You’re reading a copy of this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to help our readers stay ahead of the curve as well as links to the week’s most important news.

Friends,

Although things appear to be heating up again for American cannabis stocks as of Friday’s close, large Canadian LPs didn’t benefit from the exclusive news reported by Marijuana Moment about a Republican-led bill to legalize cannabis.

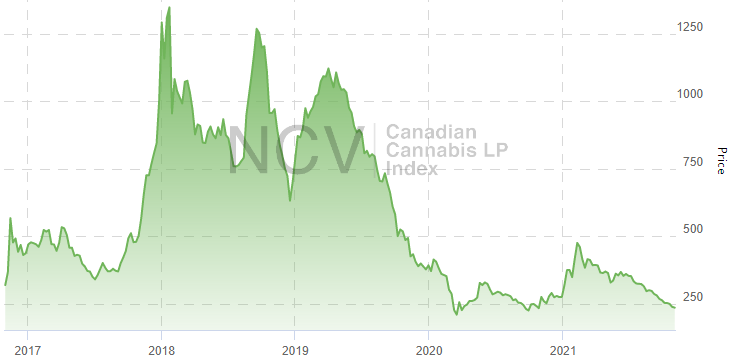

It’s been a very tough year for the Canadian LPs, and the earnings report from Canopy Growth on Friday certainly reinforced the notion that the Canadian market remains challenging for its largest players. While the overall market has advanced 57% year-to-date through September, most of the publicly traded LPs have struggled with market share losses. Excluding acquisitions, the largest LPs have seen their adult-use cannabis sales decline recently compared to a year ago. Through Friday, the New Cannabis Ventures Canadian Cannabis LP Index has declined 14% so far in 2021. It closed just 20% above the multi-year low set in March 2020 and is down from five years ago:

With sentiment perhaps as low as it can be, we think a big M&A deal could be in the works, with Altria potentially buying the remaining shares outstanding of Cronos Group. This is an idea we have been discussing with subscribers at our 420 Investor premium service for several months now, and we think it makes a great deal of sense. Predicting the timing of such a transaction, though, is always a challenge. Before we explain why we think this could happen next week, we will discuss the history and detail our rationale for the deal.

History

It was almost three years ago that Altria announced its strategic investment into Cronos Group: Altria Buys 45% of Cronos Group for C$2.4 billion with Option to Take Controlling Stake

The deal, which closed in March of 2019, infused the company with approximately US$1.8 billion, with Altria paying C$16.25 (about US$12), a price that was characterized as a 41.5% premium to the 10-day volume-weighted average price as of November 30, 2018. Altria also acquired warrants at C$19 that would give it majority ownership if exercised. Additionally, it took control of the Board of Directors. Altria made Cronos Group its exclusive partner for pursuing cannabis opportunities globally.

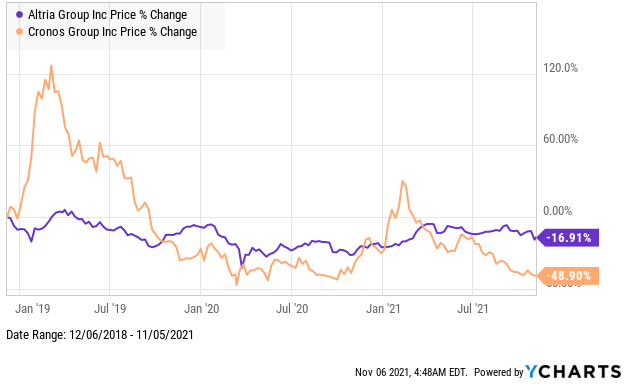

Since the deal has closed, the companies have seemingly worked very well together, though both have seen their shares decline since the announcement:

The warrants that Altria holds are now out of the money, as Cronos Group is trading at 65% below the C$19 exercise price, and they expire in just 16 months.

The warrants that Altria holds are now out of the money, as Cronos Group is trading at 65% below the C$19 exercise price, and they expire in just 16 months.

Why the Deal Makes Sense

We believe that Cronos Group is a good strategic fit for Altria, which continues to look beyond tobacco for growth. With a quarter remaining in 2021, Altria is expected to generate revenue of $21.6 billion, up just 4% from a year ago. Analysts currently forecast little or no top-line growth for the next several years. Over the past 5 years, it has seen revenue increase just 12%, though earnings growth has been a bit higher (9% compound annualized growth over 5 years).

