Cannabis RTOs/IPOs

Guest post by Steven Looi and Michael Miller of Initiative Capital

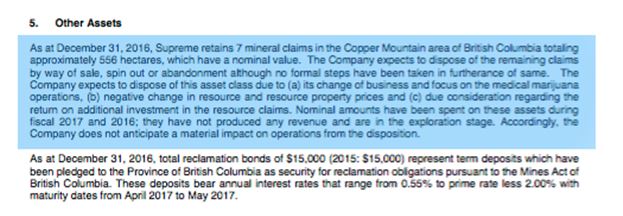

On March 11th, 2016, Ontario based Supreme Pharmaceuticals Inc. (CSE: SL) issued a press release to indicate that they had been granted a federal license to cultivate medical marijuana[1]. If you had considered investing in the wake of this news then went to their most recent financial statements published on February 29th, 2016, you might have been surprised to find that Supreme owned ‘9 mineral claims totaling approximately 607 hectares in… British Columbia[2].’ While Supreme had assigned a book value of $0 to these resource exploration assets, and as of December 31st, 2016 have reduced their number of mineral claims to 7, the question remains, why would a producer of medical marijuana own any mining assets whatsoever? The answer it turns out has nothing to do with CEO’s diversifying their grow operations by looking for gold, and everything to do with the unique nature of Canada’s capital markets.

Headquarters of the Toronto Stock Exchange (TSX) and Canadian Securities Exchange (CSE), the former of which hosts the world’s largest publicly traded cannabis producers including Canopy Growth Corp. (TSX: WEED) and Aphria Inc. (TSX: APH), Toronto can seem like the global centre for legal cannabis financing. (A title Toronto will assume and begin promoting five minutes after this article goes to print.) For most investors though, Toronto is likely better known as the centre of global mining finance with over 1200 listed companies and a whopping 57% of global mining financings executed in 2016 between the TSX and its junior partner, the TSX Venture Exchange (TSXV).[3] While over 200 of these mining companies trade on the “Big Board”, nearly 1,000[4] trade on the TSXV, with many of these companies existing as exploration companies with no plans of generating immediate revenues. Not surprisingly, many of these exploration companies don’t always find something worth digging up and many simply run out of resources to keep looking.

The link between these public mining companies, that have all but ceased operations, and a cannabis producer comes when the producer makes the decision that they want to go public. There are plenty of reasons why a Canadian (or foreign) producer would elect to go public, a key one being the need for new capital to rapidly expand their grow facilities to meet the demand for the burgeoning medical market and incoming adult-use market. This need for capital has brought in over $700 million for both public and private companies in the past six months alone according to Canaccord Genuity,[5] while major industry player Aurora Cannabis Inc. (TSXV: ACB) has brought in $150 million over the past year, of which $75 million came in just this past February[6].

Upon making the decision to go public, the producer must ultimately decide what route they want to take to become listed, and thus far in Canada the most popular route for cannabis producers has been by way of what is known as a reverse take-over (RTO). Readers are likely familiar with the concept of an initial public offering (IPO), where a private company prepares a prospectus and offers their shares to the public concurrent with becoming publicly traded, however, readers may be unfamiliar with the concept of an RTO. In an RTO, an already public company acquires or merges with a private company. The public company issues shares to the private company’s existing shareholders as consideration for the acquisition with the end-result being that the shareholders of the private company become the majority owners of the publicly listed company. A preferred condition of being able to perform an RTO is the identification of an appropriate company that has a public listing, a sufficient shareholder base, and no serious overhanging liabilities from their previous operations. (Often referred to as being “clean.”) Mining companies that have a public listing and haven’t accrued any serious liabilities, be it from environmental degradation necessitating a clean-up or otherwise, have been popular vehicles for RTOs for decades. These transactions have been common across numerous industries, and it was the vehicle through which Aurora Cannabis Inc. went public after it executed an RTO with Prescient Mining Corporation (TSXV: PMC) on December 9th, 2014.[7]

An alternative to executing an RTO through a mining company in Canada is to complete an RTO with what is known as a Capital Pool Company (CPC). CPCs are publicly listed shell companies that don’t have any commercial operations or non-cash assets that exist for the sole purpose of completing an RTO (also known as a qualifying transaction in this case) whereby the CPC will acquire an operating business or assets that can be formed into an operating business. Using a CPC to go public in lieu of a mining shell has been exceptionally popular among cannabis producers primarily because such CPCs typically do not come with any baggage (i.e. they are clean). Emblem Corp. (TSXV: EMC) used the CPC Saber Capital Corp. (TSXV: SAB:H) to perform its RTO on December 7th, 2016[8], which explains why Emblem Corp. has historical financial statements that date back to Saber’s initial public offering on July 4, 2011, years before the completion of the RTO.

