a penetration standpoint, as you view it through this new lens? Thanks.

Nick Kovacevich

Actually that’s a really good question. Not surprised by you, Vivien, but great question. I think, you know, we haven’t ran the numbers, but as sort of off the cuff, we feel like we’re somewhere around 50% of where we want to be with that Core group, so there’s a 50% bigger opportunity within what we would feel a very stable and secure customer base that we can go after, and then of course there’s still everybody outside of that group, and we’re not saying no to their business, we just are not going to focus on it, we’re not going to have a sales rep, we’re not going to pay commission, we’re not going to allow for credit terms so it’s going to be mostly cash up front business. So we’ll still get some of that.

And then we’ve got to wait for the shake out. We know that the amount of cannabis being sold continues to go up; problem is, the amount of players that are selling it keeps shifting, right, and there’s folks that are today, I mean we’ve even seen here recently, some of the bigger MSOs that everyone would think is in stable financial condition, now going into receivership.

So you just have these crazy dynamics happening, and so we’re going to say hey, there’s a bunch of opportunity over there that we’re going to worry about later, but there’s a good chunk of opportunity right in front of us, and that’s sort of the 50% that we have today that we can grow, and that’s the 50% outside of that that we would put into this Core bucket, that we don’t have today and we’re going to go get.

Vivien Azer

Got it. Okay, that seems reasonable. So, just to paraphrase and repeat back to you, focus on your core customers today, there’s a 50% customer opportunity that you’ll attack down the road, but you want to get kind of the business right sized and get through the restructuring first.

Nick Kovacevich

Yes, but I will say, we’re actively going after that other 50%. Anyone that meets a certain profile that we could call a core customer, and some of them, you know, it’s the whole range, right? So there’s some of these core customers that we’re doing a lot with today, and sure there’s going to be some opportunities in the future, and then those customers are going to grow. But we’re pretty well saturated. Then there’s some of these customers that we’re doing some with today, and we could do a lot more with. And then there’s even a few customers that we want in this bucket, but we’re really not doing any business with them today.

So when you think of the missed opportunity within what we would want to call our Core group, there’s still 50% we estimate or more out there that we’re going after today. We’re not waiting on that. What we are waiting on is anyone that would be outside of that Core group, that wouldn’t really qualify as a core customer from a balance sheet or footprint standpoint. That’s who we’re going to push off, and we’re not really going to worry. If they come to us, great, we’ll service them, but we’re not going to go try to track them down, because we think there’s going to be a lot of turnover and shake out, and we’re going to kind of wait and see how this plays out.

So hunker down on the core customers, and future new core customers, and wait on the rest of the group until we kind of see how things play out.

Vivien Azer

Perfect. That’s helpful.

Last one for me and then I’ll get back in the queue. Just looking at Canada, obviously really nice sequential growth in the quarter. Any way to unpack what proportion of that came from channel fill on 2.0 products versus legacy products that were already in the market? Thanks.

Nick Kovacevich

The majority. We’re very pleased to finally see Canada coming to life for us, and we’ve got some momentum now in that market. It was really driven by 2.0. A lot of people had flower packaging from their medical days, and they kind of transitioned that into new adult use. When 2.0 was going to be announced and rolled out, that’s when we started to engage in dialogue around designing new form factors for packaging for those products, around engaging around vape sales. That’s really what led to this lift, so I would—if we had to call it, I’d say 75% to 80% was driven by 2.0 products.

Vivien Azer

All right, perfect. I’ll go back into the queue. Thank you so much.

Nick Kovacevich

Thank you.

Operator

Thank you, our next question is coming from Aaron Grey from Alliance Global Partners, your line is now live.

Aaron Grey

Hi. Thanks for the questions. First, Chris, just want to add my best wishes in your future endeavors, and Stephen, congrats on the new role.

So, my first question, I just want to hop back in terms of you know sequential growth, you know as you look to kind of rebase, you did disclose non GAAP revenues of $27 million, so is that kind of the new base of how we should think about revenues to kind of build off of, going into the next quarter?

