On October 22nd at IC3, the 2nd Institutional Capital & Cannabis Conference (East), Adrian Sedlin, CEO of California cannabis company Canndescent, a client of New Cannabis Ventures and a leader in the premium flower category, discussed his list of top 10 myths and facts about the cannabis industry.

1. MYTH: It’s unbanked

In fact, over 400 federally chartered banks offer depository services for cannabis companies. The industry still doesn’t have a full stack of banking services, and federal banking laws are unclear. Larger companies can get depository services, but that’s not the case for most smaller companies. As a result, the larger companies have to deal with hundreds of accounts that are using cash only.

Investors should beware of fintech “solutions” like blockchain payment systems. These reflect a thesis that will go away when cannabis is rescheduled and the major banks begin serving the industry. There is more promise in financial service plays that address another issue: the lack of true growth capital available to cannabis companies. Although many US companies are going public on Canadian stock exchanges, the large pools of private equity that traditionally play a role in company growth ($25-100 million equity investments) still don’t exist, and that problem has not been solved by the industry.

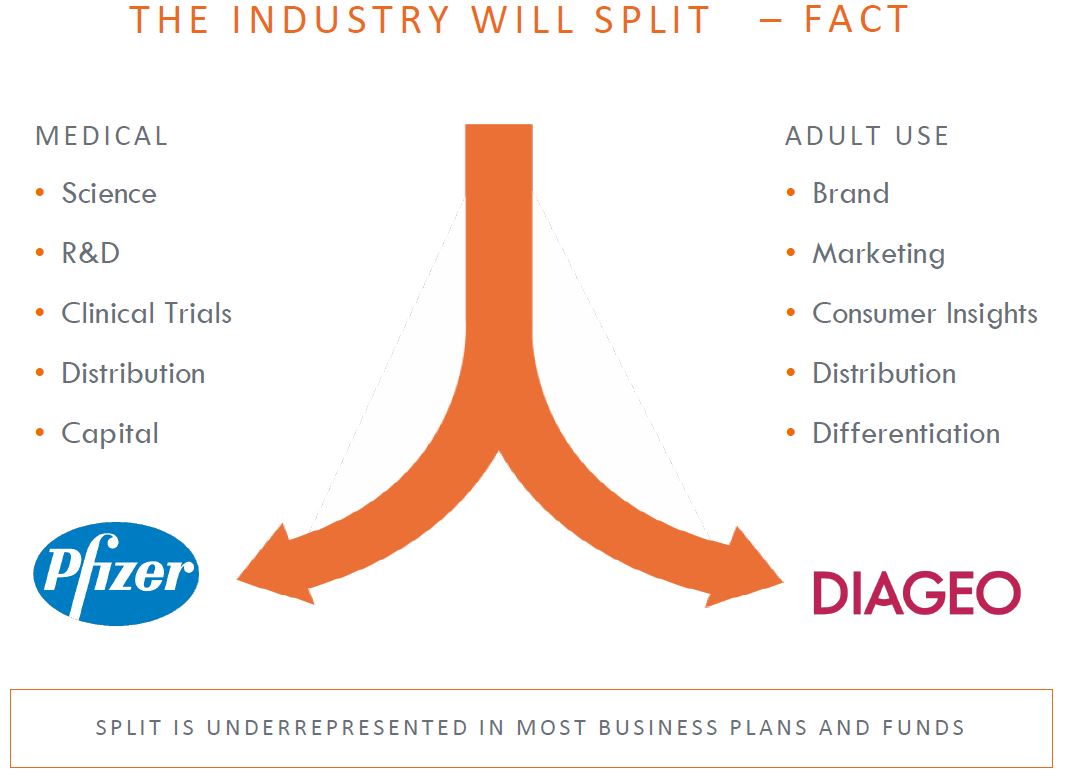

2. FACT: The industry will split

The industry has two streams — adult use and medical — and they will split very quickly over the next 15 years. Historically, the lines have been blurred. In the mid-1990s, when California legalized medical cannabis through a collective not-for-profit system, the state did not put in place a regulatory framework to govern medical use. Recreational users obtained prescription cards, and the two industries came together. Now, as individual states regulate more effectively, the industry is separating. The adult-use side, comparable to the liquor and tobacco industries, is based on customer insights, consumer segmentation, brands and marketing. The medical side, like pharmacy and biotech, is based on science, R&D, distribution and clinical trials. At this time, many so-called medical companies are still really consumer marketing companies. Investors should make sure that the company they invest in has a clear world view and a long-term (10- to 15-year) strategy.

3. FACT: Top US operators like Schedule 1

Schedule 1 is the highest drug schedule of the DEA and categorizes cannabis with LSD and heroin. For now, top US operators still like this restriction, because it offers a perfect window of opportunity. Large public companies face too much headline risk to get involved in the US. On the other hand, the activists who led the industry through its initial stages don’t have the skills to grow companies. This creates an opportunity for well-formed teams with a strong thesis and the right investors to enter the space, build barriers to entry, gain competitive advantage, and create cash flow.

By the end of 2019, most of the top operators will be ready to have cannabis taken off Schedule 1. While the situation has created a great opportunity domestically, it’s putting US companies at a material disadvantage compared to some of the Canadian operators.

