You’re reading a copy of this week’s edition of the New Cannabis Ventures weekly newsletter, which we have been publishing since October 2015. The newsletter includes unique insight to help our readers stay ahead of the curve as well as links to the week’s most important news.

Friends,

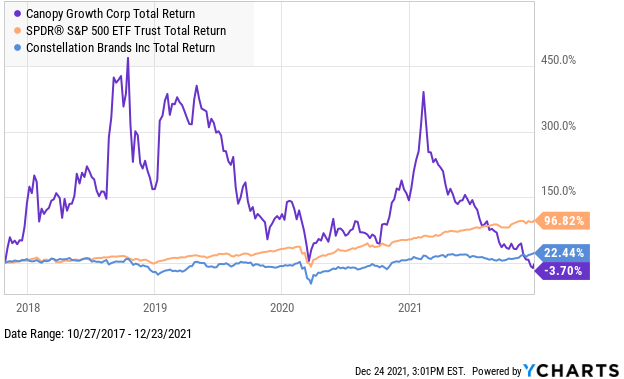

This week, Canopy Growth traded at the lowest price since 2017, as two analysts slashed their price targets into the single digits. In fact, as of the close on Thursday, Canopy Growth has now declined 4% since October 27, 2017, the day before Constellation announced its first investment in the company:

We aren’t going to weigh in today on the investment merits of Canopy Growth, but we did share our view last week, for those who might be interested. Instead, we will review the history of the Canopy Growth strategic investment and discuss what might happen over the next two years ahead of the expiration of the warrants that Constellation holds in the company.

Constellation Jumps In

While four years doesn’t seem like a long time, the cannabis industry was quite different when Constellation made its first investment in late 2017 after almost a year of preliminary discussions. Back then, the company traded on the TSX in Canada but hadn’t yet begun trading on NYSE (later the NASDAQ). In its fiscal Q1 ending in June 2017, which was reported in August, it had generated revenue of just C$15.9 million, exclusively from the Canadian medical cannabis market, as adult-use didn’t launch until late 2018.

Constellation has made three equity investments into the company and also holds C$200 million of the company’s convertible debt. The initial investment of C$245 million bought 9.9% of the company and came with warrants. The price at the time was C$12.98 (18.88 million shares) and included an equal number of warrants at the same price that were to expire 30 months after closing.

Less than a year later, Constellation announced its second investment of C$5 billion at C$48.60 per share for 104.5 million shares in August 2018, just ahead of adult-use legalization. This investment came with warrants as well that were subsequently amended.

The third investment came in May 2020, when Constellation exercised the warrants it had received from its first investment just ahead of their expiration, paying C$245 million to acquire 18.88 million shares at C$12.98. The stock was trading then near C$22. With that investment, the company then owned 142.25 million shares at an average cost of C$38.59, for a total investment of C$5.49 billion. The 142.25 million shares represent 36% of the outstanding shares of Canopy Growth, and the remaining 139.7 million warrants, now well out of the money, would give Constellation a majority of the company upon exercise.

Frustration Sets In

When Constellation made its second investment in late 2018, it took control of the Board of Directors. In May 2019, Canopy replaced its CFO with Mike Lee, a Constellation veteran. The first sign of trouble at Canopy Growth was the sudden departure of former co-CEO and co-founder Bruce Linton just six weeks later. Another Constellation veteran, David Klein, who had begun serving as a director when the second investment closed in November 2018 and as Chairman in October 2019, became CEO in January 2020.

In October, when Constellation reported its fiscal Q2, its investor presentation painted a rosy picture of its investment in Canopy Growth, calling it a “global cannabis leader in cannabis sales with a leading market share position in the recreational cannabis market.” It detailed the plan Canopy had shared earlier this year to reach positive adjusted EBITDA by its March 2022 quarter and to reach positive operating cash flow for all of the fiscal year ending in March 2023.

Of course, in November, Canopy Growth withdrew its outlook. At present, analysts don’t expect the company to generate positive adjusted EBITDA even in fiscal 2024. Additionally, the company has continued to lose share in the adult-use market in Canada. According to data from Hifyre, it was fifth behind Tilray, HEXO, Auxly and Organigram during the month of November, with share at just 8.8%. This has to be exceedingly disappointing to Constellation to see Canopy, which was the clear market share leader in Canada when it made its investment, struggle to remain in the top five.