And then, just based on that too, stepping back on commentary on medical markets and timing. So, as we look at that specific align (phon) to have been growing pretty nicely for you guys, should we think of that new base being more of the $11 million than we had seen in the quarter before, versus $7 million this quarter? Does it kind of jump back to that, or is it still kind of a slower build to that in terms of the timing and issues that going to be resolved? Thanks.

Nick Kovacevich

Okay. The first part of the question, essentially around revenue, the $27 million would be excluding the tariff surcharge, so right now we’re paying for tariffs and then we’re passing them on to customers. So we expect tariffs to continue to be in effect for some time now. Be great if they went away, but I don’t think we can bank on that. We do expect—$30 million is a solid base.

Now what we pointed to in the slide about the core customers is 82% of that was driven by core customers. So you can expect that our focus right now is primarily 99% on growing that core customer revenue, that 82%. You could almost look at it with we’re starting at that sort of that $25 million range, that we’re going to grow. Now there’s an extra group of customers that we’re not going to lose overnight, but we do expect some attrition. So hopefully we’re growing the core bucket faster than we’re losing in the non core bucket, and we can then continue to grow revenues.

We have a little bit of head start in Q3 with some of the carryover from the COVID 19 supply chain delays out of China. We also have benefited a little bit from selling some ethanol to hand sanitizer producers.

So there are some things in Q3 that we could expect growth, but we’re very cautious to guide to that, because of everything that’s changing dynamically on the COVID side, right. We don’t know what markets are going to stay open and what aren’t. California deems cannabis all to be essential and to be open, and then all of a sudden Santa Clara County, as an outlier, says no, we were not going to allow it, right? So that’s completely out of the blue. We just don’t know what’s going to happen.

If things stay the way they are, and these markets continue to stay open, and our shipments all arrive from China that are coming over right now, yes, we do expect we can grow off of that $30 million base going from Q2 to Q3. I mean that we’re not going to give guidance for Q4 either, but we’re going to basically show you guys, as we did, that the bar to get to profitability is much lower, and we believe that we can achieve that here in the near term, assuming that these market dynamics do stay in place.

So the second part of your question, what was it around?

Stephen Christoffersen

Can you repeat that second part, Aaron?

Nick Kovacevich

Yes, go ahead, Aaron.

Aaron Grey

Just on the medical markets, just how best think about it in terms of the timing shift? So should we kind of think about it rebasing to what we saw, I think it was $11 million, in the quarter before, just kind of shift right back because it was just a timing issue?

Nick Kovacevich

Yes.

Aaron Grey

Okay.

Nick Kovacevich

Yes. That should shift right back, and we’re going to—Massachusetts sales are going to be primarily medical, but we’ll be booking those into adult use. These buckets are a little bit fluid, there’s some overlap.

But yes, I mean look, we’re not—there’s nothing wrong with the medical sales, they’ve been trending great, right? If you look at our new core customer kind of profile, most of them are operating in medical markets, right? The traditional rec markets like Colorado, Washington, Oregon, California, they don’t have MSOs. Why are the MSOs not in those markets? Because the markets are tough to drive a profit, which is why a lot of the companies that are doing business in those markets can’t pay their bills. Right? So it all lines up with everything you guys are seeing, it’s just unfortunate, because we had a lot of traction in these markets and we wish that the dynamics were better and these operators could do well and prosper, which would then in turn allow us to do well and prosper. But for now people are moving to limited license markets, medical markets, to get better margin and better profitability, and we’re following them there.

Aaron Grey

All right great, thanks, I appreciate that.

Just one more and then I’ll jump back into the queue. Just on gross margins. Is there anything to think about in terms of the different gross margin profiles generally between the smaller customers and then the new core customers? Just anything based on product type, in terms of mix, or rates, or how to think about that going forward that might change how to think about the gross margin evolution for the company? Thanks.

Nick Kovacevich

Gross margin percentage obviously has been fairly important for our business, but as we look to make the turn to profitability it’s going to be probably less important, right. So we’re looking at this more as what’s more profitable gross margin dollars: to get 25% gross margin on a $100,000 order, or to get 20% gross margin on a $1 million order, right? At the end of the day it takes slightly more work to shift that $1 million order, and we’re going to get a lot bigger number of absolute gross profit dollars. So we’re going to be a little less concerned around margin as we look to move into profitability, and we’re going to be more concerned with how we capture large swaths of gross margin dollars through these larger transactions with the bigger customers.