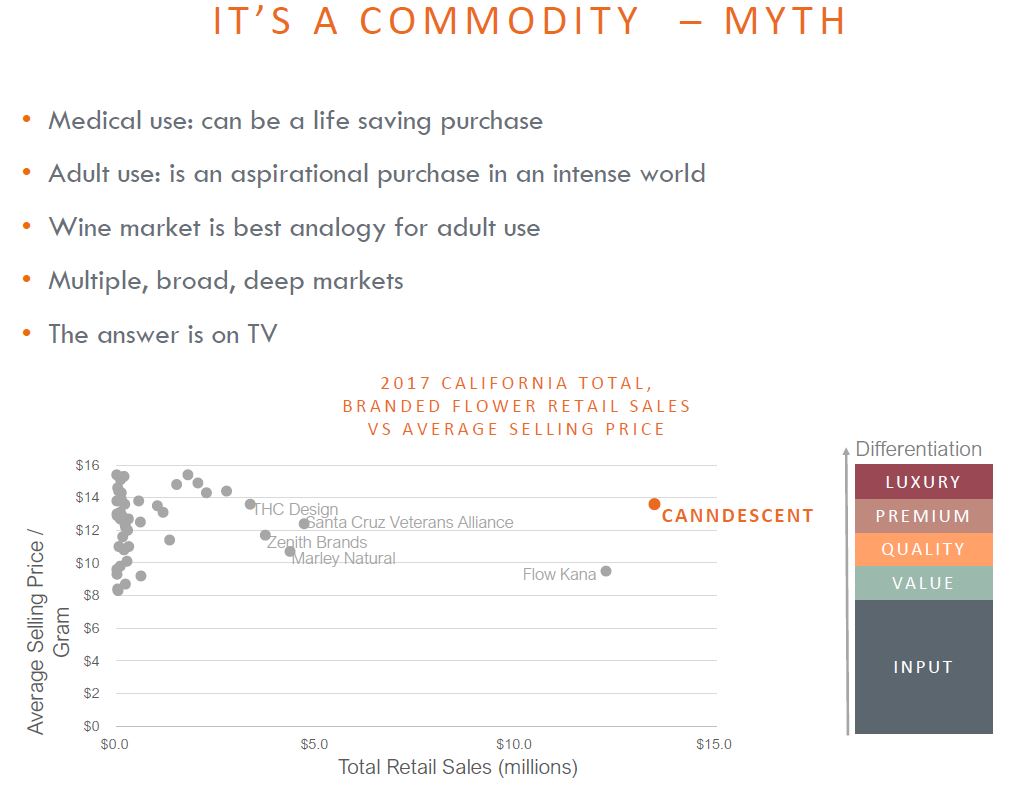

4. MYTH: Cannabis is a commodity

While there is a commodity segment to the industry, cannabis is a consumer good, and there will be multiple broad, deep markets over time. Medically, cannabis treats over 60 known conditions. When people have a medical concern, their first thought isn’t how to save money. On the adult use side, cannabis is an aspirational purchase — a product that is superior to alcohol and can easily be built into a strong, attractive selection of brands. The best analogy is the wine market: there are many different players, from budget to high-end. The successful businesses will know who their customers are and how to align with them. Thirty years from now, there will be massive segmentation, with room for luxury goods and products targeting specific population groups.

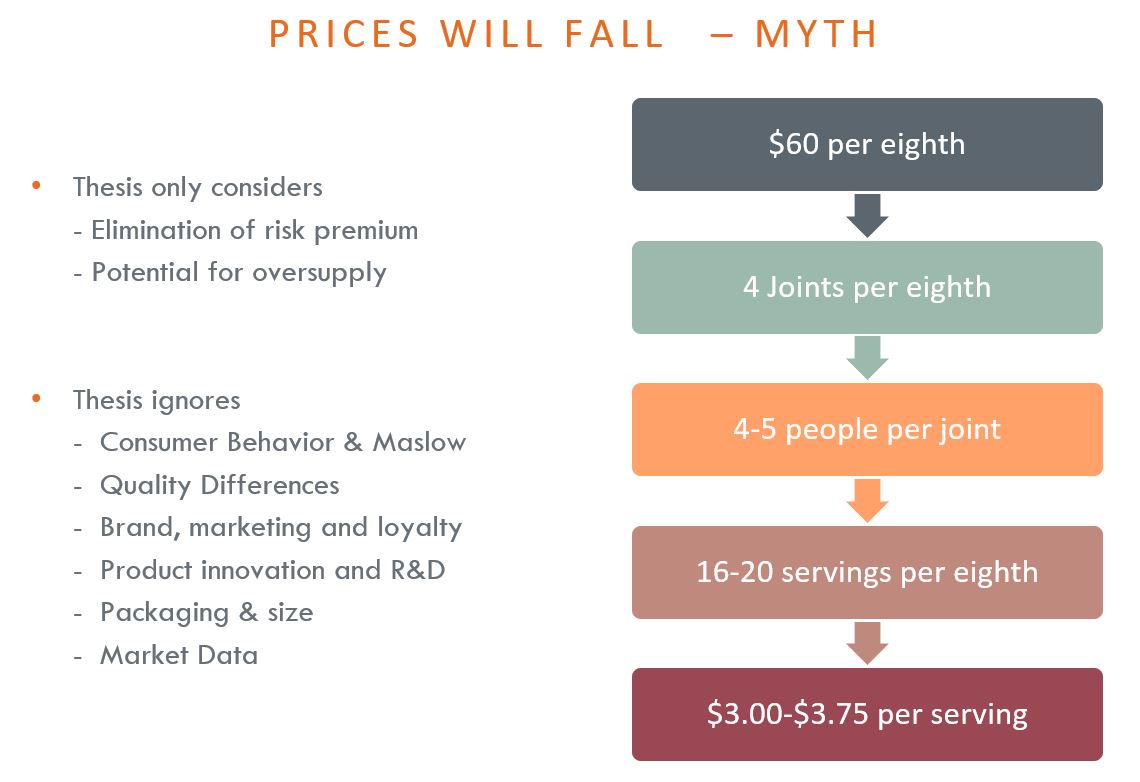

5. MYTH: Prices will fall

The cannabis industry is not a green rush — it’s a green marathon, a long-term secular trend. The “prices will fall” thesis really only considers the supply curve. At first, as supply increases, there will be a momentary oversupply and decline in prices, but that won’t last over the long term. In a post-industrial society, most consumers have their basic needs met and have enough money to pay a premium for a branded, aspirational product. Canndescent products provide a world-class psychoactive experience for $3-4 a serving — and that’s a premium price. When compared to the cost of a coffee or a movie, it’s easy to see the place for this type of product at that price point. Other factors to consider are the quality differences among products and all the R&D that will occur in the industry. So, while prices may fall at some point, they won’t be lower in the long term for the successful brands.