Since then, there have been some substantial announcements. Most recently, the company announced the pending sale of its German pharmaceutical division, which accounted for C$11.9 million (9%) of revenue in its most recent quarter. The sale price was EUR80 million compared to the purchase price of EUR225.9 million in 2019. Even assuming a full earnout, the sale price of EUR126.6 million would represent a loss of 44%. This large loss extends upon substantial write-downs of fixed assets and inventory over the past two years.

On November 19th, shortly after its disappointing financial report, the company announced that CFO Mike Lee and President Rade Kovacevic are leaving at the end of 2021. Additionally, Constellation CEO Bill Newlands resigned from Board of Directors in late November, replaced by Constellation CFO Garth Hankinson. The company didn’t issue a press release, disclosing it instead in an SEC filing without any sort of explanation.

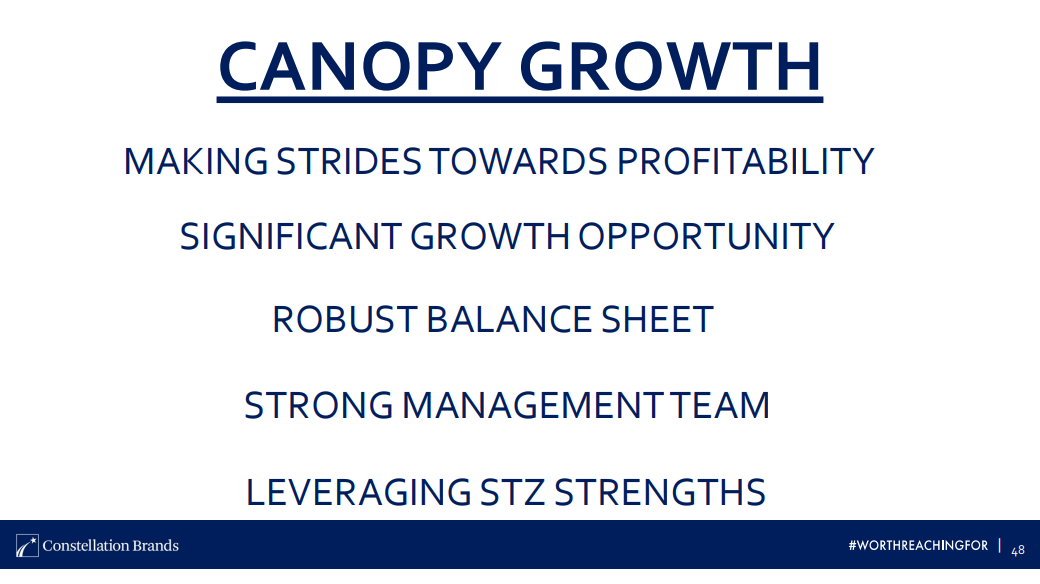

We can understand why Constellation is frustrated. Slide 48 from that investor presentation in October depicted Canopy Growth very positively:

Walking back its financial outlook certainly wiped out the first point regarding progress towards becoming profitable. In its fiscal Q2, Canopy Growth net revenue declined from a year ago by 3% to C$131 million, and the company’s adjusted EBITDA loss of C$163 million, hurt by inventory write-downs, was C$77 million worse than a year ago. Even excluding the inventory write-down, it would have been -C$76 million, the worst among all cannabis companies globally in both absolute levels as well as relative to revenue for those companies that generate substantial revenue.

Despite strong growth in the adult-use sales in Canada during that time, Canopy Growth’s sales into the adult-use market fell 1% compared to a year ago during its Q2. In fact, its sales in all cannabis categories except CBD fell compared to a year ago, as did its overall sales in what it calls “other consumer products,” which declined 12%, due primarily to the 34% decline in its Storz & Bickel unit. Canopy Growth, thus far, has failed to capitalize on its potential.