In terms of how it’s going to play out, I mean we see the MSOs and LPs obviously having better buying power. So we’re going to have to be aggressive when we come in and price, but that said, a lot of them are looking at custom solutions. And with custom solutions there’s a lot of R&D work and tooling, and so we actually end up having better margins. In a sense we actually look at, on the packaging side, potentially having margin enhancement going to this new model. We know that the vape products are pretty much priced where they’re at; I mean there’s sort of a minimum allowed advertised price that we can do with CCELL, and so there’s really no discount on the vaping stuff. So we expect that to stay intact.

Over all, I mean, look, larger customers, they should get better pricing and they will. But as we focus on less SKUs, obviously our cost on those SKUs should come down too.

We think that margin percentage may come down a little bit, but as we get better at what we do and more efficient, we can probably save and be able to keep it similar to where it is.

For now, we’re basically thinking it’s going to stay where it is, and go up like we’ve always suggested, as we get more efficient, and if that were to change we would obviously update.

Aaron Grey

All right great, thanks.

Operator

Thank you, our next question is coming from Bobby Burleson from Canaccord, your line is now live.

Bobby Burleson

Hey guys. Thanks for taking my questions.

So, just as a couple here. If we look at the states that you had some pretty good strength in the quarter, and obviously Canada as well, what did the recent demand trends look like there? Obviously there’s been some better seasonal demand that we’re seeing in March and that may be carrying over into April; I’m just wondering, from your viewpoint, whether or not you’re able to kind of look through and maybe get a glimpse at what that point of sales data looks like.

Nick Kovacevich

We’re looking at the same data you probably are, right, the BDS data and Headset data, and obviously a lot of articles written about the strong March across the board for cannabis. Seems to have leveled off at the retail, right, and most retailers are back similar to where they were prior to the run up. We’re not going to read too much into it. We’re looking at obviously markets that are changing their regulations, either moving to the delivery curbside only, shutting down adult use entirely in the case in Massachusetts. That’s going to have a much bigger impact in terms of sales, but where we’re really getting the guidance now as we hone in on these core customer groups is just around expansion and growth in these key medical markets and new emerging markets like Illinois, Michigan.

We see the growth continuing. People are giving us very, very positive feedback. We know that the demand for these products in some states is outstripping supply. So a lot of the MSOs are really forecasting their business based on, hey, they’re going to sell 100% of what they can produce, and this is their production capacity ramp, right.

It becomes a little easier to determine in these limited license markets. And then you got markets like California that have an illicit market and illegal storefronts, and so how much business is shifted over there, especially in a county like Santa Clara County, where they’ve banned legal retail, I can guarantee you, they’re giving a lot of business to the illicit retailers.

All these factors at play, I mean we don’t see too much of it in real time for our business, because we’re a couple of steps removed. But as you see more people purchasing at the retail level, that means they’re going to sell through, the brands are going to sell through, and they’re going to need to buy more stuff from us. So eventually it does trickle back, and I think at this point everyone’s very optimistic and positive about cannabis sales throughout this COVID pandemic, but we know it’s also a very fluid environment so it’s too early to really say where it’s going to ultimately end up, and we have to exercise some caution.

Bobby Burleson

Okay great, thanks for that.

And then speaking of some of these growth areas and expansion with your core customers, in the past you’ve talked about having to kind of invest in new markets to be prepared for those expansions. I’m wondering, are you seeing anything in terms of headwinds on licensing or construction delays, just in your customer base, that might cause you to pause being as aggressive in terms of building out in conjunction with where their plans might be?