Cronos Group has followed a different path than most of its peers, pursuing an “asset-light” strategy. As of Q2, its entire investment in fixed assets was $193 million, and its inventory was less than $36 million. The company didn’t overbuild for the Canadian market. Its cash balance was $1.1 billion at mid-year, with no debt whatsoever. Cronos Group has pursued an investment into cannabinoids produced by yeast fermentation and has been focused on markets outside of Canada, particularly Israel and the U.S., where it has CBD operations as well as a recent investment in an option to acquire a minority stake in MSO PharmaCann. It has also pursued investment into consumption device research.

Altria has a market cap of $83 billion. Adding in net debt, the enterprise value is $108 billion. Cronos Group is quite small relative to Altria, with a market cap of $2 billion (less than 3% of Altria) and an enterprise value of $900 million roughly (less than 1% of Altria). Our point is that even paying a 75% premium for the equity of Cronos Group ($9.25) would cost the company $2.5 billion net of cash or less than 3% of its enterprise value. This is less than a single quarter of operating income for the company. The financial impact on its own P&L and balance sheet would be minimal. Since the company owns 156.6 million shares (42%) already, the actual cost to acquire the remainder of the company would be substantially lower. In fact, the $2 billion required to buy the remaining shares of Cronos at $9.25 would be $2 billion, which is less than the cash balance at Altria as of 9/30. Of course, a deal could be at a different price and could be stock-based rather than in cash. Our point is that this is rather insignificant financially to Altria.

Because Altria owns less than half of Cronos Group, it doesn’t consolidate the results in its financials. Instead, the financials reflect only the changes in the carrying value of the investment. The fact that Altria’s investment has deteriorated is already reflected in its financials.

With the stock price low, especially in light of a still tremendous cash balance relative to the market cap, buying Cronos is less about near-term financial benefits for Altria than doubling down on its strategic vision. The companies have worked closely now for almost three years, and we believe that Cronos Group is likely much more limited than the combined company would be in pursuing more deals like the PharmaCann transaction. Altria’s larger size will allow a more aggressive investment into the American cannabis industry over the next few years. The original plan to acquire control of the company by exercising warrants is now at risk with the warrants way underwater and running out of time. Altria would be prudent, in our view, to rethink its position and buy the balance of Cronos Group now.

A Potential Clue on the Timing

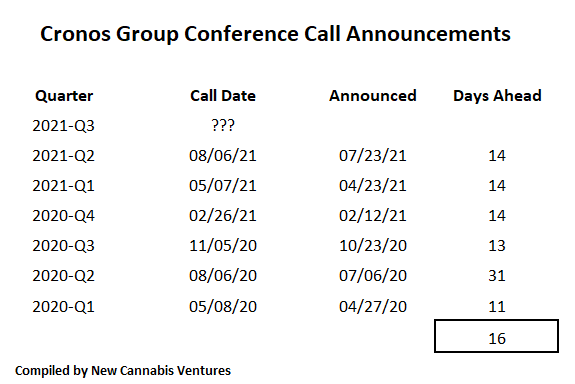

Cronos Group is a large accelerated filer with the SEC, which means its Q3 financials are due on Tuesday, November 9th. Historically, the company has provided investors with at least a week’s advance notice of its conference call, but there has been no call announced yet.

We believe it’s possible that that the lack of notification is because a deal is brewing. To be clear, this is just our speculation, but we can’t come up with any other reason for not announcing a conference call thus far except that it might have a pending acquisition of its own.

What If We Are Wrong

We know we are going out on a limb here with a very speculative call and recognize that we could be wrong about the reason for no conference call announcement. With that said, we don’t see substantial downside in the stock if our hunch proves to be incorrect. The good news is that our view doesn’t appear to be priced in at all, with Cronos Group printing a 52-week low on Friday.

While we may be missing some nefarious reason for the lack of announcement, we believe that investors are likely to receive a relatively good report from the company. To date, the cannabis sales have been modest, but data from Hifyre showed very strong sales during Q3 at the retail stores, with sequential growth of 48% far outpacing the market growth of 9% during the quarter. This is in stark contrast to drastic loss of share at its larger peers like Aurora, Canopy Growth and Tilray. According to Sentieo, analysts are expecting revenue to reach a record $19 million in Q3, representing 67% growth from a year ago.