The balance sheet has become a substantial challenge that we think led the company to sell the German pharmaceutical subsidiary at a steep loss. The unit, which doesn’t fit with Constellation’s strategic vision for Canopy any longer, generated C$23.3 million of revenue in H1 of Canopy’s fiscal year, 8.7% of overall revenue. The sale price, including the full earnout, is about 3.5% of the current market cap of the entire company. This initial cash of approximately C$115.5 million will leave the company with about that amount of net cash at 12/31 by our estimate. We had previously discussed our expectation that total cash would be at or below the outstanding debt at that time due to the outflows from cash from operations and the up-front payment subsequent to 9/30 to Wana Brands. Canopy has total debt of C$1.5 billion, including C$600 million of debt due in June 2023 that is convertible at C$48.18, far above the current price, and a US$750 million credit facility that matures in 2026.

With respect to the point about a strong management team, two of the top executives at that time were fired in November, as detailed above, including the last remaining legacy Canopy exec as well as the Constellation-installed CFO.

At C$12.54, Canopy Growth now trades 67.5% below the cost of Constellation’s investment into the company. From our perspective, it has bet on the wrong horse. While some of the challenges Canopy has faced have been out of its control, like the slow rollout in Canada of adult-use, the pandemic and a longer path to entry into the United States than the company anticipated, it’s very clear that the company is not what Constellation thought that it was buying back in 2018. Canopy is not a leader in global cannabis, and it continues to bleed financially. The company has moved from an abundance of cash into a position of what will soon be net debt, and that debt is due in the intermediate term and will impede its growth in our view. At present, Canopy’s financials will continue to weigh on those of Constellation, leaving it in a tough position. After all, its own executives have been running the company for more than two years now and haven’t been able to fix the challenges.

How This Could Play Out

By November 2023, Constellation will have a big decision that it must make. At that time, its first tranche of warrants, 88.5 million at C$50.40 (about 4 times the current price), will expire. Barring a big rally in the stock, Constellation and Canopy could move to reduce the warrant conversion price and/or extend the term as we approach late 2023. Constellation could also potentially just buy the remaining shares of the company if the price continues to decline. Buying Canopy Growth could interfere with the company’s commitment to improving cash flow and returning capital to shareholders through dividends and share repurchases.

We think Constellation is in a tough position, as it must decide over the next 22 months how it can create value where it has failed to do so thus far. A big factor in how it addresses the situation will likely be the timing of its potential ability to own direct cannabis assets in the U.S. As long as Canopy Growth remains locked out of the market, it becomes increasingly difficult for Constellation to commit additional capital to it. If there is still no clear path for Canopy to enter the U.S., Constellation could move to exit its investment.

The recent sale of its German pharmaceutical unit could be the precursor to additional divestitures at Canopy Growth. The first source of additional funds to deal with the cash drain from its existing operations could be the sale of its Storz and Bickel unit. In the first half of fiscal 2022, the unit has generated revenue of C$38.6 million, or 14.4% of sales. Vaporizers don’t seem consistent with the overall strategy of Constellation at this time. When it announced the German divestiture, Canopy Growth defined its strategic focus as cannabis and cannabinoid-based consumer products. Canopy paid EUR145 million (equivalent now to C$210 million) and could likely generate slightly more than that currently. The retail stores could be another source of potential cash. In the first half of its fiscal year, Canopy Growth generated C$34 million in revenue from its stores in Canada, 12.7% of overall sales.

The problem with selling potentially non-core assets to address the weakening balance sheet and continued drain of its operations on cash flow is that Canopy Growth’s core Canadian cannabis operations are likely the biggest impediment to profitability, and this could lead Constellation and Canopy Growth to move in two directions. First, they could continue to consolidate the industry, as they did with their acquisition of Supreme earlier this year. This is a risky strategy, in our view. We think the more likely scenario is that the company moves to dramatically reduce its scale in Canada. This would likely entail substantial write-down of its C$353 million in inventory and C$1.1 billion in fixed assets, C$910 million of which is in Canada, as it further scales back its Canadian operations.

Canopy Growth’s financial condition has deteriorated substantially since Constellation made its investments into the company, and there is no quick fix. Not only has it used up most of the net cash that Constellation infused into it, but it is far from profitability and has failed to achieve the leadership position that such a substantial investment should have yielded. Now, Constellation must decide over the next two years how to address the problem. Canopy Growth’s future success seems likely tied to its ability to enter the U.S. cannabis market. It doubled down on its strategy of arranging future acquisitions with contractual agreements when it paid US$297.5 million for the right to acquire 85% of Wana Brands in October. Its rivals Cronos Group and Tilray have also been pursuing this strategy, but Canopy’s financial condition limits it from additional transactions in our view.