Nick Kovacevich

Great question. I’m glad you brought this up, because it’s actually part of the dynamic that’s changing under our new strategic plan, which is really tied—dictated by what’s happening in the market. What’s happening in the market is, again, years ago, even not too long ago, people in these markets, there was a lot of players, and it was a new market, it was kind of a free for all. So we saw a lot of success by putting infrastructure in these markets; being able to allow for cash and carry, as a lot of people were under banked; being able to take advantage of a surging market where a lot of new players were coming in, buying their tools and their supplies to get into the market, and ultimately trying to find success. Well, fast forward, a lot of these smaller folks have had tougher time finding success, and a lot of these newer markets that are opening up, they’re starting very limited in nature. Illinois for example, right, very few players are allowed to be active in Illinois today; they’re a few months into their new adult use market.

So the dynamics have actually changed. Whereas it used to be very strategic and opportunistic for us to invest in these new markets and put boots on the ground and large infrastructure, that’s going away, and now as we focus on these core customers we can be a little bit more tactile and strategic about our operational footprint, make sure that we’re in the right areas to be able to support these companies, but we can do it in a way that’s much more cost efficient as we’re not going to be chasing the herd of these new brands that are popping in, because quite frankly a lot of them haven’t had staying power and also, as we look at the downturn in the capital markets, a lot of these new incumbents won’t even get the funding to be able to try to play.

The dynamics have changed significantly, and we’re always changing along with it, we wish we could get out ahead of it, and we try to at times, but right now we’re just reacting to what the market’s telling us. These smaller customers, everybody was building a brand, everyone had a lot of optimism behind it; that dynamic is going away, and the MSOs and LPs are really the ones that are systematically expanding into new markets and taking share, and we’re aligned and we’re aligning better with that customer group, which is all part of this new plan and adjusting to what the market’s giving us.

Bobby Burleson

Great, thanks, and just one last one.

Nick, or Stephen, I’m wondering just with the focus on custom going forward, what type of R&D we should think about as a percentage of sales, kind of whether or not that’s going to creep up; and then is there any incremental risk in terms of inventory when it’s custom, versus the kind of standard products that you guys were carrying?

Nick Kovacevich

What we’re going to is a model where we’re offering custom solutions for a select few customers, right. For the most part they’re going to be paying to be able to go down these roads. We’re not expecting a big uptick in R&D or anything like that. There will come a time at some point in the future where hopefully we want to invest more in R&D. But for now we’re being very cost conscious; we’re doing what’s necessary for the core business, and when there is appetite for custom projects, we can apply resources, but as long as it’s being paid for and subsidized by the customer. So that’s primarily for the most part on the custom side.

And then when we look at the stock inventory, we’ve identified really 70 or so SKUs that are very fast moving, that have high turn, and it covers the sweet spot for us, items that we can source at really good price points, so we have competitive advantage. That’s the items that we’re going to be keeping in stock. If anyone wants anything outside of that, we can get it for them, but there’s going to be a lead time, there’s going to be a deposit; for some customers, it’s going to be a 100% deposit, so it’s probably going to deter people from doing that. We don’t want to spend a lot of resources going and sourcing some new custom item for somebody that needs 2000 or 5000 units that might not even be around come year end.

So it’s the right strategy and it’s actually going to lower all of our costs associated with it, and it’s going to increase our turns and allow us to run this business more efficiently with less inventory and tying up less of our cash.

We’re actually really excited about this model for numerous reasons, because again these are the right customers, we expect big growth, and we know it actually helps optimize our business on the cost and cash flow side of things.

Bobby Burleson

Great. Thanks for those answers.

Nick Kovacevich

You’re welcome. Thank you.

Operator

Thank you, our next question is coming from Scott Fortune from Roth Capital Partners, your line is now live.

Scott Fortune

Good afternoon. Real quick, any update on the supply chain from China? I know they’re getting back turned on, but any issues from the (inaudible) side on the China side of things?

Nick Kovacevich

A lot was made out of the China supply chain issues for companies. Our opinion’s always been that, of all the issues of COVID 19, the Chinese supply chain is actually one that’s very temporary and short term. So we’re not very concerned about it. Yes, there was delay. There’s now a little bit tougher time getting carriers to move the goods. But for the most part, the factories are back at 80% plus capacity. They’re producing these goods. We have goods coming over right now. We have goods landing in the ports all month. We expect, when we look at come May, this supply chain issue or disruption or delay, whatever you want to call it, from China will be virtually done with completely, right.

