Eight Stakeholders Discuss the Shift to Cannabis 2.0 and How the Industry Will Evolve

The legal cannabis industry has rapidly developed, but it is still a business in its nascent stages. Federal illegality and volatile capital markets create a challenging environment subject to frequent winds of change. Yet, operators are finding ways to compete, thrive and drive the industry forward. The cannabis business may still be very green, but the players responsible for pushing it forward are finding ways to adopt the strategies and business models that have been proven in more established consumer packaged goods industries.

What do the CPG and the much-discussed “Cannabis 2.0” models look like for multi-state operators and cannabis brands today, and what comes next?

Cannabis 1.0

Looking to the past paints a picture of just how far the cannabis industry has come. Cannabis 1.0 existed largely before widespread legalization. Quality control and measurable potency, let alone different form factors, were of little to no consequence. The focus was mainly on access with differentiation in products mostly lumped into two groups: indica or sativa flower.

As state legalization, both medical and adult-use, moved forward in more states, access was no longer the main concern. Regulations set the bar for quality and a suddenly much larger consumer base, some of whom had never used cannabis, meant companies needed to know more about their products, educate their customers, learn what those customers actually want and provide it. Legalization sowed the initial seeds of Cannabis 2.0.

Cannabis 2.0

The term “Cannabis 2.0” is often applied to different form factors. For example, edibles and beverages are classified as 2.0 products. But this more mature stage of the industry is about more than just different types of products. “It’s all about the brand and the flavor and the form factor. It’s less about the substance itself,” says Nick Kovacevich, CEO of Greenlane Holdings.

For cannabis companies, both brands and MSOs, the product itself remains foundational, but branding has become paramount as well. With so many different products available, companies need branding to create differentiation and consumer connection. “What we’re seeing now more than ever in the industry is a focus on consumer insights in the product development and brand-building process,” says Adam Grablick, COO of Kiva Confections.

Cannabis brands are looking for ways to stand out, creating the foundation for what they hope to be will a lasting place in the evolving industry. “What puts a brand at the forefront of cannabis is the people—the community they serve, the team they build and the people who execute the brand vision. Those elements create a brand that can stand the test of time,” says Tori Cole, VP of Marketing at Cookies.

The people of Cannabis 2.0 are increasingly sophisticated, both in the professional and consumer spheres. The booming industry is luring people from more established industries – finance, agriculture, retail, CPG and more – with the promise of using polished skills to build something new.

Cannabis 2.0 has also created a more diverse consumer base. The illegal market remains active, but there are customers accustomed to the illicit market migrating to the legal space. These consumers, as well as others who have in-depth knowledge of cannabis, know what they want. Other consumers are introduced to the market as medical patients, seeking relief for specific symptoms. Still another group is attracted to the idea of health and wellness benefits. Others are labeled “canna-curious,” considering the role recreational cannabis could play in their lives.

Cannabis 2.0 products and brands are not one-size-fits-all. There are different consumer wants and needs that demand different products and brands. “As with any CPG company, our job is simple: to understand the needs of our consumers, then develop products that meet those needs better than our competitors,” says Joseph Bayern, CEO of Curaleaf.

In the current cannabis landscape, retail is a critical consumer touchpoint. Cannabis cannot be shipped over state lines. Ecommerce certainly plays a role within state lines for THC-based products (nationally for some companies with CBD products), but retail is the place people come for consumer education and the in-person experience.

In the early days of legalization, simply opening the doors to a new dispensary was exciting news for consumers. In the more established market, that is hardly the case anymore. With MSOs and regional operators gobbling up licenses as quickly as they can apply for or acquire them, consumers in many states can afford to be picky. “Gone are the days in many markets where you have lines out the door that generate themselves on a day-to-day basis,” says Cory Rothschild, SVP of Brand Marketing at Cresco Labs. “The regular differentiated retail experience that you’d expect in so many other industries is now what we should expect in cannabis.”

Regulatory Constraints

Federal illegality prevents cannabis companies from fully mirroring traditional CPG industries. In today’s environment, interstate commerce is not possible. Marketing is strictly guided by regulations that vary from state to state. Form factors can also be limited depending on a market’s regulations.

The varying patchwork of regulations that spans across the legal cannabis market in the U.S. creates a challenging dynamic. Cannabis companies operating in federally legal markets, like Canada, face their own regulatory challenges as well, not to mention the complexity faced by companies flexing their muscles and taking on operations in multiple countries.