If Constellation, then, wants to continue to pursue the American cannabis market, it will need to infuse Canopy Growth with additional capital or acquire the company and use its own balance sheet. Alternatively, it could move to reduce the drain on cash by selling off some additional assets. Ultimately, we think it needs to fix its Canadian operations, which could be through additional consolidation to gain greater scale, which we think is less likely, or to dramatically reduce its focus on the market by pulling back on adult-use, a strategy that Aurora Cannabis has recently adopted.

Conclusion

Fear of missing out prompted a speculative investment into Canopy Growth four years ago. Constellation took control of Canopy effectively at a substantially higher price a year later and has been running the company since then, with control of the Board of Directors and through the installment of its own executives at the top of Canopy as well as deeper in the organizational chart. The results to date have been horrendous, and deterioration in Canopy’s outlook in November has already led to some big changes. Over the next two years, Constellation has a number of alternatives it can pursue, but the status quo, absent a change in the ability to conduct business in the American cannabis industry, will continue to challenge the company, which could see a negative impact on both the income statement (Canopy losses that flow through its P&L) and its balance sheet (carrying value of its investment). From our perspective, the best option is to retrench significantly from the Canadian adult-use market in order to improve cash flow ahead of its pending 2023 debt maturity. If Constellation is serious about the U.S. cannabis market, it needs to restore investor confidence in the stock of Canopy Growth. Otherwise, Canopy Growth won’t be able to continue to raise and deploy capital into the U.S.

Understand complex financials and get the facts with a subscription to Alan Brochstein’s 420 Investor, the longest running cannabis stock due diligence platform trusted by investors for over 8 years. The primary goal of 420 Investor is to provide professional, real-time, objective information about the top cannabis companies in the market in order to help investors Capitalize on Cannabis™.

New Cannabis Ventures publishes curated articles as well as exclusive news. Here is some of the most interesting business content from this week:

- Exclusive: Canadian Retail Cannabis Sales Increased 36% in October to $364 Million

- Exclusive: Flourish Software Looks to Power the Cannabis Industry as Core Piece of the Technology Stack

- Glass House Brands to Buy Plus Products for $25.6 Million

- Exclusive: How Trulieve is Evolving Beyond the Florida Medical Cannabis Market

- Key Investment Partners Raises $30 Million for Cannabis Venture Capital Fund

- Exclusive: Michigan Cannabis Sales Increase 66% in November to $153 Million

- Organigram Buys Quebec Cannabis Producer Laurentian Organic for $36 Million

- Planet 13 to Buy Next Green Wave Holdings for Approximately C$91 Million in Stock

- Exclusive: Why Pelorus Plans to Stay Private as It Continues to Fund the Buildout of the Cannabis Industry

To get real-time updates download our free mobile app for Android or Apple devices, like our Facebook page, or follow Alan on Twitter. Share and discover industry news with like-minded people on the largest cannabis investor and entrepreneur group on LinkedIn.

Get ahead of the crowd! If you are a cannabis investor and find value in our Sunday newsletters, subscribe to 420 Investor, Alan’s comprehensive stock due diligence platform since 2013. Gain immediate access to real-time and in-depth information and market intelligence about the publicly traded cannabis sector, including daily videos, weekly chats, model portfolios, a community forum and much more.

Use the suite of professionally managed NCV Cannabis Stock Indices to monitor the performance of publicly-traded cannabis companies within the day or over longer time-frames. In addition to the comprehensive Global Cannabis Stock Index, we offer a family of indices to track Canadian licensed producers as well as the American Cannabis Operator Index and the Ancillary Cannabis Index.

View the Public Cannabis Company Revenue & Income Tracker, which ranks the top revenue producing cannabis stocks.

Stay on top of some of the most important communications from public companies by viewing upcoming cannabis investor earnings conference calls.

Discover upcoming new listings with the curated Cannabis Stock IPOs and New Issues Tracker.

Sincerely,

Alan & Joel