You’re reading this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to help our readers stay ahead of the curve as well as links to the week’s most important news. We no longer send these by email as we did in the past, but we post this and all of the newsletters on our website here.

Friends,

Cannabis stocks are very strong in July, though they have dropped over the past week. So far in July, the NCV Global Cannabis Stock Index has gained 8.2%, which far exceeds the 1% gain in the S&P 500. Of course, the action is very different year-to-date, with the S&P 500 up 7.3% in total return and the cannabis index down 21.1% in price.

Last week, I questioned the big rally in the early days in July, and the Global Cannabis Stock Index has dropped 3.7% since then. Last week, 22 of the 23 stocks in the index were up in July, and now that number is a still-high 19. The number of double-digit percentage gainers has dropped from 7 to 5, and none of those are MSOs. Last week there were two.

Today, I want to look more closely at the MSOs. At 420 Investor, I reduced my exposure in my model portfolio last week and now hold just two names that total 12.4% of the portfolio, which is slightly above the index weight currently of 12.1%. Recall that the index weighting plunged when the index was rebalanced at the end of June, with just three MSOs in the index now: Glass House Brands, Green Thumb Industries and Trulieve. The contrarian in me wants to be longer the sub-sector, but the analyst in me is telling me to be patient!

Owning the MSOs is making a bet on 280E taxation being eliminated. I first wrote in this newsletter about 280E taxation as a big issue in late 2022. It seemed like cannabis was going to be rescheduled, which would have wiped out 280E taxation, but that no longer looks likely. Of course, it could still happen.

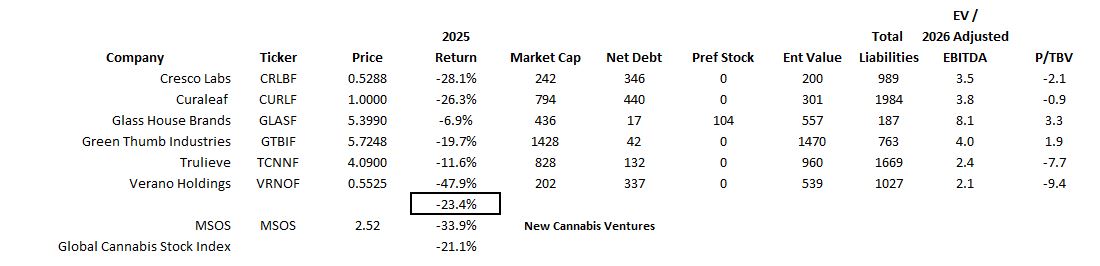

Looking at the Big 5 MSOS, which include Cresco Labs, Curaleaf, GTI, Trulieve and Verano, and Glass House, which is in the index, they seem very cheap. If 280E remains in place, though, there will likely be some financial challenges for several of them. There have been several MSOs that have already experienced financial challenges, and one Tier 2 name, AYR Wellness, faces them currently. That stock is down 67% in 2025.

Here is a table that includes these six stocks that I am focusing on (as well as AdvisorShares Pure US Cannabis ETF (MSOS) for the price performance):

The best balance sheet among the Big 5 MSOs belongs to GTI, but it does trade at a premium to its tangible book value. Investors can find names among the Canadian LPs and the ancillary companies that trade on a higher exchange and that trade below tangible book value despite having no net debt. Glass House Brands, which I not follow closely, trades at a higher ratio, and the rest of these MSOs have negative tangible equity. Note that the liabilities of Curaleaf and Trulieve are multiples of their net debt. Note as well that Glass House Brands, which issued preferred stock yesterday, is the only MSO here that does so.

The cheapest name on an enterprise value to projected adjusted EBITDA basis is Verano Holdings, though most of these stocks do trade at a very low ratio. While I don’t include GLASF on my Focus List at 420 Investor, I did write about it yesterday, saying it appears expensive.

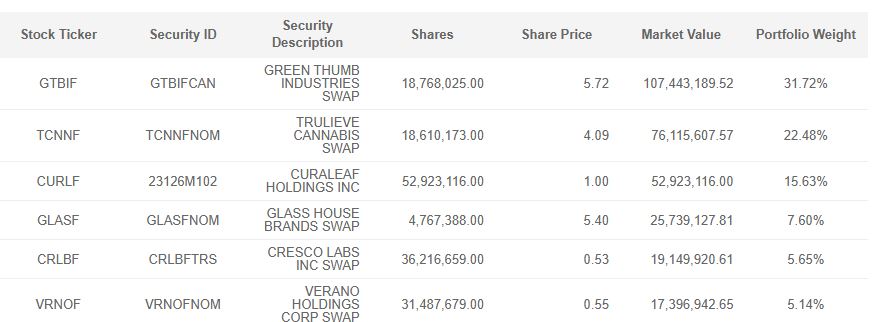

Again, I remain very negative on MSOS. I wrote about it here last in late May, saying that it was at risk, and it has not changed in price since then. The current exposure to the Big 5 totals 80.6%, and its fourth-largest position, GLASF, is 7.6%:

I continue to believe that the very big issue is 280E taxation, but there are other issues, like the pace of legalizations by state, developments in the hemp market and consumer demand for cannabis, that could matter. The big state that could legalize for adult-use is Pennsylvania, but its medical market is already very advanced. I live in Texas, and there is a major improvement in the medical cannabis program that kicks in this year. Overall, though, the state legalization market will not drive big long-term growth. I am a big fan of the hemp market, and three large MSOs are involved, but I don’t see this as a driver of any of those stocks. On demand, the pandemic boosted it, and there has been a pullback, especially in the west, but things seem to be improving. I don’t see demand soaring and driving the MSOs.

There are some other big issues potentially. The biggest would be federal legalization or descheduling, and this may happen. It probably won’t happen soon, and there will be plenty of opportunity to get in, if it does happen. For those who believe legalization or descheduling will take place, the MSOs do seem cheap enough and out of favor enough for it to generate gains. The final issue is M&A, but this does not seem like a big factor for the largest MSOs. Remember Cresco Labs and Cannabist (Columbia Care)? The rules of the states can get in the way, with some limiting the number of retail stores and some limiting the size of the cultivation.

So, I am not very optimistic at this moment on the largest MSOs. I think that there are good opportunities in certain ancillary stocks and in some Canadian LPs. I do wish all cannabis investors the best!

Sincerely,

Alan

New Cannabis Ventures publishes curated articles as well as exclusive news. Here is what we published this past week:

Exclusives

Florida’s Cannabis Market Is Crumbling

Weak Michigan Cannabis Sales in June

Capital Raises

Cronos Group Lends High Tide C$30 Million

Glass House Refinances Preferred Stock

To get real-time updates, like our Facebook page, or follow Alan on Twitter. Share and discover industry news with like-minded people on the largest cannabis investor and entrepreneur group on LinkedIn.

View the Public Cannabis Company Revenue & Income Tracker, which ranks the top revenue producing cannabis stocks.

Stay on top of some of the most important communications from public companies by viewing upcoming cannabis investor calendar.