Given the need to identify an appropriate entity for an RTO, whether it is a mining company or a CPC, and the risks of inheriting the baggage of another company, why wouldn’t a cannabis producer just perform a conventional IPO? A common misconception has been that the RTO process will be considerably cheaper or faster than an IPO, however, both the costs and timelines are often quite similar. While each licensed producer would have their own motivations, drivers for conducting an RTO as opposed to an IPO can include: the acquisition of a sufficient shareholder base to meet the minimum listing requirements of an exchange, the ability to test the waters with investors by offering a private placement before conducting the RTO as opposed to initiating the IPO process and incurring significant professional fees before determining the market’s sentiment, and, depending on the transaction structure, the ability for holders of the company’s shares (other than insiders), acquired through a private placement in advance of going public to freely trade their shares upon closing, thereby avoiding the four month statutory hold period customarily imposed on such shares.

Dentons Canada LLP partners, Corey MacKinnon and Kris Miks, have advised that “with proper advance planning, RTOs really do offer private companies significantly reduced execution risk. Knowing that the financing is complete, essentially in advance, removes a huge hurdle and a large degree of anxiety for management teams. Management, needs to understand that any going public transaction is enormously distracting to its focus on its core business. Accordingly, any reduction in execution risk makes such distraction much more palatable.”

As cannabis producers continue to list in Canada, investors should not be surprised to see historic names and assets lingering on the company’s financial statements. Cannabis investors should be wary, however, to make sure that the company has not assigned significant values to these assets, are not incurring significant expenses to maintain them, and that there are no off-balance sheet contingencies in the notes of their financial statements indicating that they may be on the hook for a significant payout. That being said, the use of RTOs to obtain listings is not unique to cannabis and is something that some of the most successful publicly traded companies have done. Media and entertainment giant Lions Gate Entertainment Corp. (NYSE: LGF), a producer of the show Mad Men, a distributor for the Hunger Games franchise, and a company with a market capitalization of ~$4 billion USD, first went public after it executed an RTO with Beringer Gold Corp. in 1997[9]. Given their history, RTOs have come to be considered a well-worn and acceptable path for going public by the investment community in Canada, and it is a path that many licensed producers are likely to take in the future.

[1] Supreme Pharmaceuticals Inc. Supreme Obtains MMPR License to Cultivate Medical Marijuana, March 11th, 2016.

[2] Supreme Pharmaceuticals Inc. Management Discussion and Analysis of Financial Results February 29th, 2016.

[3] TMX Group, Mining https://www.tsx.com/listings/listing-with-us/sector-and-product-profiles/mining Accessed March 14th, 2017.

[4] TMX Group, Mining http://www.tmxmoney.com/en/research/mining.html Accessed March 14th, 2017.

[5] Reid Southwick, Canadian cannabis industry raises $700M in six months, report says, Calgary Herald. March 14th, 2017. http://calgaryherald.com/business/local-business/canadian-cannabis-industry-raises-700m-in-six-months-report-says Accessed March 15th, 2017.

[6] Ibid.

[7] Aurora Cannabis Inc. Management Discussion an Analysis February 29th, 2016.

About the authors:

Michael Miller and Steven Looi are founding members of Initiative Capital, a cannabis venture fund based in Toronto, Canada.

Michael is a multi-disciplinary venture capitalist and a regular adviser to early-stage companies looking for guidance on valuation, raising capital, and long-term positioning. A frequent writer on the emerging cannabis industry, Michael’s writings can be found in leading trade and consumer publications.

Prior to co-founding Initiative Capital, Steven was an entrepreneur with international reach having launched and successfully exited from businesses in both China and Canada. With experience founding, operating, and managing software, pharma, and urban agricultural companies, Steven brings a multifaceted approach to the challenges of the cannabis industry. Steven has been a regular fixture at industry events in both Canada and the United States in his capacity as a cannabis angel for emerging companies.