You’re reading a copy of this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to help our readers stay ahead of the curve as well as links to the week’s most important news.

Friends,

The world used to care a lot about Canadian cannabis stocks, and now it seems to care very little. The largest licensed producers are down substantially this year:

Despite the big declines from the largest LPs, the New Cannabis Ventures Canadian Cannabis LP Index is up year-to-date by 5%. Of course, the index has plunged over the past year, falling 51.3%.

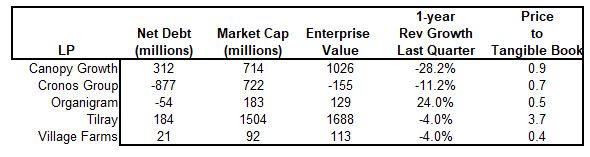

I have shared my negative views on Canopy Growth and Tilray on Seeking Alpha, and we have written in this newsletter about Canopy Growth’s challenges several times. In late March, we discussed alternatives for investors who want to own LPs, including Cronos Group, Organigram and Village Farms. All of these companies trade at substantial discounts to their tangible book value and aren’t burdened by debt. In fact, Cronos Group and Organigram have a lot of cash on their balance sheets.

Canada, which reports its February retail sales on Friday, is seeing a maturation of its cannabis industry, which commenced legal adult-use sales in late 2018. Hifyre is projecting that sales during the short month fell 9.6% sequentially to C$357.4 million, roughly flat on a per-day basis and up 10.3% from a year ago. There are too many producers in the country, and the structure and some of the rules are problematic. In most provinces, the province is the customer of the LPs, which puts the LPs in an awkward position. One of the crazy rules limits THC to 10mg per package. This is not reasonable.

Looking at the landscape, investors seem to have decided that Canopy Growth and Tilray will be winners, but both companies have been losing share and burning cash. Given that their net debt has been growing, the financial positions of both of these companies is risky in our view. Compared to the three companies we prefer, both stand out for trading at higher multiples of tangible book value. This table is done in US dollars:

Note that the revenue growth is for the entire company and not just for cannabis. Tilray has only a minority of its sales coming from cannabis, and Village Farms was at about 50% in its Q4. Similarly, cannabis is not the entire source of revenue for Canopy Growth.

Note that the revenue growth is for the entire company and not just for cannabis. Tilray has only a minority of its sales coming from cannabis, and Village Farms was at about 50% in its Q4. Similarly, cannabis is not the entire source of revenue for Canopy Growth.

We included the enterprise value, which is the market cap plus debt less cash, and the two that we think are expensive, Canopy Growth and Tilray, outweigh the ones we like substantially.

For those investors that own HEXO Corp., it is trading above the price implied by the pending Tilray deal. The stock closed at $1.13 on Friday, which is almost 10% higher than the price of Tilray, $2.37, multiplied by the ratio of .4253, which yields $1.03.

We like some of the Canadian LPs despite the current challenges because they are priced very reasonably, especially in comparison to Canopy Growth and to Tilray. With that said, we believe that there are several alternatives outside of the Canadian LP sector that could make sense too.

Like this newsletter? Sign up, and you will receive a free copy by email each Sunday morning. Each week, we share the top stories and write an original perspective as well.

New Cannabis Ventures publishes curated articles as well as exclusive news. Here is some of the most interesting business content from this week:

Exclusives

Michigan reported very strong cannabis sales in March. Sequentially, the sales lifted by 4.2% on a per-day basis and 15.4% absolutely from February. The record $249.7 million was up 62.9% from a year ago.

Financial Reports

Organigram fiscal Q2 sales rose 24% from a year ago, but they declined 9% sequentially to C$39.5 million. Adjusted EBITDA was $5.6 million, a bit higher than expected. CEO Beena Goldenberg pointed to large format flower pricing as negatively impacting the company’s revenue. The company reported substantial cash and immaterial debt.

Tilray Brands fiscal Q3 cannabis revenue fell by 5% sequentially to C$47.5 million, which was down 14% from a year ago. Overall revenue was below the analyst expectations, and adjusted EBITDA of $14.0 million fell short as well.

Financing

Canopy Growth was able to get Constellation Brands to extend the C$100 million of 4.25% debt it holds through Greenstar Canada Investment Limited Partnership by a year to 12/31/24.

Transactions

Curaleaf closed on the recent acquisition in Utah of Deseret Wellness, paying $20 million to acquire the medical cannabis provider, which operates 3 dispensaries and generates about $14 million of sales annually.

Tilray Brands also announced that it plans to buy the rest of HEXO Corp. that it doesn’t own through the exercise of its warrants for stock (0.4352 shares of Tilray for each HEXO share).

To get real-time updates download our free mobile app for Android or Apple devices, like our Facebook page, or follow Alan on Twitter. Share and discover industry news with like-minded people on the largest cannabis investor and entrepreneur group on LinkedIn.

Use the suite of professionally managed NCV Cannabis Stock Indices to monitor the performance of publicly-traded cannabis companies within the day or over longer time-frames. In addition to the comprehensive Global Cannabis Stock Index, we offer a family of indices to track Canadian licensed producers as well as the American Cannabis Operator Index and the Ancillary Cannabis Index.

View the Public Cannabis Company Revenue & Income Tracker, which ranks the top revenue producing cannabis stocks.

Stay on top of some of the most important communications from public companies by viewing upcoming cannabis investor earnings conference calls.

Discover upcoming new listings with the curated Cannabis Stock IPOs and New Issues Tracker.

Sincerely,

Alan & Joel