Cannabis companies are striving to adopt the guise of national CPG players while operating on a state-by-state basis. For MSOs, this means establishing individual operations capable of producing products consistent in quality and consumer experience. These companies either must establish vertically integrated operations – and in some states, they are required to do so – or they must find trusted partners to help them expand their footprints. Traditional CPG industries, like alcohol, can simply set up regional hubs to service large swaths of a market, rather than a single state.

Cannabis brands must vie for shelf space in different states, adopting each individual market’s requirements for marketing and packaging, and develop operations or find partners to maintain the now-paramount quality and consistency for their products.

Regulations, while an enduring challenge, have helped to shape Cannabis 2.0 and pave the path forward. Regulation has raised the bar on quality, giving consumers access to safer, more consistent products. “I don’t mean to say that regulation is the enemy of progress towards Cannabis 2.0. What I mean is regulation as executed by states or regulators and lawmakers that don’t fully understand cannabis and Cannabis 2.0.…makes progress in this industry very difficult,” says Joe Hodas, CMO of Wana Brands.

This regulatory landscape makes it difficult to develop a unified presence and brands, but cannabis companies are finding ways to use the CPG playbook in this reality. “Our goal is to make product launches look much like the ones that other large, national, CPG companies typically do,” says Bayern. “In March, we announced the launch of Select Squeeze, a fast-acting THC-infused beverage enhancer, which marked a significant milestone as the cannabis industry’s widest national product launch.”

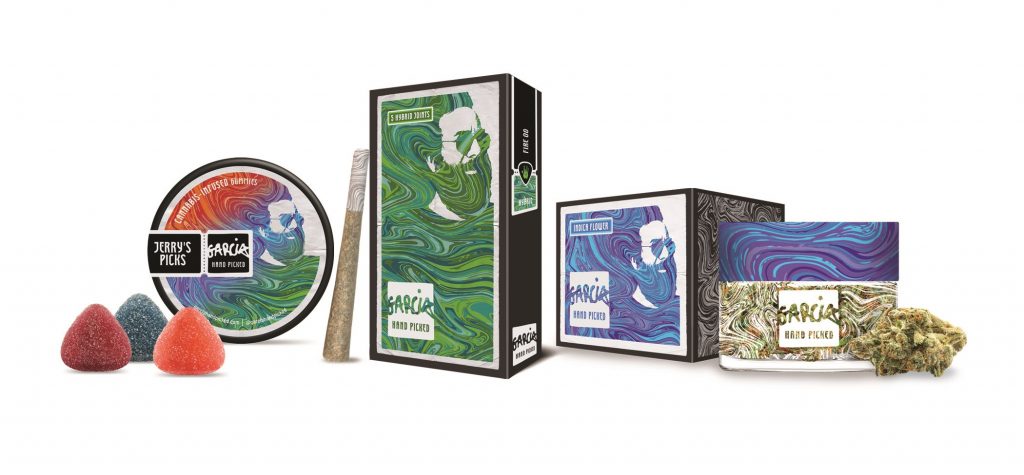

Regulatory constraints around marketing mean cannabis companies have not been able to connect with consumers via all the same channels as other CPG companies. With retail being so important, cannabis companies and brands have been forced to get creative with how they present their products on those shelves. “That lends packaging to be one of the most important parts of getting access to that consumer because they’re going to walk in, they’re going to spot a product on the shelf that they’re going to want to engage with and then the initial part of that experience is going to be in unboxing of that product,” says Nick Kovacevich.

With each state making its own rules, and regularly changing them, cannabis companies are forced to remain flexible. In some ways, that challenge has been a boon for the industry. “Some of the challenges we are up against in cannabis have enabled faster and more profound innovation than we ever could have imagined, and innovation is the key to the evolution of any industry,” says Josh Genderson, CEO of Holistic Industries.

Making Progress

Cannabis 2.0 is not a perfect reflection of the established CPG model, but companies are finding ways to leverage CPG strategies within the current regulatory frameworks and capital environment. “Using traditional CPG frameworks like good-better-best pricing and upper and lower funnel marketing are also ways that the industry (its biggest players at least) are increasingly mirroring approaches found in a CPG model,” says Grablick.