So it has been challenging, but it’s very temporary, and we haven’t seen much of a material negative impact to the business. People are just having to wait a little bit to get the stuff that they want. But the good news is, like I said, the stuff is coming, it’ll be here, customers will get it, and then on a go-forward basis there really should be very little disruption to supply chain out of China.

Scott Fortune

Okay. Thanks for the color.

And then, real quick, kind of a high end level question on kind of legalization now. Obviously COVID’s putting an impact on a lot of these states, and we’ve seen a pause or pushback on some legislation measures, New York more recently. What’s your outlook now as far as legalization for either rec or medical states in 2020? Do you see it continuing to be a robust opportunity to add on four or five more new states this year, or more of a hold delay process here?

Nick Kovacevich

I mean, putting on my Company hat, we’re operating this business like there’s no more capital coming into the sector, there’s no new big markets opening up, there’s no federal legalization that’s going to save the day. That’s how we’re operating, right? But putting my optimistic cannabis enthusiast hat on, yes, I think there’s going to be some states that legalize this November, states that have ballot initiatives. Obviously states that needed to do it legislatively, like New York, are a bit distracted right now, so it’s unlikely to happen. But I think also the momentum should be bigger post COVID, as a lot of these states are going to be depleting their budget surpluses, and they’re going to be needing to look for new ways to generate meaningful tax dollars, and as we all know cannabis is one of the biggest tax generators dollar for dollar than any other industry here in the U.S. And the other thing people need right now with record unemployment is going to be jobs, and we know cannabis, dollar for dollar, is probably the biggest job creator in the U.S. as well.

I think all of that bodes well for future momentum, but I just don’t think it’s something that any of us should be operating our businesses based on, given that we’ve had delay after delay, we’ve had mismanaged regulatory process after regulatory process; and we just can’t put our hope into something that we expect or hope to come. We have to put our business behind what’s really actually happening, and make smart strategic decisions around what we can actually really truly underwrite to, and that’s really our mentality right now.

Scott Fortune

Okay. Thanks. Appreciate the color.

Nick Kovacevich

Oh, one more thing to comment on that, Scott, actually I forgot, is, I think that the federal reform that everyone’s been waiting for, I think it all comes down to November. I think as long as the Republicans are in the Senate, I do not think we will get anything meaningful done for cannabis. November is a big election, not necessarily for the President, because I think whoever’s in the President’s chair is going to sign a bill. I think it’s all about the Senate. If the Democrats can get control of the House and Senate, we will have legal cannabis coming soon. If that doesn’t happen in November, we’re in for a long four years.

Operator

Thank you. Our next question is coming from Greg Gibas from Northland Securities, your line is now live.

Greg Gibas

Afternoon, guys, thanks for taking my questions, and I appreciate all the info that was in the slide deck, it’s very helpful.

So first, you talked a little bit about aligning yourself with the customers that you’re confident can make their payments on a timely basis. So I guess, to what degree I guess has lack of collections from customers impacted revenue last couple of quarters? When we think about some reduction in contributions from legacy customers, how much of that is simply the customer either going out of business or unable to place an order just due to limited visibility, versus you guys kind of refusing to take their orders or at least extend credit to them?

Nick Kovacevich

Could you repeat the first part of that question?

Greg Gibas

Just to what degree I guess, or if you can quantify, like how lack of collections from customers has impacted revenue recently, maybe last couple quarters or so?

Nick Kovacevich

I’ll give some anecdotal examples and try to quantify. But I mean this is a situation that we deal with, right, all the time. We have a legacy customer in a state like California that’s traditionally purchased a lot through us. They now have an outstanding balance of $300,000 to $400,000; it’s 90, 100, 120 days past due. They’re chipping away, they’re making payments. But guess what else we have? We have $300,000 to $400,000 of inventory with their name on it sitting in our warehouse. So now we’re stuck between a rock and a hard place. They want the inventory, but they can’t pay down their balance. Do we then give them the inventory, then jacking up the receivable? Or do we just sit on the inventory, which is costing us money to store, and try to see if these guys can pay us down? And if they can’t get additional credit from us, what do you think they’re going to do? They’re probably going to call one of our competitors and start going and buying from them, just so that they can get additional lifeline and keep their business going.