Cronos Group’s valuation is quite low in our view relative to other large Canadian LPs. The stock trades at just 1.4X tangible book value. Unlike its peers, it isn’t burdened with a high level of inventory or excess production capacity. In fact, its cash balance is more than half of its tangible book value. Further, unlike its peers, the company has no debt. Similar to peers, the company is burning cash, but with its stronger balance sheet and improving market share, this should diminish over the next few years, especially if its biosynthesis efforts pay off.

Sector Implications

If we are correct about Altria acquiring Cronos Group, we believe that it could provide an immediate boost to sentiment for the entire sector. Three other Canadian LPs that have strategic partnerships could see short-term gains: Auxly (Imperial Brands), Canopy Growth (Constellation) and Organigram (BATS). In all cases, we think it would be very premature to assume any sort of deal in the near-term, especially for Canopy Growth, which has a relatively high market cap compared to Constellation (12%) and particularly challenging near-term financial results that we think preclude acquisition at this time. We would not be surprised if other Canadian LPs were to benefit from speculation of new strategic investment partners, but we believe the real beneficiary would likely be American companies. If Altria buys Cronos, we believe it could accelerate the company’s efforts to make legally compliant investments into the American cannabis industry and inspire others to potentially do so as well. We believe that the larger company could also potentially acquire distressed assets in Canada as well as pursue opportunities globally.

Like this content?

Join 420 Investor for more thought-provoking ideas.

Get the facts and be ready for important catalysts with a subscription to Alan Brochstein’s 420 Investor, the longest running cannabis stock due diligence platform trusted by investors for over 8 years. The primary goal of 420 Investor is to provide professional, real-time, objective information about the top cannabis companies in the market in order to help investors Capitalize on Cannabis™.

New Cannabis Ventures publishes curated articles as well as exclusive news. Here is some of the most interesting business content from this week:

- Exclusive: American Cannabis Sales Weakened Further in September According to BDSA

- Exclusive: Ancillary Cannabis Stocks Drop 8% in October

- Cannabis Equipment Finance Company XS Financial Raises $43.5 Million

- Canopy Growth Q2 Revenue Falls 3% to C$131 Million on Wider Adjusted EBITDA Loss

- Colombian Cannabis Producer Flora Growth to Buy Consumption Accessory Company for $30 Million

- Exclusive: Drizly Spinoff Lantern Has $40M in Funding and Plans to Light the Way for Cannabis Ecommerce

- Goodness Growth to Sell Phoenix Dispensary to Copperstate Farms for $15 Million

- Exclusive: Illinois Adult-Use Cannabis Sales Increase 64% in October to $123 Million

- Innovative Industrial Properties Q3 Revenue Increases 57% to $54 Million

- Exclusive: October Decline Leaves Global Cannabis Stock Index Down 7.5% in 2021

- Exclusive: Restructured and Recapitalized Retailer MedMen Looks to Leave Legacy Issues Behind

- Scotts Miracle-Gro Hawthorne Sales Fall 2% in Q4 to $329 Million

To get real-time updates download our free mobile app for Android or Apple devices, like our Facebook page, or follow Alan on Twitter. Share and discover industry news with like-minded people on the largest cannabis investor and entrepreneur group on LinkedIn.

Get ahead of the crowd! If you are a cannabis investor and find value in our Sunday newsletters, subscribe to 420 Investor, Alan’s comprehensive stock due diligence platform since 2013. Gain immediate access to real-time and in-depth information and market intelligence about the publicly traded cannabis sector, including daily videos, weekly chats, model portfolios, a community forum and much more.

Use the suite of professionally managed NCV Cannabis Stock Indices to monitor the performance of publicly-traded cannabis companies within the day or over longer time-frames. In addition to the comprehensive Global Cannabis Stock Index, we offer a family of indices to track Canadian licensed producers as well as the American Cannabis Operator Index and the Ancillary Cannabis Index.

View the Public Cannabis Company Revenue & Income Tracker, which ranks the top revenue producing cannabis stocks.

Stay on top of some of the most important communications from public companies by viewing upcoming cannabis investor earnings conference calls.

Discover upcoming new listings with the curated Cannabis Stock IPOs and New Issues Tracker.

Sincerely,

Alan & Joel