As more and more cannabis companies and brands strive to adopt these kinds of CPG strategies, competition in the industry grows. “When Kiva started in 2010, things like beautiful packaging, consistent dosing, and lab testing set us apart. Today, to stay competitive brands need to think about things like positioning, segmentation, product points-of-difference and the consumer’s evolving need states,” says Grablick.

Consolidation has swept into this competitive environment, with large players extending their footprints and broadening their portfolios by acquiring other operators and brands. M&A is a big theme, but cannabis companies are still faced with the challenge of integration.

M&A is on the radar for plenty of companies, but actually pursuing deals could be tempered by valuations and access to capital. With so much growth within reach, many cannabis companies are feeling the pressure to scale and meet demand. “The biggest issues we see are related to the physical capital required to usher in the next wave and the regulations that make it harder. We desperately need higher output manufacturing equipment, larger trucks, more distribution warehouse square footage and more backroom stock space up and down the supply chain,” says Jake Bullock, co-founder of cannabis beverage brand Cann.

Despite capital market pressure felt across the industry, there are companies that have reached profitability. “When you have a profitable company, [it] can actually put those profits back into [its] own operation to improve it, and it’s an amazing feat. That’s not something we could say about our industry even two years ago,” says Rothschild. “The more that companies can put themselves in a position to actually reinvest, the more we’re going to actually see tactics and outcomes that mirror what we expect from so many other companies.”

While profitability is a sign of progress, it does not mark the journey’s end for companies that achieve it or for the industry as a whole. “While we’ve made progress, we still have work to do as an industry to educate and advocate,” says Bayern. “In other categories like apparel and personal care, people have spent their entire lives using the category and have built brand loyalty. Cannabis brands have a lot more work to do.”

What Comes Next?

If the industry is making progress in its 2.0 stage, what will 3.0 look like? “Cannabis 3.0 doesn’t exist until legalization,” says Hodas. Of course, cannabis companies do not know exactly what the timeline for legalization looks like and what exact form it will take. Legalization comes with the hope of decriminalization, tax relief and a flood of more investment. But, new regulation means new challenges.

In a federally legal environment, companies that have already mastered their CPG strategies in other areas could make their way into the cannabis space. “I think we will see more consolidation and more mainstream companies enter the industry through strategic partnerships and acquisitions,” says Genderson.

The breadth of offerings that seems to characterize Cannabis 2.0 may become narrower in the next stage of growth. “Companies will get more focused and really try to win and own a more limited SKU set and a more limited a product offering within a category versus the kind of breadth today that exists with a lot of the leading operators,” says Kovacevich.

What those more limited SKU sets look like for companies could evolve beyond what is available in the market today. “Today, higher dose products are still king. When cannabis becomes federally legal, you’ll also see micro-dosed products rapidly increase in popularity as new-to-cannabis consumers flood into the market,” says Grablick. The industry’s next stage of maturation may also bring with it more innovation. “You’ve seen more adaptation of traditional form factors into the cannabis market, whereas in the future, you may see more innovation of new factors that are innovated within the cannabis sector,” says Kovacevich.

A shift in federal regulations could also herald a change in how cannabis companies are allowed to market and connect with consumers. “The next progression of cannabis will be a focus on relationships through omnichannel marketing. Brands will develop a more direct and intimate relationship with the consumer, allowing for more control over how much they interact with the brand,” says Cole. “Brands that meet the consumer where they’re at and authentically fulfill their customers’ needs will be on track to become the next Coca-Cola or Procter & Gamble of cannabis.”

The retail stores, too, are likely to change as the industry matures. “As more and more mainstream cannabis products enter the market, we think we will see the cannabis industry’s retail environments look and feel a lot more like grocery and liquor stores,” says Bullock. “Cannabis 3.0 is the convergence of cannabis and the traditional CPG markets into one: for example, buying Cann at a liquor store or a bar, having beer distributors deliver cannabis products and alcohol products using the same trucks, manufacturing lines that run both alcoholic beverages and cannabis beverages.”

Industry stakeholders can imagine the broad strokes of Cannabis 3.0, the new freedoms and challenges that come with federal legality, but for now, they must continue to find ways to adapt CPG strategies that work today and build a bridge to the next stage of the industry, whenever it arrives.

New Cannabis Ventures provides sponsored Investor Dashboards for Greenlane Holdings and Cresco Labs. Learn more about the other thought leaders by visiting the Holistic Industries, Curaleaf, Wana Brands, Kiva, Cookies and Cann websites.