This is the game that unfortunately we’ve been dealing with in a lot of these markets; and we’re sick of it, to the point where we have outstanding balances from customers, up to you know in the million seven figure range, where yes they’ve been paying us $25,000 here and $25,000 there, and we’re just done with it. We’re taking all the write offs, we’re doing it all right now, and yes, we’re going to collect some of that in the future, but we just don’t want to deal with it, and we’re not going to be extending credit to these guys any more, and we’re going to be focusing just on folks that can actually pay their bills in a timely fashion and get us the money that we’re deserved for the service and the products that we provide.

So if I had to quantify it, I would say, certainly California, the majority of the revenue that we’re missing there has either been from customers that have ran up too high a balances and have been forced to go find other people that will give them credit, also companies that have been basically hurt in the market and their sales just are nowhere near what they once were, so they’re trying to play catch up and rebound their business. We also have instances where folks have gone out of business. Right? We’ve even been able to secure some collateral in some instances, so we do have things that we can go after, but it’s just really challenging, especially for doing this for hundreds or thousands of accounts. It just becomes time consuming, and we just don’t have the resources and the money, so we need to get to a more streamlined model, and this really does it.

Jason wanted to comment here too, so go ahead.

Jason Vegotsky

Hey Greg, it’s Jason.

The only thing I would add to that, that we’ve seen over the last three or four quarters, is that a year ago it’s not like this wasn’t going on. It was going on, but it was the smallest of the customers in these states, right? What we’ve seen is that this trend has creeped into the industry as a whole. It doesn’t matter how big or small you are, outside of those bigger MSOs that all you folks are covering, the regional player is just struggling. That regional player, it only got exacerbated when the vape crisis and capital crunch hit. This isn’t necessarily a new game for us, but the customer base that’s affected is not just the mom and pop anymore. It’s all the way up to the large regional player.

Greg Gibas

Okay, got it, yes, that’s really helpful, guys.

And then it sounds like order visibility, you’re seeing from customers on the vaping side, the business is improving? Can you maybe elaborate on what you’re seeing differently with respect to vape orders since the last call, and maybe when we would expect the return to vape sales levels to be on par with pre vape crisis demand?

Jason Vegotsky

This is Jason again.

I think a lot of this is due to just buying pattern changes. I mean we had a lot of customers that were out there, trying to get the best price, buying as much as they can when they had the money; and once you saw the vape crisis hit, just buying patterns have changed dramatically. Nobody is out there saying hey I’m just going to load up for an extra $0.05 discount, right. As people are saying I want to conserve my cash, I don’t care how big they are, everybody wants to conserve their cash and buy exactly what they need and have no excess fat on there.

I think a lot of it is buying power, and then, especially in California, right, it starts with the retailers. If the retailers aren’t paying their bills down to the brands, then the brands just aren’t going to be able to have the funds to then go and buy appropriately. So it’s a trickle down effect across the entire supply chain.

Nick Kovacevich

The other dynamic with the delays in the supply chain here recently is folks are waiting on bigger custom orders that they would take a larger chunk. But in the interim, they’re making smaller stock order purchases because they don’t want to run out of vape products, but they really want to wait as long as possible to get their custom order. So the timing on all this, due to all these dynamics, has shifted, and we think, in terms of vape demand, we see the data, it’s coming back at the consumer level, we’re aligned with these core customers, we’re seeing their vape demand be very strong and continuing to grow. The only difference is, we’re not selling vape to a lot of customers that have outstanding balances with us and can’t pay their bills. That’s really the one thing that hasn’t allowed us to get back to those pre vape crisis levels when it comes to our vape sales.

Greg Gibas

Okay, got it. Thanks guys.

Operator

Thank you, our next question is coming from Gordon Johnson from GLJ Research, your line is now live.

Gordon Johnson

Hey guys, thanks for taking the question.