6. FACT: The opportunity is undervalued

Cannabis is a radically undervalued opportunity. It’s a zero-calorie neuro-activator known to help with 60 conditions, and linked to improved sexual relations. In contrast, alcohol is a high-calorie neuro-inhibitor that is linked to 12 serious diseases, intimate partner violence, and incidence of rape. Fewer millennials see getting high as unhealthy, compared to drinking alcohol. Meanwhile, global sales for the alcohol industry in 2017 were roughly $1.6 trillion, and the market capitalization of the top 10 companies in the alcohol industry is close to the same number. The top 10 cannabis companies had a $48 billion market capitalization in 2017 and sales in the global regulated market were $14 billion.

Cannabis also offers multiple form factors, giving it further advantages over the alcohol industry. Alcohol companies that seek to create cannabis-infused beverages are not understanding all the ways that cannabis can be consumed or the full value of the opportunity.

7. MYTH: A rising tide raises ships

This is an undervalued industry with radically overvalued stocks — an asset bubble. People see the opportunity but there are not many ways to play it, so the limited supply of stocks are trading at 100 times current revenues, and future projections are excessive. This bubble that can be traced back to the first Constellation investment in Canopy Growth, with asset bubbles like this tending to last about 5-6 years. The category will remain, but there are multiple innings as it evolves.

The key to survival is to invest in companies that have a strong point of view and solve a real problem. Companies that simply state what they do (cultivation, seed to sale, extraction) are saying the equivalent of “I run a restaurant.” The business plan must be specific and address a real consumer problem.

8. MYTH: Current leaders will win

Although the answer is not simple, in general this is a myth. In this green marathon, investors should look for “fast followers” with a very strong and well-developed understanding of who they are trying to serve and how. Apple is a good example of a fast follower in most of its product categories.

Current leaders won’t win just by strength of market capitalization. Most of the public cannabis companies went public before they were ready, and are splintering their focus, trying to be all things to all people too quickly. It’s better to retain focus and build core strength in a business. Don’t presume the early leaders will win.

9. MYTH: We’ll build the brand later

9. MYTH: We’ll build the brand later

It’s not possible for branding to be an after-thought. Many companies are loading up on assets and becoming multi-state operators, creating superficial brands after the fact. That’s not an investable thesis. Great brands are built from the inside out, with every aspect of the business aligned. Even the investors should share the company’s thesis. Trying to build this focus across multiple assets and regulatory markets is not sustainable. As the industry segments and specializes, companies will have to be best in class, not just first.

10. FACT: Brand from the inside out

10. FACT: Brand from the inside out

Canndescent created a brand by identifying a problem to solve. The company saw an industry with mediocre flower quality, where the retail experience was confusing and intimidating. Customers needed to be weed scientists to make a basic cannabis purchase, and the environment and packaging were counter-cultural rather than aspirational. Eighty-six per cent of products were testing positive for pesticides, and consumers had no recourse. Canndescent focuses on solving these problems.

Great companies will brand from the inside out, have a strong point of view and create lasting, sustainable competitive advantage by relentlessly interpreting the same idea over and over, just as Apple has done with its focus on humanizing technology. Companies that align with the audiences they are trying to serve will be the winners in this green marathon and have a place in what will eventually be a trillion dollar industry.

Listen to the entire presentation:

Download Slides

Are you a cannabis industry thought leader and want to be heard? Let us know your story.