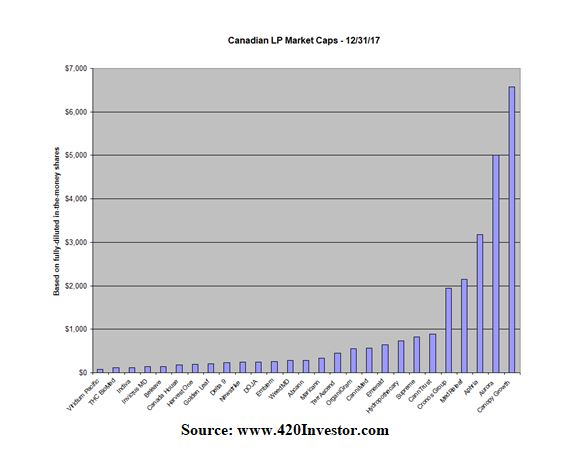

Health Canada has issued 84 licenses to date under Authorized Licensed Producers of Cannabis for Medical Purposes (ACMPR) and has indicated that it will ramp up to over 200 in the next few months. 27 companies, some with multiple licenses but most with one, now trade publicly and have, according to my calculations, a combined market cap in excess of C$26 billion.

These market caps are based upon outstanding shares as well as in-the-money dilutive securities, including convertible notes, options and warrants. The average market cap is C$983mm, while the median is C$287mm, with 5 companies valued in excess of C$1.9 billion, including Canopy Growth (TSX: WEED) (OTC: TWMJF), Aurora Cannabis (TSX: ACB) (OTC: ACBFF), Aphria (TSX: APH) (OTC: APHQF), MedReleaf (TSX: LEAF) (OTC: MEDFF) and Cronos Group (TSXV: MJN) (OTC: PRMCF).

Breaking down the remaining 22 companies, another 5 have market caps between C$500 million and C$900 million, with the remaining 12 between C$71mm and C$452mm. There will be more publicly-traded licensed producers (LPs) in early 2018, and several companies already trade publicly that are likely to become LPs. Six public companies are now producing annual sales at a rate in excess of $C20mm, including Canopy Growth, MedReleaf, Aurora Cannabis, CannTrust (CSE: TRST) (OTC: CNTTF), Aphria and CanniMed Therapeutics (TSX: CMED) (OTC: CMMDF), as we report on our revenue tracker.

Most of the LPs that were licensed before 2016 already trade publicly, but there are several who don’t, including Broken Coast, Canna Farms, RedeCan, Tilray and Whistler, all of which were licensed in 2014. Only Tilray is currently possibly producing at what one might be considered large-scale, but it is privately held as part of Privateer Holdings and hasn’t publicly disclosed its revenue. So, with the possible exception of Tilray, it’s unlikely that any of the older private LPs will be among the top six in terms of market cap were they to go public.

2018 is likely to be a year that Canada sees consolidation among the LPs, public and private, and late-stage applicants. Those that have achieved scale have tremendous market caps and can use their stock to accomplish several goals, including acquiring additional capacity that will potentially lead to quicker revenue than a new project and also financially-driven deals that will help justify the large market caps. Another emerging point that has been highlighted by Aphria’s strategic change revealed in its to recent massive capital raises. The company had previously suggested that its Ontario facilities would be its sole mode of production, but the move towards legalization has resulted in the need to potentially have physical production within provinces in which one wants to sell. Demand from international medical markets opening up could also lead to consolidation. The Aurora purchase of Quebec-based Peloton, then only an applicant but now an LP known as Aurora Vie, which will export to Europe, is a good example. Finally, some in the middle may join together or use M&A to keep pace with the early leaders.

Thus far, the sector hasn’t seen substantial consolidation. To date, Canopy Growth has been a the biggest consolidator, acquiring Bedrocan Cannabis and Mettrum as publicly-traded companies but also several late-stage applicants that it helped cross the finish line. Aurora has also acquired late-stage applicants, and it recently launched a hostile bid for CanniMed Therapeutics, which in turn is bidding for Newstrike (TSXV: HIP) (OTC: NWKRF).

In a webinar New Cannabis Ventures conducted with Canopy Growth CEO Bruce Linton in early November, he discussed consolidation at about 24 minutes in. He doesn’t anticipate another deal like Constellation’s for at least another year, and he sees the sector consolidating, though doesn’t expect Canopy play a significant role going forward. Canopy would be “satisfied with a 40% market share” and didn’t see the value of the assets for sale, which he said were numerous, matching valuations (and this is before the huge rally over the last two months). Linton explained to me in a recent conversation that he expects the big to get bigger and the middle to struggle.

At the New West Summit in October, about a month ahead of the CanniMed bid, Aurora Cannabis EVP Cam Battley addressed the topic head-on, suggesting at 33:30 into the presentation that large LPs were approaching the company to be acquired. He pointed to the need to acquire more product to feed its aggressive growth strategy and how the company regularly reviews acquisitions vs. new construction. Intellectual property on the medical side is something Aurora would seek to acquire as well.

In mid-November, after Constellation Brands (NYSE: STZ) had announced a C$245mm investment into Canopy Growth for roughly a 10% stake with a warrant to take it to 19.9%) and Aurora Cannabis had announced its bid to acquire CanniMed Therapeutics, I interviewed Michael Gorenstein, CEO of The Cronos Group to gain his. perspectives on these deals and the implications for the industry. Gorenstein expects Aurora Cannabis to pursue another acquisition if CanniMed rebuffs its hostile bid successfully. As far as consolidation ahead in the sector beyond Aurora, he expects to potentially see “mergers of equals” and thinks that underperforming stock prices could lead to M&A interest.

I also interviewed John Fowler, CEO of The Supreme Cannabis Company (TSXV: FIRE) (OTC: SPRWF), who sees the potential for more companies from outside the cannabis industry to make investments, similar to Constellation’s deal. He also sees the way the industry is moving towards more differentiation as increasing the likelihood of M&A. Supreme hasn’t yet done acquisitions, but it is looking to add brands, downstream products and oils.

An interesting but not widely discussed transaction that could portend how certain LPs may evolve is the recapitalization of TerrAscend, in which Canopy Growth, its partially owned subsidiary Canopy Rivers and Jason Wild’s JW Asset Management bought just over half of the company for C$52.5 million. I spoke with Canopy Growth CEO Linton last week about the backstory, and apparently Wild was contemplating forming a new LP with Canopy’s backing. The investment into TerrAscend was a great fit and a way to jumpstart the effort. The TerrAscend deal was an anomaly, as the company had an exceptionally low market cap that allowed the deal to take place, but should certain LPs with strong, underappreciated assets fall in valuation, this type of transaction could take place again.

Valuations across the sector seem very expensive, especially after the two-month rally that ensued following the Constellation Brands investment into Canopy Growth. Among the largest LPs and based on my calculation of market caps that incorporate dilutive, in-the-money securities, the six LPs with the highest current sales have price-to-sales ratios based on analyst consensus forecasts for 2019, the first full year of legalization, ranging from 5.6X to 16.7X, and these sales forecasts could be overly optimistic given all the uncertainty.

Looking at valuation from a different perspective, I have compared the market caps to the tangible book value (adjusted for the conversion of convertible notes or the exercise of warrants and options, including the cash received). By this metric, only four LPs trade below 3X. On the other hand, four trade in excess of 10X, with an average for the sector of about 7X. Said very simply, the LPs trade at a huge premium to the value of their assets. Given that none of the LPs is particularly profitable at this point and most are far from it, this metric points to significant risk to prices if legalization doesn’t take place in the expected time-frame or if any companies fail to scale production as rapidly as expected.

With valuations high, most deals will have to be like the Aurora/CanniMed and CanniMed/Newstrike proposed deals, with stock as the sole component, similar to the Canopy/Mettrum deal a year ago. Looking at only financial and valuation metrics could lead to overlooking possible acquisition candidates, as larger LPs may be looking at characteristics like new geographies, brands, technologies and capabilities. Another wildcard could be international exposure.

The bottom-line

While to date there has been little M&A activity, the Canadian LP sector is likely to see consolidation in 2018. The types of deals most likely to occur will likely be the very large companies acquiring LPs with special attributes or relatively low valuations, but one of the big drivers may be companies in the middle that want to combine to achieve better scale in order to compete with the more established LPs. With absolute valuations high, investors should expect stock-based transactions.